Section 90 of Companies Act, 2013- ‘Register of Significant Beneficial Owners in a Company’

Read with ‘The Companies (Significant Beneficial Owners) Rules, 2018‘ and ‘The Companies (Significant Beneficial Owners) Amendment Rules, 2019‘

The Section and Amendments therein

Hello all, we all know Section 90 of the Companies Act 2013, which was related to the investigation of significant beneficial ownership of shares in relation to the company, was notified w.e.f. 01st April 2014. But, the section came into limelight, when the whole section was substituted and a new Section 90 was introduced through the Companies (Amendment), Act, 2017 which became applicable w.e.f. 13th June 2018.The Companies (Significant Beneficial Owners) Rules, 2018 were also notified on 14th June 2018 along with the introduction of Forms BEN-1 to BEN-4, which were further amended on 08th Feb 2019 and 01st July 2019.

These amendments shifted the entire onus of investigating the significant beneficial ownership of shares in a company, from government authorities to that of the company itself, and cause the company to ensure the compliances. The section specifically provides that a company shall take necessary steps to identify an individual who is a significant beneficial owner of shares in relation to the company, report the details to Registrar and keep a record of the same.

Who is a “Significant Beneficial Owner” (SBO)?

The term is defined by the amended law in a very comprehensive manner. In short, it simply means an individual who owns or exercises control in the company by way of:

- either holding shares or voting rights or having significant influence in excess of 10% of total shares or rights,

- held or exercised either directly by him or indirectly through his relatives or entities in which he has significant influence or both.

It is important to note that a SBO shall be an individual only (either resident or non-resident; whether he is a member of the company or not) and not any other person e.g. firm, company, trust, fund, etc.

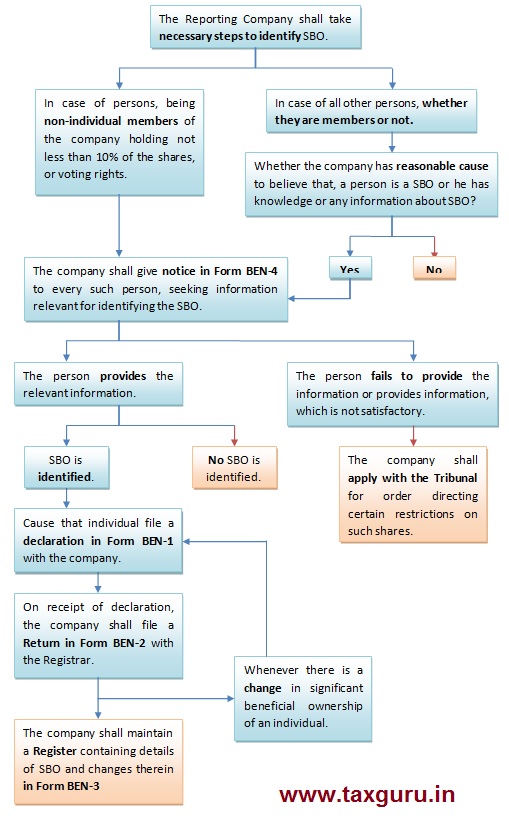

Flowchart explaining the provisions of section 90

I hereby demonstrate the law, through a flowchart given below, how a reporting company would perform its duties (i.e. identify significant beneficial owners (SBO) and report relevant information thereafter to the Registrar) as required by the new provisions, read with the rules, as notified and amended.

Interplay with Section 89 of the Act

If we look deeper, Section 89 comes into light, which also contains provisions regarding beneficial ownership in relation to a company. However, this section puts onus on the persons only (whether they are members or not) to submit the declaration regarding beneficial ownership, if exists, as soon as they receive the shares or acquire the ownership, in Forms MGT-4 or MGT-5 respectively, with the company. On receipt of such declarations, the company shall file a Return with the Registrar in Form MGT-6.

Here, it is important to note that Section 89 contains provisions regarding beneficial ownership, whereas Section 90 contains provisions regarding significant beneficial ownership i.e. in excess of 10% only. Let’s understand this difference with an example given below:

| Person | Beneficial Ownership | Section 89 | Section 90 |

| Mr. A | 7 % | √ | X |

| Mr. B | 12 % | √ | √ |

Further, Section 89 does not contain provisions regarding maintenance of any register by the company, as compared to that of Section 90.

It can be concluded from above comparison that, where the provisions of Section 89 have been complied with and the required MGT forms have been filed, there is no need to take necessary steps as required by the provisions of Section 90, as it would be duplicity of actions only. However, if the company has reasonable cause to believe that, the declarations so given are not satisfactory, then, it should issue a notice in BEN-4 to such persons and follow the provisions contained in Section 90 of the Act.

Exemptions / Relaxations

1. In case of Government Company, Section 89 and Section 90 shall not apply – Notification dated 5th June 2015.

2. In respect to shares of the reporting company, being held by:

(a) Its holding company (provided details are reported in Form BEN-2)

(b) Authority constituted under Investor Education and Protection Fund.

(c) The Government or local Authority.

(d) Any organisation controlled by the Government or Local Authority.

(e) Investment Vehicles regulated by SEBI, RBI, IRDA, and PFRDA.

Summary of relevant Forms

| Section 90, read with relevant Rules | |

| BEN-1 | Declaration given by SBO to the company. |

| BEN-2 | Return of SBO to be filed by the reporting company with the Registrar. |

| BEN-3 | Register of SBO to be maintained by the reporting company. |

| BEN-4 | Notice given by the reporting company to persons (whether they are members or not) seeking details of SBO. |

| Section 89, read with relevant Rules | |

| MGT-4 | Declaration by the member to the company on receipt of shares that he does not hold beneficial interest in those shares. |

| MGT-5 | Declaration by the beneficial owner of shares to the company on acquisition of ownership in such shares. |

| MGT-6 | Return of beneficial interest to be filed by the company with the Registrar. |

I hope, I would be able to clear the doubts regarding the provisions of Section 89 and Section 90 along with their rules notified for that purpose.

Disclaimer

1. He includes she, and his / him includes her.

2. The information and procedures explained in this article are in line with the provisions effective upto the date of publishing of this article. Please check the bare act for any updates thereafter.

3. This article is strictly meant for educational purposes only and shall not be used in any legal matters.

Author Bio

Helpful.

Thank you

Trilochan Sharma

your article was very informative, thank you for putting the efforts and sharing the information. I do have 2 questions:

1. Say there is a company having 9 shareholders, each of them holding more than 10% of shareholding, so the BEN-1 and 2 are required to be filed for each shareholder?

2. Say there is a company in which another company is a member and holds 30% of share. and in that member company, there are 50 share holders, each having less than 10% of share. Is there a need to file BEN-1 and 2?