BACKGROUND:

The Limited Liability Partnership (LLPs) is an alternative corporate business vehicle that provides the benefits of limited liability but allows its members the flexibility of organizing their internal structure as a partnership based on a mutually arrived agreement. In order to provide greater ease of doing business in India to law abiding LLPs, it was the need of the hour to review the penal provisions of the Act so as to decriminalize compoundable offences involving minor, procedural or technical violations of the Act, or offences which can be objectively identified as where no fraud or mala fide intent is present nor is there any harm to public interest.

On Wednesday, 28th July, 2021 Cabinet has passed LLP Amendment Bill, 2021. This will be the first time that changes are being made to the Act since it came into effect in 2009. They have made 29 amendments to LLP Act 2008 by LLP Amendment Bill 2021.

OBJECTIVE OF AMENDMENTS:

The main objects behind the LLP amendment bill, 2021 are as follow:

- To encourage the conversion of partnership firm into LLPs;

- To make LLP popular for startups;

- To provide greater ease of doing business in India;

- The objective of the De-criminalization exercise is to remove criminality of offences from business laws where no malafide intentions are involved;

- To promote the formation of LLPs.

HIGHLIGHTS OF THE AMENDMENT:

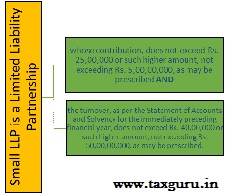

Small limited liability partnership– The Bill defines the term “small limited liability partnership”. The definition is an exhaustive definition.

- Residency of designated partners– There is a pre-requisite for each LLP to have at least 2 designated partners who are individuals and at least one of them shall be a resident in India. While determining the condition of residency the amendment bill has reduced the term of stay to 20 days during the financial year.

- Accounting Standards– the Central Government, in consultation with the National Financial Reporting Authority constituted, prescribe the Accounting Standards and prescribe the Auditing Standards, as recommended by the Institute of Chartered Accountants of India for a particular class of LLP.

- Authority to Regional Director– the Bill provides that a Regional Director, authorized by the Central Government, may compound such offences. The compounding provisions have been brought in line with the compounding provisions mentioned under the Companies Act, 2013

- Establishment of Special Courts– For the purpose of speedy trial of offences, the Central Government may establish Special Courts. The amendment bill further mentions the composition of such courts which is as follows:

(i) a Sessions Judge or an Additional Sessions Judge, for offences punishable with imprisonment of 3 years or more; and

(ii) a Metropolitan Magistrate or a Judicial Magistrate, for other offences. They will be appointed with the concurrence of the Chief Justice of the High Court.

The Amendment Bill also elaborates on the procedure of trial of such Special Courts. The appeal and revision petitions shall lie to the High Court within whose jurisdiction the Special Court is located.

- Registration of documents– Any document required to be registered with Registrar, if, is not registered within the time frame, may be registered after that time, on payment of such additional fee in addition to any fee as is payable.

- Role of Appellate Tribunal– Appeal shall lie to the Appellate Tribunal. No appeal shall lie to the Appellate Tribunal from an order made by the Tribunal with the consent of parties. The time frame within which appeal shall be filed is period of 60 days. For sufficient cause the time frame can be extended if the Appellate Tribunal is satisfied with the cause. Opportunity of being heard is an important element while dealing with appeals filed.

- Penalty for offences– If an LLP or any partner or any person contravenes this Act or the rules, the defaulter, shall be liable to a penalty of Rs. 5,000 and in case of a continuing contravention with a further penalty of Rs. 100 for each day after the first during which such contravention continues, subject to a maximum of Rs. 1, 00,000.

- Punishment for defraud– If an LLP or its partners carry out an activity to defraud their creditors, or for any other fraudulent purpose, every person party to it knowingly is punishable with imprisonment now of up to 5 years and a fine between Rs 50,000 and Rs. 5,00,000.

- Adjudication of penalties– The amendment bill provides for adjudication of penalties by officers appointed by the Central Government not below the rank of Registrar. The officer may by border impose penalty. The penalty where payable by a small LLP or start-up LLP or by its partner the such penalty shall be to the tune of one-half of the penalty specified subject to a maximum of Rs. 1,00,000 for LLP and Rs. 50,000 for every partner or any other person. Opportunity of being heard play the key role under this proceeding.

Appeal shall lie to the Regional Director in case the party is aggrieved by the order of the Registrar which shall be filed within 60 days.

Where an LLP fails to comply with the order within 90 days from the date of receipt of order, shall be punishable with fine not be less than Rs. 25,000, but may extend to Rs. 5,00,000.

Where a partner or designated partner fails to comply with an order within 90 days from the date of receipt of order, shall be punishable with imprisonment which may extend to 6 months or with fine which shall not be less than Rs. 25,000 but may extend to Rs. 1,00,000, or both.

- Decriminalizing certain offences: The Bill seeks to decriminalize numerous sections bearing in mind the harsh consequences of criminal proceeding on the overall functioning of the LLP.

