-Chintan Mehuriya & Jaya Singhania

What Is ‘Corporate Fraud’?

Corporate fraud consists of activities undertaken by an individual or company that are done in a dishonest or illegal manner, and are designed to give an advantage to the perpetrating individual or company. Corporate fraud schemes go beyond the scope of an employee’s stated position, and are marked by their complexity and economic impact on the business, other employees and outside parties.

Regulatory Legislations :-

1. Indian Contract Act 1872.

2. Indian Penal Code 1860.

3. Prevention of Corruption Act 2013.

4. Prevention of Money laundering Act 2012.

5. The Companies Act 1956& 2013.

6. Information Technology Act 2008.

7. Prohibition of Insider Trading.

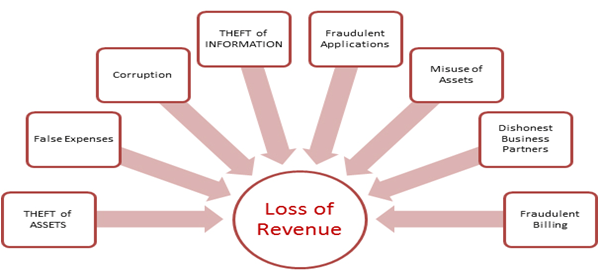

Types of Fraud:-

There are many types of corporate fraud, including the following common frauds:

1. Theft of cash, physical assets or confidential information

2. Misuse of accounts

3. Procurement fraud

4. Payroll fraud

5. Financial accounting mis-statements

6. Inappropriate journal vouchers

7. Suspense accounting fraud

8. Fraudulent expense claims

9. False employment credentials

10. Bribery and corruption.

Who conducts the investigation?

HR managers are increasingly being called upon to conduct in-house investigations. The question of whether to bring in law enforcement, a regulatory agency, external audit teams, a private law firm, or handle the matter in-house is an open one. This decision is fact and case specific, and will depend upon the duration and breadth of the potential

problem as well as potential in-house investigatory skills. Many times the in-house investigations are coordinated with outside counsel. If the company initially decides that it will conduct an internal investigation instead of an external investigation, the roles of the individuals involved in the investigation should be clearly delineated. If the investigation is conducted in-house under the supervision of an HR manager, the benefits may include:

1. Heightened knowledge about the company’s business, employees, and procedures;

2. Increased control over the investigation as well as the possible resulting publicity;

3. An unfiltered view of the fraud and the extent of it.

Keeping the investigation in-house will also prevent possible problems with the Fair Credit Reporting Act (FCRA). The FCRA applies generally to workplace investigations, but does not apply when the investigation is done completely in-house. On the other hand, the disadvantages to keeping the investigation in-house may include:

1. Lack of attorney-client privilege;

2. Insufficient training In carrying out fraud investigations;

3. Less objectivity than an external investigation;

4. Possible conflicts between the company’s well-being and management’s professional obligations; and

5. Possible loyalty issues between the investigator and the employees and lack of support.4 although some of the disadvantages are not damaging to the company generally, the existence of such factors when conducting an in-house investigation might be problematic.

How to Prevent Fraud :-

One of the best ways to develop policies and procedures that are effective in prevention corporate fraud is with the assistance of an experienced anti-fraud professional who has investigated hundreds of frauds to develop the most relevant and most effective anti-fraud controls including:

1. Establish clear and easy to understand standards from the top down. Have an employee manual that clearly outlines these standards and keeps the rules from becoming arbitrary.

2. Always check references and perform background checks that include employment, credit, licensing and criminal history for all new hires.

3. Secure physical assets, access to data, and money at all levels including monitoring and using pre-numbered checks, keep checks locked up, have a “voided check” procedure and never sign blank checks. Review all disbursements regularly.

4. Segregation of duties of employees. Divide activities so one employee doesn’t have too much control over an area or duty. Separate important accounting and account payable functions. Small-business owners and managers should review every payroll check personally. The person who has custody of the checks should never have check signing authority. The person opening the mail should not record the receivables and reconcile the accounts.

5. Proper authorization of transactions, ensuring that employees aren’t exceeding their authority.

6. Independent checks on performance, using audits, surprise check-ups, inventory counts, or other procedures to verify compliance with policies and procedures, as well as accuracy.

7. Instill an anonymous reporting mechanism, such as an employee fraud hotline.

8. Small-business owners should control who first receives the bank statements and other sensitive documents. Consider a separate post office box for the purpose of receiving bank statements, customer receipts or any other sensitive documents.

9. All account reconciliations and general ledger balances should have an independent review by a person outside the responsibility area such as an outside accountant. This allows for reviews, better ensuring nothing is amiss and providing a deterrent for fraudulent activities.

