When a company expands it requires additional funds. One of the many ways to raise additional capital for a listed company is rights issue of shares. If a company issues shares to the public at large, it may affect the voting rights of the existing shareholders of the company. So in order to avoid this imbalance occurring, the company issues additional shares to the existing shareholders of the company. It is an invitation to the existing shareholders to buy the new shares. This type of issue provides securities to the shareholders. These securities are called rights. In this article we have discussed about Rights issue of shares under the Companies Act 2013

Page Contents

- Right Issue means to offer shares to the existing shareholders of the company in proportion to their existing share holding in the company for the purpose of raising fresh capital for the company.

- Right issue is ideal for the small companies where the power of the shareholding remains with the shareholders of the company only.

- In other words, it is “pre-emptive right” that a shareholder has in a company in preference to an outsider.

- Whether it is a Private Limited Company, a Public Limited Company, listed or unlisted company can go for Right Issue.

- With these rights the shareholders of the company can purchase new shares at a discounted rate to the market price.

Following are the types of rights issues:

- Fully paid rights issue: Where an applicant has to pay the entire issue amount at the time of the application of the issue is called a fully paid rights issue.

- Partly paid rights issue: Where an applicant is required to pay only a partial amount at the time of the application is called a partly paid rights while the balance amount is to be paid as and when the company makes the subsequent calls.

- Renounceable rights issue: In this kind of rights issue, the rights issue can b transferred or sold in the open market to other investors. When a renounceable rights holder does not wish to subscribe to his rights, he can opt to transfer his rights.

- Non-renounceable rights issue: A non-renounceable rights issue cannot be transferred or sold to anyone. When the renounceable rights issue holder is no more willing to exercise his right to buy the rights share will have the only option to give up his rights and let the rights issue lapse.

- When a company sets out a plan for expansion, the requirement of a huge amount of capital arises. At this time, the companies may like to go for equity to avoid fixed payments of interest instead of getting funds from the market. So for raising equity capital, a right issue may be a faster way to achieve the objective compared to any other way.

- When a company is into a project where debt or loan funding is not available or expensive, the company may raise capital through a rights issue.

- When the companies are looking for improvement in the debt-to-equity ratio or is planning to buy a new company may opt for funding via the same route.

- When the company is in debt, such company may issue shares to pay off the debt and to improve the financial health.

Step 1: Hold a board meeting

When the company decides to issue shares, the company needs to hold a board meeting. For this purpose, a notice needs to be given to the members at least 7 days prior to such board meeting mentioning the agenda for the meeting.

Step 2: Pass the resolution

In the board meeting the resolution needs to be passed for the following purposes:

- For approving the offer letter to issue shares on the basis of the rights.

- For fixing the date, price of the shares and ratio on which the rights issue will be given.

- For right issue shares to the existing shareholders.

Step 3: Notice of offer

After passing the resolution, the notice letter of offer needs to be sent through registered or speed post or through electronic mode to all the existing shareholders at least before the opening of the issue. The letter of offer shall contain the number of the shares offered to the shareholders. The shareholder shall be given a time period of 15 to 30 days to accept or reject the offer.

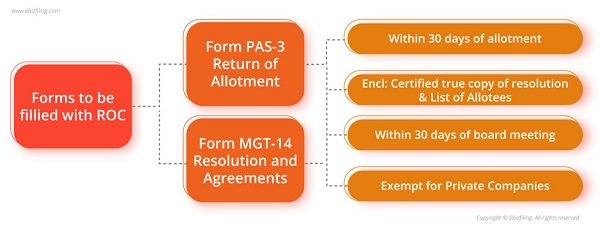

Step 4: File form MGT 14

Once the resolution is passed, the company needs to file Form MGT 14 with ROC within 30 days of passing such resolution. The form MGT 14 is mandatory only for the public limited companies and not for the private limited companies. Form MGT 14 needs to be filed with the true certified copy of the board resolution.

Step 5: Receipt of the money

The shareholders who have accepted the application must send the accepted application along with the application money. The company shall make the arrangement for the receipt of the share application money.

Step 6: Conduct the second board meeting

After the receipt of the application money, the company needs to hold the second board meeting within 60 days. Once the company passes the resolution for the allotment of shares, then the company must allot the shares within the 60 days of receiving the application money. However, if the company fails to allot the securities, the compay needs to repay the application money to the subscribe within 15 days from the date of the completion of the 60 days. Also, if the company fails to repay the money within 15 days, the company shall have to repay the interest at the rate of 12% alongside the application money.

Step 7: Filing of forms with ROC:

After the conclusion of the second board meeting and allotment of shares, the company needs to file form PAS 3 with the ROC within 30 days. The form PAS 3 must be filed with the attachment of true certified copies of the list of the shareholders whom the shares have been allotted and the board resolution.

Step 8: Issue of shares certifictes:

The last step would be to issue the share certificates in Form SH- 1. If the shares are in Demat form, then the company is required to intimate the depository on an immediate basis on allotment of shares. However, if the shares so issued are in physical form, the share certificates must be issued within 2 months from the date of allotment of shares.

Penalty for not complying with the provisions of Right Issue

There is no provision for the penalty if the company or directors fails to comply with the provisions of right issue. However, the company and the director of the company who are in default, and no provisions have been prescribed for penalty, in such cases, the company and associated officer shall be punishable with fine up to RS. 10,000/- and further fine of Rs. 1000/- for every day after the first during the time contravention continues.

The right issue of shares is beneficial to both the company and the existing shareholders. Such shareholder will get the advantage of getting shares at a discounted rate and also can retain the voting rights. On the other hand the company will be able to raise a huge amount of share capital by resorting to the issue of rights shares.

My Share premium price for Rights Issue comes comes at Rs. 15528.29/- Should it be rounded off to 15529? Is there any such provision?