Introduction: –

A blockchain is a distributed database or ledger that is shared among the nodes of a computer network. Blockchain started to gain visibility back in 2009 when Bitcoin was invented using this technology. As a database, a blockchain stores information electronically in digital format. Blockchains are best known for their crucial role in cryptocurrency systems for maintaining a secure and decentralized record of transactions.

From Business point of view, Blockchain is an advanced database system that allows transparent sharing of information between various business networks. It is system that has built-in mechanisms that prevent unauthorized transaction or entries in the system of the business which creates consistency in shared view of these transactions.

Key Features of Blockchain: –

1. Decentralization:

Absence of traditional centralized organization is the main benefit of blockchain technology. It is done through public distributed ledger which is a shared database. If anyone tries to change data in one of the blocks, everyone in the network will be intimated and will be able to see the change. This way, data tampering will be restricted.

2. Smart contracts:

Smart contracts are programs that executes the transaction as exactly coded by the programmers. They are stored in blockchain and runs automatically when certain conditions are met. Smart contracts are enforceable by code.

3. Immutability:

Immutability means something that cannot be changed or altered. Once someone has recorded any transaction, it cannot be altered. One can reverse the mistake by passing the right entry which will be visible to the network.

4. Consensus:

Blockchain system establishes rules that allows participants to make changes or record new transactions on consent basis. Through this system, changes or new transaction can be made only when maximum participants give their consent for the same.

5. Public Key Cryptography:

To uniquely identify the participants in the network, blockchain uses public key cryptography. Two set of keys is generated for network members. One key is a public key that is common to all participants in the network, while other is a private key that is unique to every member. Both the keys works simultaneously to unlock data in the system.

Application of Blockchain: –

There are various uses of Blockchain technology spread over multiple businesses. Some of them are explained below:

1. Banking Sector – Many complex process included in core banking service of banks can be handled smoothly by blockchain technology. Some of the process harmonised are real time verification of financial documents, streamlined credit prediction, real time asset management, and enforcement of regulatory controls. This technology reduces counterparty risk and decreases issuance and settlement times.

2. Supply Chain – Combination of IOT and Blockchain technology allows business to track shipments and make payments when certain conditions are met, (i.e. only when product is delivered to the specified person). Using smart containers can indicate the companies of the lower inventory levels. In this way each step can be recorded and authenticated via blockchain.

3. Entertainment And Media – Management of Copyright data is done through blockchain by many companies, since copyright verification is critical for fair compensation of artists. Transparent and real time distribution of royalty can be ensured through this technology.

4. Healthcare Sector – Blockchain is used in healthcare to preserve patient data through hospitals, diagnostic laboratories, pharmacies and physicians. It plays an influential role in handling deception in clinical trials. This technology offers data efficiency in healthcare.

5. Food Industry – Applicability of Blockchain provides the food brands to trace the product’s route from its origin, through each stop it makes and finally the delivery. Through this system, if the products are ever contaminated, the source of such contamination can be easily traced back. Identification of the problem to occur can be detected far sooner which may saves lives.

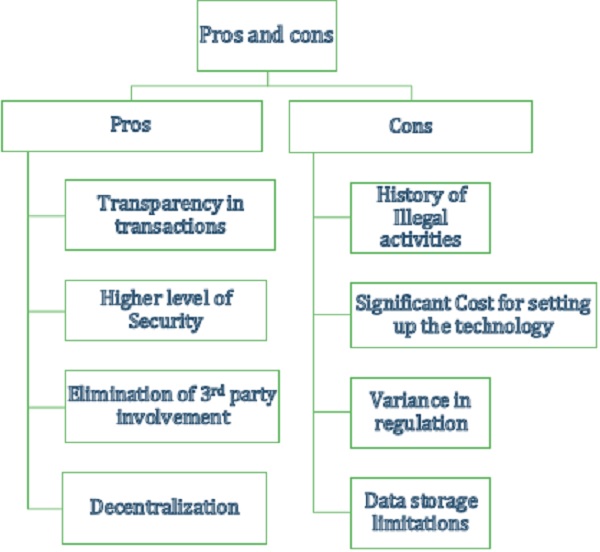

Pros and Cons of Blockchain:-

Conclusion: –

Relationship can flourish between organisations and people if it is built on trust. Blockchain technology can elevate that trust to an entirely new level by helping parties to automate processes, authenticate and record transactions at level. This leads to lesser disputes and paperwork which will automatically lead to happier customers and entirely new level of doing business. With provision of high level of security and trust that modern transactions require, blockchain technology is changing the way how businesses are operating.

******

(This article represents the views of the authors only and does not intent to give any kind of legal opinion on any matter)

Authors:

Parth Desai | Director| +919819238879 | parth.desai@masd.co.in

Shripriya Aithal | Associate Consultant |+918779984264|shripriya.

Author Bio