10. Conduct annual audits to motivate all bookkeeping- related staff to keep things honest because they can never be sure what questions an auditor is going to ask or what documents an auditor may request to review.

11. While no company, even with the strongest internal controls, is completely protected from fraud, strengthening internal control policies, processes and procedures will go a long way towards making your company a less attractive target to both internal and external criminals.

Corporate Scandals :–

One of the most reputed company revealed in September that it had installed software on millions of cars in order to trick the Environmental Protection Agency’s emissions testers into thinking that the cars were more environmentally friendly than they were, investors understandably deserted the company.

Company lost roughly $20 billion in market capitalization, as investors worried about the cost of compensating customers for selling those cars that weren’t compliant with environmental regulations.

The company not only has to deal with compensating their customers, but it will also need to contend with potential fines from regulators as well as a reputational hit that could severely affect its market share.

Other Example of Corporate Scandal is one of the biggest Ponzi schemes in West Bengal that enjoyed political patronage and lured millions of investors to deposit money with the promise of abnormally high returns including fancy holidays etc. The chit fund eventually collapsed leading to defaults after a crackdown by SEBI and the Reserve Bank of India. The default, apart from leaving small depositors high and dry, also led to 10 media outlets owned by company being forced to wind up, leaving 1000 journalists jobless.

And an online business survey firm that collected thousands of cores of rupees from over 24 lakh investors, asking them to fill surveys and guaranteeing to quadruple their income in one year, company was accused of running a Ponzi scheme. A criminal case was registered against the company in 2011, some accounts frozen and its business shutdown.

Penalty or Punishment under the various acts :-

As Per Section 447 of Companies Act 2013, prescribes that the person who is guilty of fraud shall be punishable with imprisonment for a term not less than 6 months and up to 10 years and fine, which shall not be less than the amount involved in the fraud and may extend to thrice of such amount.

If the fraud involves public interest, the minimum imprisonment to be awarded shall be 3 years.

As per Prevention of Money laundering Act 2012 if any person convicted offence in this act, there can be punishment of imprisonment up to 3-7 years with fine up to 5 lakh rupees.

As per Indian Penal Code 1860, punishment of offences, every person shall be liable to punishment under this Code and not otherwise for every act or omission contrary to the provisions thereof, of which he shall be guilty within India.

As per Section 66F (Acts of cyber terrorism) of Information Technology Act 2002, If a person denies access to authorized personnel to a computer resource, accesses a protected system or introduces contaminant into a system, with the intention of threatening the unity, integrity, sovereignty or security of India, then he commits cyber terrorism and he is liable for Imprisonment up to life.

The corporate world is witnessing various changes. Corporate world’s networks are increasingly being targeted by cyber criminals. Each passing day comes up with some news about breaches on corporate networks at global and Indian levels. For running the day-to-day affairs of corporates, the electronic format is the defacto format.

Corporates need to be aware to the facts that the law has gone ahead and given an expansive definition of personal information to mean any information that relates to a natural person, which, either directly or indirectly, in combination with other information available or likely to be available with a body corporate, is capable of identifying such person. Further, the law has gone ahead and defined what constitutes sensitive personal data or information. Sensitive personal data or information of a person has been defined to mean such personal information which consists of information relating to; ―

1. Password;

2. Financial information such as Bank account or credit card or debit card or other payment instrument details;

3. Physical, physiological and mental health condition;

4. Sexual orientation;

5. Medical records and history;

6. Biometric information;

7. Any detail relating to the above clauses as provided to body corporate for providing service; and

8. Any of the information received under above clauses by body corporate for processing, stored or processed under lawful contract or otherwise.

9. Companies are required to have detailed terms and conditions, rules and regulations as also privacy policies, while handling or dealing with information including sensitive personal information or data. Companies should also have policies for collection, preservation, retention, disclosure and transfer of sensitive personal information.

What Are the Precautions Taken By All Companies?

1. Know Your Employees

2. Make Employees Aware/Set Up Reporting System

3. Implement Internal Controls

4. Monitor Vacation Balances

5. Hire Experts

6. Live the Corporate Culture

Conclusion :-

Corporate frauds and scams greatly erode corporate wealth. Corporate India as a whole has a vested interest in preventing and minimizing corporate frauds and scams. Independent directors on audit committees provide one of the best ways of reinforcing internal audit and annual statutory audit. Their independence must be strengthened. With respect to incentives, in end executive compensation is about ethics and can only be sparingly controlled. The solutions to corporate fraud must be comprehensive and all encompassing.

Very well explained