This Section comes into picture when Company does some specified contracts or arrangements with related parties. The intention behind this section is to protect the company from any loss which may arise to it because of any transaction with related parties as defined in the Act. This Section only specifies 7 transactions and provisions related to those transactions. Related Party is defined under Section 2(76) of The Companies Act, 2013. Section 188 will not be applicable on every transaction with such parties. Provisions of this Section will be applied only when following contracts and arrangements with related parties are entered into-

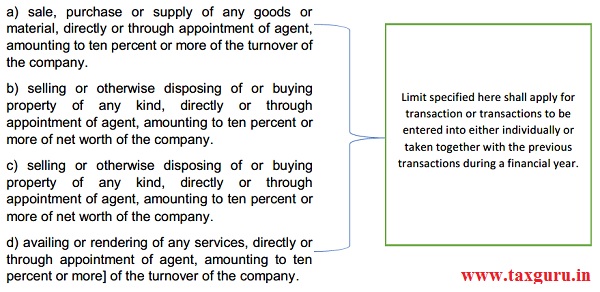

(a) sale, purchase or supply of any goods or materials.

(b) selling or otherwise disposing of, or buying, property of any kind.

(c) leasing of property of any kind.

(d) availing or rendering of any services.

(e) appointment of any agent for purchase or sale of goods, materials, services or property.

(f) such related party’s appointment to any office or place of profit in the company, its subsidiary company or associate company.

(g) underwriting the subscription of any securities or derivatives thereof, of the company1.

If such Contract and Arrangement is below the threshold then Board Resolution passed in meeting of Board of Directors would be enough. If amount of Contract and Arrangement is up to the specified threshold or above then in addition to Board Resolution, Resolution in the meeting of shareholders is also required i.e., Ordinary Resolution.

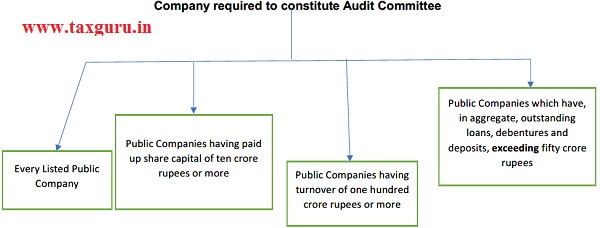

If a company is such which is required to constitute Audit Committee then approval of Audit Committee is also needed in addition to above resolutions, as the case may be.

–

e) is for appointment to any office or place of profit in the company, its subsidiary company or associate company at a monthly remuneration exceeding two and a half lakh rupees.

f) is for remuneration for underwriting the subscription of any securities or derivatives thereof, of the company exceeding one percent of the net worth.

If any such transaction is entered by director or employee without obtaining required consent mentioned above then such is to be ratified within 3 months by the Board or Shareholders, as the case may be. If it is not ratified, it shall be voidable at the option of Board or Shareholders, as the case may be.

Penal Provisions

Any director or any other employee of a company, who had entered into or authorized the contract or arrangement in violation of the provisions of this section shall—

(i) in case of listed company, be punishable with imprisonment for a term which may extend to one year or with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees, or with both; and

(ii) In case of any other company, be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees.

Related Party means-

(i) a director or his relative

(ii) a key managerial personnel or his relative

(iii) a firm, in which a director, manager or his relative is a partner

(iv) a private company in which a director or manager 1[or his relative] is a member or director

(v) a public company in which a director or manager is a director and holds along with his relatives, more than two per cent of its paid-up share capital

(vi) any body corporate whose Board of Directors, managing director or manager is accustomed to act in accordance with the advice, directions or instructions of a director or manager

(vii) any person on whose advice, directions or instructions a director or manager is accustomed to act

(viii) any body corporate which is—

a holding, subsidiary or an associate company of such company

a subsidiary of a holding company to which it is also a subsidiary, or

an investing company or the venturer of the company

(ix) a director other than an independent director or key managerial personnel of the holding company or his relative, shall be deemed to be a related party.

Relative means-

any one who is related to another, if—

(i) they are members of a Hindu Undivided Family

(ii) they are husband and wife, or

(iii) A person shall be deemed to be the relative of another, if he or she is related to another in the following manner, namely:-

(a) father (including step father)

(b) mother (including step mother)

(c) son (including step son) and his wife

(d) daughter and his husband

(e) brother (including step brother)

(f) sister (including step sister)

Company required to constitute Audit Committee

Author Bio

I want to write articles on Tax guru on regular basis on company law, gst and startup India