Discover the complete guide to start-ups, covering inception, marketing strategies, funding, tax benefits, registration under Start-up India Scheme, and the step-by-step closure process. Stay informed for successful entrepreneurship.

Start-ups are young organizations that aim to create or develop a unique, not necessarily new, product or service for the target market, specifically targeting customers. One of the main objectives of a start-up is to provide a remedy for deficiencies in existing products or create new products to solve one or more potential market gaps or problems. Some examples of big start-ups are Facebook, Netflix, and Apple.

The individuals who initiate start-ups are called entrepreneurs. Entrepreneurship is an attempt to create value through the recognition of a business opportunity, management of risk appropriate to the opportunity, and management of various functions of management.

Generally, start-ups require significant funding to create unique products or services, and they also need to make substantial investments in technological equipment. They are initially funded by their founders, but they also look for venture capitalists to fund their organizations. Venture capitalists are wealthy investors who like to invest their capital in start-ups with a long-term growth perspective.

Start-ups, like any other organization, need to make decisions about the 4Ps of marketing: Product, Price, Place, and Promotion.

Product: Start-ups need to define the product or service they want to offer. This involves identifying the unique features and benefits of the product, understanding the target market’s needs and preferences, and differentiating the product from competitors.

Price: Start-ups must determine the monetary value of their product or service. Pricing decisions involve considering factors such as production costs, market demand, competition, and perceived value by customers. It’s important to find a balance between setting a price that customers are willing to pay while ensuring profitability for the start-up.

Place: Start-ups need to decide where they will conduct their business operations. This could be online, in a physical office, or in a brick-and-mortar store, depending on the nature of the product or service. The choice of place should align with the target market’s preferences and accessibility.

Promotion: Promotion involves the communication and persuasion efforts used to reach and engage customers. Start-ups need to develop marketing strategies and tactics to create awareness, generate interest, and drive sales. This can include advertising, public relations, social media marketing, content creation, and other promotional activities.

By carefully considering and making decisions about these 4Ps, start-ups can effectively position their products or services in the market, attract customers, and achieve business success.

The date of incorporation for tax benefits for start-ups has been extended by our Finance Minister, Nirmala Sitharaman, in the budget for 2023 from March 31, 2023, to March 31, 2024.

The government helps start-ups directly and indirectly in many ways, such as through the Pradhan Mantri Mudra Yojana. The Pradhan Mantri Mudra Yojana is a scheme in which Mudra Banks provide loan facilities at very affordable rates to micro-finance institutions and NBFCs, which extend loan facilities to start-ups and small businesses. A maximum of Rs.10 lakhs can be granted as a loan under this facility, depending on whether a business is categorized as “sishu”, “kishor”, or experienced. An experienced business can obtain a loan of up to Rs.10 lakhs under the Pradhan Mantri Mudra Yojana, while a “shishu” business can obtain a loan of up to Rs.50,000, and a “kishor” business can obtain a loan of up to Rs.5 lakhs.

Page Contents

Minimum Tax compliance required from a start-up:

Minimum tax compliance required from a start-up includes filing Income Tax Return, Tax Audit Report, TDS Return, and assessment of tax liability under the Income Tax Act, 1961, as well as registration of the establishment under the GST Act and filing monthly, quarterly, and annual returns under the GST Act, 2017.

Registration under the Start-up India Scheme can be done for the following types of organizations:

- private companies,

- limited liability partnership firms,

- and partnership firms.

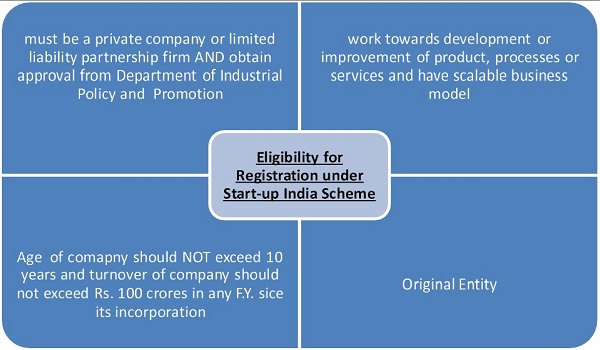

Eligibility for Registration under Start-up India Scheme

• The company to be formed must be a private company or limited liability partnership firm

• The organisation must obtain approval from Department of Industrial Policy and Promotion

• The organisation should work towards development or improvement of product, processes or services and have scalable business model.

