Case Law Details

Macro Agencies Vs Commissioner of Customs (CESTAT Chennai)

The appeal before the CESTAT Chennai could not proceed because the appellant-proprietor had died during the pendency of the proceedings. When the matter was called, no one appeared for the appellant. The counsel informed the Tribunal through a letter dated 10.04.2026 that the appellant-proprietor had passed away and produced a copy of the death certificate issued by the Government of Karnataka. The Department was represented by the Additional Commissioner.

The Tribunal examined Rule 22 of the Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules, 1982, which provides that where an appellant dies, the appeal shall abate unless an application for continuance is filed by the successor-in-interest, executor, administrator, receiver, liquidator, or other legal representative within 60 days of the event. The Rule also permits the Tribunal to condone delay if sufficient cause is shown.

After considering the record, the Tribunal found that the appellant had died on 17.11.2023 while the appeal was pending. It also noted that no application had been filed by any successor or legal representative seeking continuance of the proceedings as required under Rule 22.

The Tribunal further relied on the Supreme Court’s decision in Shabina Abraham & Ors. Vs. Collector of Central Excise & Customs, wherein it was held that proceedings cannot be initiated or continued against a deceased person because doing so would violate the principles of natural justice, as the deceased is no longer alive to defend the case.

In view of Rule 22 and the Supreme Court’s ruling, the Tribunal held that the appeal stood abated upon the death of the appellant. Accordingly, the appeal was disposed of as abated.

FULL TEXT OF THE CESTAT CHENNAI ORDER

When the matter was called out none appeared for the Appellant. The Counsel on record has filed a letter dt. 10.04.2026 informing that Appellant-Proprietor is no more and in this regard, he has furnished a copy of Death Certificate issued by Govt of Karnataka.

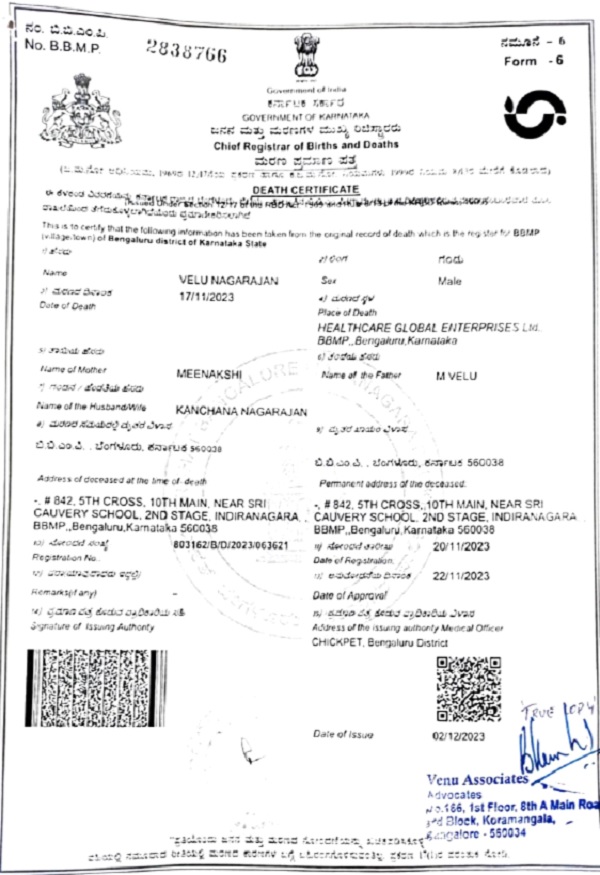

2. The Death Certificate of Appellant-Proprietor is reproduced below for ready reference:-

3. Smt. O.M. Reena, Ld. Additional Commissioner appeared for the Department.

4. On the death of the Appellant, the Appeal stands abated in terms of provisions of Rule 22 of the Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules, 1982. Rule 22 of the CESTAT (Procedure) Rules reads as under:-

“Rule 22. Continuance of proceedings after death or adjudication as an insolvent of a party to the appeal or application. – Where in any proceedings the appellant or applicant or a respondent dies or is adjudicated as an insolvent or in the case of a company, is being wound up, the appeal or application shall abate, unless an application is made for continuance of such proceedings by or against the successor-in-interest, the executor, administrator, receiver, liquidator or other legal representative of the appellant or applicant or respondent, as the case may be:

Provided that every such application shall be made within a period of sixty days of the occurrence of the event:

Provided further that the Tribunal may, if it is satisfied that the applicant was prevented by sufficient cause from presenting the application within the period so specified, allow it to be presented within such further period as it may deem fit.”

5. After perusing the material on record, we find the Appellant has died on 17.11.2023 during the pendency of the present Appeal. We also find that in terms of Rule 22 of Customs, Excise and Service Tax Appellate Tribunal (Procedures) Rules, 1982, on the death of the Appellant, the proceedings shall abate unless an application is made for continuance of such proceedings. In this case, no such application is made till date.

6. We find that in view of the judgement of the Hon’ble Supreme Court in the case of Shabina Abraham & Ors. Vs. Collector of Central Excise & Customs [2015 (322) E.L.T. 372 (SC)], wherein it has been held that no proceedings can be initiated or continued against a dead person as it amounts to violation of natural justice in as much as the dead person, who is proceeded against is not alive to defend himself. It is apt to quote from the case of Shabina Abraham & Ors. Vs. CCE :

“1. “Nothing is certain except death and taxes. Thus spake Benjamin Franklin in his letter of November 13, 1789 to Jean Baptiste Leroy. To tax the dead is a contradiction in terms. Tax laws are made by the living to tax the living. What survives the dead person is what is left behind in the form of such person’s property. This appeal raises questions as to whether the dead person’s property, in the form of his or her estate, can be taxed without the necessary machinery provisions in a tax statute. The precise question that arises in the present case is whether as assessment proceeding under the Central Excises and Salt Act, 1944, can continue against the legal representatives/estate of a sole proprietor/manufacturer after he is dead.”

7. In view of the above, we hold that on the death of the Appellant, the Appeal stands abated. The Appeal is accordingly disposed of.

(Dictated and pronounced in open court)

Author Bio