Introduction:

Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) is a kind of advance tax that needs to be deposited with the government periodically and the onus of doing the same lies on the deductor or collector respectively rather than taxpayer. For the tax payer, TDS or TCS can be claimed in the form of a tax credit at the time of filing their income tax return. Since there is an increase in the applicability of TDS or TCS more and more individuals would face deduction of TDS on incomes or collection of TCS on expenses. Trend of past few years have indicated that the ambit of TDS or TCS have increased leaps and bounds.

If at the time of filing returns, the tax payer realises that his tax liability is considerably less than what he actually paid, then he can claim the refund for the same. However, in case where the tax payer thinks that his tax liability for the year will be NIL or less than TDS or TCS rate applicable on a particular source of income or expenditure, the Income Tax Act permits him to apply for a lower rate of TDS/TCS or no TDS/TCS which helps to avoid unnecessary withholding of tax payer’s funds with the government.

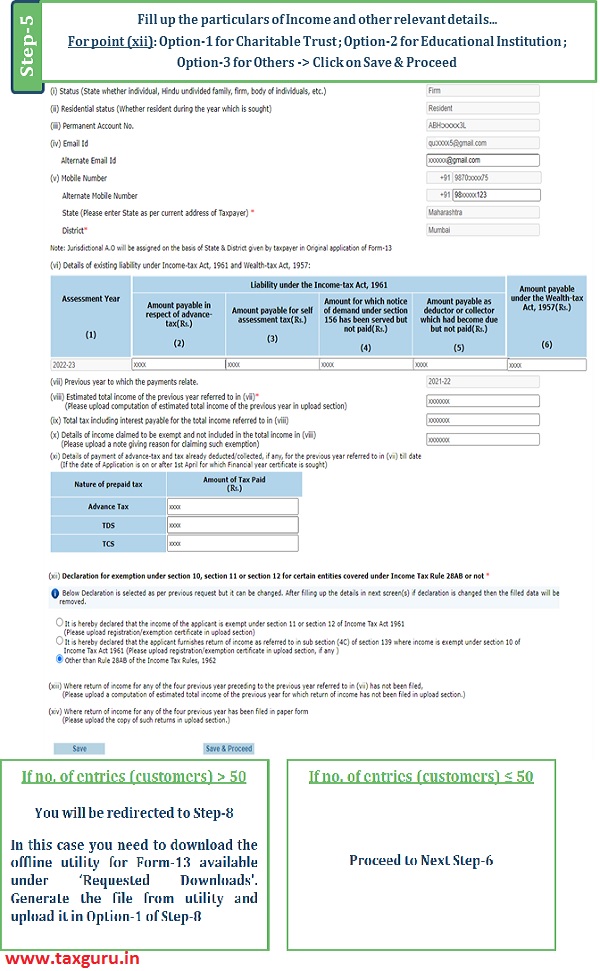

Taxpayer claiming lower rate or nil rate TDS/TCS needs to submit the application to the Assessing Officer in Form-13 (Annexure-I for No/Lower Deduction / Annexure-III for Lower Collection). Pursuant to the processing of the application, the AO issues the Lower Deduction Certificate (LDC). In this certificate, the Income Tax Department seeks a list of parties who may deduct/collect tax while transacting with the Assessee and directs them to deduct/collect tax at lower rate or no rate as determined by the AO.

LDC is issued for a particular financial year and stands valid from the date of issue till the end of financial year unless cancelled by the assessing officer before the expiry.

Benefits of Lower Deduction or No Deduction Certificate:

1. Requirement of Working Capital is fulfilled since lower or no tax is deducted or collected while receiving or paying as the case may be

2. On account of lower deduction certificate, the amount of refund if any would be less and the refund would be initiated earlier

3. Time Value of Money- The Govt. provides interest @6% on Refund amount whereas if that amount is invested in the market would give higher returns

4. The risk of default on the part deductor or collector of not depositing the TDS or TCS with the government is mitigated

Who can ideally apply for non/lower deduction certificate?

List of Documents required to file application in Form 13:

1. Covering Letter containing the following:

a. Nature of income (specifying heads of income), business activities, and nature of activities.

b. Reason for applying LDC

c. Suggested Rate of LDC (Cannot be less than: Est. Tax Payable ÷ Est. Turnover * 100)

2. Computation of Income, Audited P&L and Balance Sheet with relevant annexure/schedules of last 4 financials years (in case audit is not done for Previous FY, we need to furnish provisional accounts)

3. Income Tax returns of Last 2 years (ITR Form and Acknowledgement)

4. Details of tax deduction of last 3 years (Form 26AS)

5. Projected P&L account, Balance Sheet and Computation of Income and tax thereon for the Current Financial Year

6. List of Parties containing

a. Name &TAN

b. Section under which tax is to be deducted at source

c. Amount (expected to be received as per projected financials)

7. Assessment / Survey Orders (if issued) for last 4 Assessment Years

8. Copy of last LDC issued u/s. 197

9. Screenshots of TDS return filing status of Previous FY along with acknowledgement

10. Challan reflecting the payment of outstanding demand if any against TAN / PAN

Procedure for making the application in Form 13

Application for Nil or Lower Deduction is required to be filed using the Form-13 with the Assessing Officer (TDS) seeking permission. Form-13 has to be filed Online.

Steps for making application Online through https://www.tdscpc.gov.in/

Authors:

| Vishal Kothari | Director | +91-9320614111 | vishal.kothari@masd.co.in |

| Ashish Raithatha | Consultant | +91-9819911153 | ashish.raithatha@masd.co.in |

Author Bio

Helpful to avoid lengthy time taken for refund.

VERY USEFUL ARTICLE!