• The organisation’s period of existence and operation should NOT exceed 10 years from date of incorporation

• The organisation should Not have turnover exceeding Rs. 100 crores for any of the financial year since its incorporation

• The organisation needs to be an original i.e. it should NOT have been formed by splitting up or reconstructing an already existing business

Benefits of Registering under Start-up India scheme

Benefits of registering under the Start-up India scheme include self-certification, fast-tracking of patent applications, tax exemptions under section 80IAC and section 56, easy winding up of the company, easier public procurement norms, access to funding, tax exemption on capital gains under section 54EE, exemption under section 54GB, the option to set off or carry forward losses, and more. Some of them are explained as below-

• Self-Certification: The Objective of self-certification is to reduce regulatory burden on start-ups. The main benefit to start-ups is that they are allowed to be self-certify compliance under 6 labour laws and 3 environmental laws through an online procedure. In case of labour laws, no inspection will be conducted for a period of 5 years and start-ups may only be inspected on receipt of credible and verified complaint of violation. In case of environmental laws, only random checks will be carried out.

• Patent Application: In case of start-ups, there is, generally, fast tracking of application of patent made by start-ups. Also, the entire cost, except statutory costs, of filing trade mark or patent by a start-up is bear by Central government. Also 80% of statutory fees is provided as REBATE to start-ups.

• Tax exemption under section 80IAC: Only start-up which is eligible for start-up India scheme and incorporated after 1st April, 2016, is eligible for exemption under section 80IAC. Eligible start-ups can be exempted from income tax on eligible business for 3 consecutive years out of first 10 years of incorporation.

• Exemption under section 56: A start-up which is a private limited company, DPIIT recognised, whose aggregate amount of paid up share capital and share premium, after issue, does not exceed Rs.25crores and not investing in specified class of assets, are eligible for exemption under section 56.

• Easy Winding up of Company: A start-up with simple debt structure or those meeting certain income criteria can be wound up within 90 days of filing an insolvency application.

• Easier Public Procurement Norms: Public procurement refers to the process by which the government and state-owned enterprises purchase goods and services from private sector. The Government has taken steps to make it easier for start-ups to participate in public procurement process.

• Access to Funding: One of the key challenge faces by start-up is access to finance. In order to provide funding support, Government will set up fund with an initial corpus of Rs.2500crores with total corpus of Rs.10000crores over a period 4 years.

• Tax Exemption on Capital Gains(Section 54EE): As per section 54EE, investment in government specified bond by eligible start-ups on LTCG is exempt up to Rs.50lakhs, if such start-up invest the amount within six months from the date of transfer of long term asset which shall remain invested for 3 years. In case of premature withdrawal the exemption will be revoked.

• Section 54GB: This section introduces to provide support to start-ups indirectly. As per section 54GB of Income Tax act, 1961, individual or HUF can get exemption on LTCG from sale of residential property if such individual or HUF invest amount of LTCG from sale of residential property in 50% or more in shares of eligible start-ups and does not sold or transfer such shares for a period of 5 years from the date of purchase.

• Option to set off or carry forward losses: If all shareholders of an eligible start-up who have voting power on last day of year in which losses were incurred continue to hold shares on last of previous year in which such losses to be carried forward, then the carry forward of such losses is permitted.

How to Register a start-up in India

• Step 1 Incorporate your Business: The very step is to incorporate business as a Private limited company or limited liability partnership firm under MCA and acquire certificate of incorporation or registration.

• Step 2 Register your business with start-up India: Once the entity is incorporated the next step is to registered as start-up under start-up India scheme by filing a form available on start-up India website.

• Step 3 Upload the Documents: An organisation needs to submit along with certificate of registration of company and brief description about products’/services’ innovative nature, one of the following in order register as start-up:

a) A recommendation letter concerning the innovative nature of business from an established incubator in an Indian post-graduate college approved by UGC in format specified by DIPP, OR

b) A letter of support from an incubator that has been funded for the project by Government of India, OR

c) A recommendation letter concerning the innovative nature of business from a Government approved incubator in format specified by DIPP, OR

d) A letter of fund from an incubation fund or angel fund or private equity fund, accelerator or angel network which is not less than 20 % in equity that is duly registered with SEBI and support the business innovation, OR

e) A letter of fund from a Government as part of any specified scheme that promote innovation

• Step 4 Determine whether you want to take advantage of tax break: In India, start-ups do not have to pay tax for first 3 years but to avail this benefit organisation needs to obtain certificate from Inter-Ministerial Board. However, start-ups recognised by DIPP do not have to obtain certificate from Inter-Ministerial Board in order to avail this benefit.

