Hello there, GST has been rolled out but still there are clouds roaming over the status of Goods Transport Agency (GTA) services. I have tried to cover all the topics still any questions are welcomed.

1. Who is GTA?

The term “goods transport agency” has not been defined in either of the GST acts. However, the definition is given in Finance Act, 1994 as:

65(50b) “goods transport agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called.

This definition can be considered under GST regime also until the government does not amend the new law.

2. Does transportation of all goods attract GST?

The answer is NO. The government has carried the following exemption from service tax to GST regime also.

|

||

|

S. No. |

Description of Services |

|

|

22 |

Services provided by a GTA, by way of transport in a goods carriage of: | |

| (a) agricultural produce; | ||

| (b) goods, where consideration charged for the transportation of goods on a consignment transported in a single carriage does not exceed one thousand five hundred rupees; | ||

| (c) goods, where consideration charged for transportation of all such goods for a single consignee does not exceed rupees seven hundred and fifty; | ||

| (d) milk, salt and food grain including flour, pulses and rice; | ||

| (e) organic manure; | ||

| (f) newspaper or magazines registered with the Registrar of Newspapers; | ||

| (g) relief materials meant for victims of natural or man-made disasters, calamities, accidents or mishap; | ||

| (h) defence or military equipments. | ||

It means that if the GTA is transporting above mentioned goods or consignments, then there will be no tax liability under GST regime. However, tax will be payable on goods and consignments other than above.

3. Tax rates applicable to GTA services

If the services include transportation of goods other than mentioned above, then the Tax Rates are as below:

|

Table – B (Applicable Tax Rates) |

|||

|

S. No. |

Description of Services | GST Rate |

ITC |

|

8

|

Services of goods transport agency (GTA) in relation to transportation of goods [including used household goods for personal use] |

5 % |

No ITC |

The services have been put into the lowest tax bracket. However, Input Tax Credit (ITC) will not be available on such services. It will restrict the flow of credit of taxes.

4. SERVICES UNDER REVERSE CHARGE

If a GTA provides services to specified categories of person, then Reverse Charge will be applicable. It means GTA does not need to pay the tax. But, the tax liability will stand with the person who receives such services i.e. the recipient of service.

|

Table – C (Reverse Charge Mechanism) |

||

| S. No. | Service |

Recipient of Service |

|

1. |

Services provided or agreed to be provided by a goods transport agency (GTA) in respect of transportation of goods by road |

(a) any factory registered under or governed by the Factories Act, 1948; |

| (b) any society registered under the Societies Registration Act, 1860 or under any other law. | ||

| (c) any co-operative society established by or under any law; | ||

| (d) any person registered under CGST/SGST/UTGST Act; | ||

| (e) anybody corporate established, by or under any law; or | ||

| (f) any partnership firm whether registered or not under any law including association of persons. | ||

| (g) Casual taxable person located in the taxable territory | ||

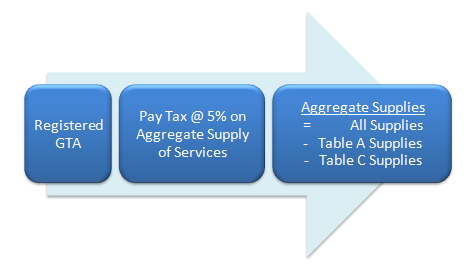

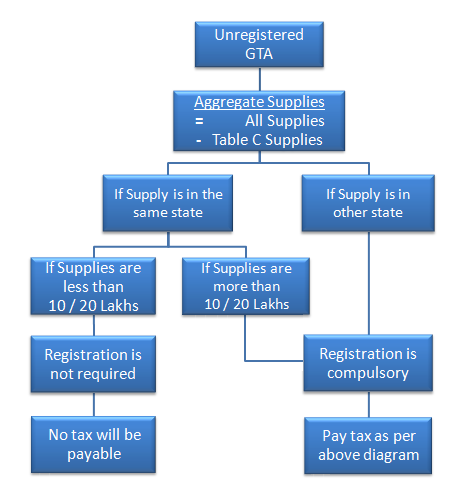

5. So, when GTA need to Register and Pay the Taxes?

Well, the answer to this question varies from person to person. This could be understood from below diagrams:-

(Rs. 10 Lakh Limit for 11 Special Category States :- Arunachal Pradesh, Assam, Jammu & Kashmir, Manipur, Meghalaya, Mizoram, Nagaland, Uttarakhand, Tripura, Himachal Pradesh, and Sikkim)

(Rs. 20 Lakh Limit for all other states and territories)

6. Migration to GST

Sec. 22(2) of the CGST Act says that if a person is already registered in earlier tax regime then it is mandatory for him/her to register into the new tax regime.

It implies that if the GTA is already registered under Service Tax then he is required to migrate into the GST regime.

However, if as per the provisions of GST, he/she has migrated but is not required to register under GST, then he/she can opt of cancellation of registration.

Also Read- GTA Services under GST Regime (Part 2)

Author Bio

under reverse charge mechanism the service receiver is eligible to take itc or not sir.

under reverse charge mechanism the service receiver pay the tax, whether it is eligible for itc.

Can a Manufacturer avail the ITC On GTA under Reverse charge ( After GST paid on GTA) against the output tax liability of GST on supply of goods?

If we pay the GST on GTA services under reverse charge, would ITC be available on such services. In other words “No ITC” is only for GTA services provider or it is also applicable on gst paid on reverse charge