Employee Stock Option Plan (ESOP) – Companies Act, 2013 for un-listed Companies

1. Objective of issuing ESOP :- The objective of issuing ESOP is to:

A. Provide incentive to retain and reward employees of the company based on their contribution.

B. Motivate employees to contribute to the growth and profitability of the company in future as well.

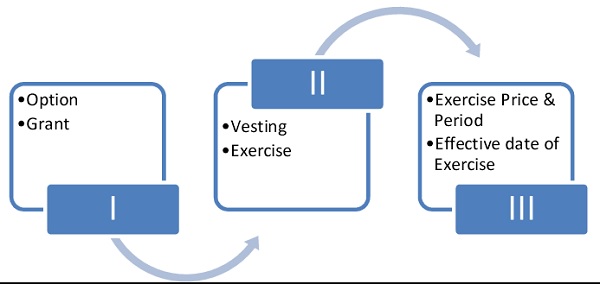

2. Important Terms and flow of actions:-

Important to Note: ESOP

A. OPTION: – a right but not an obligation – to purchase the shares of the company on the fulfillment of the conditions mentioned in the ESOP plan at the price decided at the time of grant of options.

B. GRANT :-The eligibility of a particular employee (depending on the criteria set) for grant of stock options based on his role and performance is known as grant of option

C. VESTING:- Vesting has two components – Vesting percentage and vesting period. Vesting period is the period on the completion of which the said portion can be exercised. Vesting percentage refers to that portion of total options granted, which the employee will be eligible to exercise.

D. EXERCISE: – The activity of converting the options granted to an employee into shares by paying the required exercise price is known as exercise of options.

E. The effective date of exercise is the date on which the Company allots the shares.

F. The companies have freedom to determine the exercise price in conformity with the applicable accounting policies, if any.

G. There shall be a minimum period of one year between the grant of options and vesting of option.

H. The company shall have the freedom to specify the lock-in period for the shares issued.

3. Applicable Rules and Regulations: – Sec 2(37) of Companies Act, 2013 defines “employees stock option” read with Sec 62(1)(b) of Companies Act, 2013 and Rule 12 of the Companies (Share Capital and Debentures) Rules, 2014. This Rule specifies that on complying certain terms and conditions only the unlisted company can offer shares to its employee’s under ESOP.

These are as follows:

A. Sanction by Special Resolution

B. Employees to whom ESOPs may be issued

C. Disclosures in the explanatory statement annexed to the notice for passing of the resolution.

D. Pricing

E. Shareholders’ approval by way of separate resolution in case of holding or subsidiary or more than 1% of issued capital

F. Variation of terms of ESOS through special resolution in case not yet exercised the options.

G. Minimum vesting period

H. Lock-in-period for shares issued on exercise of option

I. Right to receive dividends

J. Forfeiture/ Refund of amount paid by employees under ESOP

K. Options not transferable

L. Who can exercise the option

M. Disclosures in Board of Directors Report- Employees Stock Option Scheme: (a) options granted; (b) options vested; (c) options exercised; (d) the total number of shares arising as a result of exercise of option; (e) options lapsed; (f) the exercise price; (g) variation of terms of options; (h) money realised by exercise of options; (i) total number of options in force; (j) employee wise details of options granted to;- (i) key managerial personnel; (ii) any other employee who receives a grant of options in any one year of option amounting to five percent or more of options granted during that year. (iii) identified employees who were granted option, during any one year, equal to or exceeding one percent of the issued capital (excluding outstanding warrants and conversions) of the company at the time of grant;

N. Register of Employees Stock Options

4. ESOP Scheme: – It is most important documents, which is approved by the Board and Shareholders of the company.

This should have the answers of all the following queries:

- the total number of stock options to be granted;

- identification of classes of employees entitled to participate in the Employees Stock Option Scheme;

- the appraisal process for determining the eligibility of employees to the Employees Stock Option Scheme;

- the requirements of vesting and period of vesting;

- the maximum period within which the options shall be vested;

- the exercise price or the formula for arriving at the same;

- the exercise period and process of exercise;

- the Lock-in period, if any;

- the maximum number of options to be granted per employee and in aggregate;

- the method which the company shall use to value its options;

- the conditions under which option vested in employees may lapse e.g. in case of termination of employment for misconduct;

- the specified time period within which the employee shall exercise the vested options in the event of a proposed termination of employment or resignation of employee.

Author Bio