• Step 5 Self Certification: An organisation needs to self-certify following:

a) Organisation is a private limited, LLP or a partnership firm

b) Business must be incorporated or registered in India NOT before 10 years

c) Organisation’s annual turnover should NOT exceed Rs.100 crores

d) Organisation should work towards development or improvement of product, processes or services

e) Organisation needs to be original i.e. it should NOT have been formed by splitting up or reconstructing an already existing business

• Step 6 Obtain a recognition number: On application of this registration, organisation will obtain a recognition number but organisation obtains the certificate of registration only after the examination of all documents uploaded for this registration is performed.

However, if any discrepancy found in the uploaded documents then organisation will be punished with a fine of 50% of paid-up capital or Rs.25000 at least.

Step by step Registration process

• Visit the start-up India Official portal

• Enter details including email id, mobile number and desired password.

• Verify email id via an OTP

• Sign in using login credential

• Now create the profile which best defines your role and apply for Department for Promotion of Industry and Internal Trade(DPIIT) recognition to get ‘benefits as a start-up

• On the next page, click on “Get recognised” button

• Now, click on “DPIIT Recognition for start-up” which is under “schemes and policy” tab

• A form will appear which you need fill, after filling the form and uploading the documents, accept the terms and conditions and submit the form

• You will receive a recognition number unique to your start-up. If all documents uploaded are verified and no errors found, then within two days your organisation will obtain a certificate of recognition from DPIIT

Steps involved in Closure of Start-up

• Step 1 Determine whether there is a need for winding up: The organisation shall determine whether there is any need for shutting down business or any alternative is available with the help of which the business can survive and grow

• Step 2 Tax clearance to be obtain: When organisation decides to shut down its operations then they required to ensure that tax clearance are obtained and also ensure payment of indirect taxes is made

• Step 3 Surrender or cancel License, approvals etc.: A start-up obtains many licenses, approvals etc. for operating business. All these license, approvals etc. needs to be surrendered or cancelled after evaluating whether these licenses or approvals require specific consideration from relevant authorities.

• Step 4 Settle employees and complete Labour laws: Closure of business requires organisation to pay employees their dues as well as other benefits in accordance with labour laws in view of closure of business.

• Step 5 Settle dues of Creditors and Lenders: All dues of creditors and lenders need to be identified, negotiated and settled. Where the entity does not have adequate resources to settle such dues then organisation must go through Insolvency and bankruptcy code

• Step 6 Accounts to be closed: The organisation needs to close the accounts and in case of surplus the organisation shall distribute such surplus among co-founders

• Step 7 File for Closure of the legal entity: After completing all steps mentioned above, the organisation shall submit application of closure of business to registrar along with documents required for such purposes

• Step 8 Retain Records: The co-founders may require to retain the critical and crucial records about organisation and its closure in a manner as may require by law and regulation and for a time period as may require by law and regulation

Ways to Shut-Down Start-up

• Fast-Track Exit Mode: It is the best suited for start-up as it involves least cost and time to shut-down the organisation. In order to apply for a fast track exit, an organisation should:

a) NOT have any assets and liabilities

b) NOT had any start-up business operations for the past years

If these two conditions are met, the organisation can shut-down its operations through Fast-track exit mode

• Voluntary Closure: Another way to shut down start-up business is voluntary closure; however this requires shareholders and creditors to be on the same page with regard to details of closure. While it is an easy route, it might not always be practical

• Court or Tribunal Route: It is the traditional mode of closure, however not best suited for start-ups as it involves a lot of time and cost

In addition to above stated means, The Insolvency and Bankruptcy Bill, 2015 is a new closure tool. This requires start-up to have simple debt structure, where an insolvency professional is hired to liquidate assets of company within 90 days.

When a start-up business does not wish to operate but also not want to shut down, it can apply to be a ‘Dormant company’, that allows company to stay afloat with minimum compliance. However, a dormant company for a period of more than 5 years is automatically struck off from Roc.

******

The author can be however contacted for further clarification at 9654182791 or via mail at caajay92@gmail.com

DISCLAIMER:- This Blog is for the purposes of information / knowledge and shall not be treated as solicitation in any manner or of for any other purposes whatsoever.

Author Bio