The list of sections is as follows:

| Sr. No. | Relevant Section | Provision |

| 1. | section 7(1) | Every limited liability partnership shall have at least two designated partners who are individuals and at least one of them shall be a resident in India: Provided that in case of a limited liability partnership in which all the partners are bodies corporate or in which one or more partners are individuals and bodies corporate, at least two individuals who are partners of such limited liability partnership or nominees of such bodies corporate shall act as designated partners |

| 2. | section 7(4) | Every limited liability partnership shall file with the registrar the particulars of every individual who has given his consent to act as designated partner in such form and manner as may be prescribed within thirty days of his appointment |

| 3. | section 7(5) | An individual eligible to be a designated partner shall satisfy such conditions and requirements as may be prescribed. |

| 4. | section 9 | A limited liability partnership may appoint a designated partner within thirty days of a vacancy arising for any reason and provisions of sub-section (4) and sub-section (5) of section 7 shall apply in respect of such new designated partner, Provided that if no designated partner is appointed, or if at any time there is only one designated partner, each partner shall be deemed to be a designated partner. |

| 5. | section 13 | Every limited liability partnership shall have a registered office to which all communications and notices may be addressed and where they shall be received. |

| 6. | section 15 | If the proposed name implies a connection with government or if the name contains a controlled word, it may only be registered with the approval of the Government. |

| 7. | section 21 | Every limited liability partnership shall ensure that its invoices, official correspondence and publications bear the following, namely:-

(a) the name, address of its registered office and registration number of the limited liability partnership; and (b) a statement that it is registered with limited liability. (2) Any limited liability partnership which contravenes the provisions of sub-section (1) shall be punishable with fine which shall not be less than two thousand rupees but which may extend to twenty-five thousand rupees. |

| 8. | section 25 | Where there is any change in the name or address of a partner, file a notice with the Registrar within thirty days of such change. |

| 9. | section 34 | Every limited liability partnership shall file within the prescribed time, the Statement of Account and Solvency prepared pursuant to sub-section (2) with the Registrar every year in such form and manner and accompanied by such fees as may be prescribed. |

| 10. | section 35 | Every limited liability partnership shall file an annual return duly authenticated with the Registrar within sixty days of closure of its financial year in such form and manner and accompanied by such fee as may be prescribed. |

| 11. | section 60 | Compromise or arrangement of limited liability partnerships |

| 12. | section 62 | Provisions for facilitating reconstruction or amalgamation of limited liability partnerships |

CONCLUSION:

It is evident from the amended Act that it focused on smoother operation of LLPs to enable the LLPs to enjoy the privileges currently enjoyed by the Companies under the Companies Act, 2013. They are trying to bridge the gap between Company and LLP’s and to make LLPs more attractive and easier to handle, so that many of the startups today, which prefer the LLP model can also feel equally given the ease of business opportunities.

KEY TAKEAWAY:

It can be concluded from this article that Limited Liability Partnership is the most flexible form of business and offers a much-secured business environment to the partners. The latest amendments proposed through the Bill will provide coverage to a lot of small and large enterprises and provide the benefits of a company as well as traditional partnership firms.

BIBLIOGRAPHY:

http://164.100.47.4/BillsTexts/RSBillTexts/Asintroduced/LLP%20as%20int-E.pdf

https://taxguru.in/corporate-law/key-away-llp-amendment-act-2021.html

https://prsindia.org/billtrack/the-limited-liability-partnership-amendment-bill-2021

*****

DISCLAIMER: The entire contents of this article have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, we assume no responsibility. Therefore, Users of this information are expected to refer to the relevant existing provisions of applicable Laws. We assume no responsibility for the consequences of use of such information. In no event we shall be liable for any direct, indirect, special, or incidental damage resulting from, arising out of or in connection with the use of the information. This is only a knowledge sharing initiative and author does not intend to solicit any business or profession.

*****

About the firm:

Jaya Sharma and Associates is a firm of Practicing Company Secretaries located in Mumbai, Maharashtra, India that specializes in solving the complexities of corporate laws and company secretarial practice promptly and correctly with an attention to detail and personal services catering to pan-India and foreign clients. The peer-reviewed firm specializes and adheres to the parameters of quality control systems and guidelines as prescribed by the regulatory body.

FCS Jaya Sharma-Singhania, Founder & Mentor has been listed as one of the Top Best Ten Women Legal Consultants in India 2021 by Women Entrepreneur Magazine.

Mehul Solanki is a commerce and law graduate having more than four years of working experience in company law compliances, setting-up companies, compliances of listed companies and not-for-profit companies. He is currently Research Associate & Start-up Consultant at Jaya Sharma & Associates and has authored various articles on corporate and securities law related topics which have been published on various websites, blogs and professional magazines including Compliance Calendar, Taxguru, Legal Service India and journal of ICSI etc.

Menakshi Bajaj is a commerce postgraduate and an aspiring Company Secretary currently undergoing her long-term training at Jaya Sharma and Associates, taking interest in understanding and interpreting complexities of the prevailing law and has panned down various articles on corporate law related topics which have been published on various websites namely: Compliance Calendar, Taxguru etc.

Sir kya proprietor ship firm LLP ya Pvt Ltd main Convert ho skti hai Or uska prosess or documents formality kya hai my ph no. Is 8954836339

To convert a Sole Proprietorship into a Private Limited Company, an agreement has to be executed between the Proprietorship and the Private Limited Company (once it is incorporated) for the sale of the business.

Sole proprietorship cannot be directly converted into an LLP. It can be either done by closing the proprietorship and registering an LLP or by including another person in the business and making him a partner and then converting it to an LLP.

For more details your can reach us on corplaw@cs.com or call on 022 2881 8135.