ESOP vs Sweat Equity – EMPLOYEE RETENTION MECHANISM-INSTRUMENT

About the Article

This article throws light on the situation pertaining to the aspect of employee retention for basic start up business and businesses which are already established. Promoters today have huge cost of retention and gone are those days when people stay for 30-40 years in a company i.e from their young 20’s to their super annuation 60; today we see the attrition is quite high each one prefers to jump from one company to another where there is decent growth rate. Human resource is such an important area which cannot be neglected today as the famous saying goes “Employees First, Customer Second and Investors are the last”. This article will try to help the reader find out what could be the best instrument which they can use to help retain some of the talents in their own office without losing them, as training the new employees involves, cost, time and lots of resources which again becomes a financially taxing one. The journey through this article shall be in the form of preface, learning about ESOP and Sweat Equity their regulatory and company impact angles, comparison between the two instruments and finally the conclusion.

Before we start and dwell on performer retention aspect let us discuss why this is necessary? Technically because of the fact that growth of the company largely depends on the continuity of such people and also because of the fact that it helps them to get motivated and feel part of the whole process of progress.

Coming to the moot point start ups are usually quagmired by the fact of paying employee salaries which is a fixed burden to the company and also it hits bottomline (PAT- Profit After Tax) adversely on account of the fact that profit shrinks due to the huge burden of providing them a fixed pay, deducting TDS (Tax Deducted at Source) having PF registrations remittance of the same is a compliance burden for the company considering the fact that it is a start up. Secondly when the person are made employees without a considerable salary a omnipresent question that comes up in almost all the board meeting with VC / Angel Investor funding a start up and having a board seat is that how will you have a control on the employee what would actually motivate him or her to stay with the company why should a performer who is performing excellently well be associated with the company ( Please note here we are discussing about start ups who find it increasingly difficult to hire a talent which would take above the market price bidding for them to digest in the company).Now to do away with this, the only option left with the company is to either take their service as employees in initial stages and if there is a significant value addition say in the form of an IPR / Depreciable Asset then on such instance sweat equity can be given to them provided they have worked in the company for a year atleast in the form of a permanent employee. For established companies the preference of ESOP goes up on all likelihood in order to exercise greater control on employees for mapping their performance management; here the concept of permanent employee comes up. Further there are more compliances such as establishment of trust to be followed depending on the type of company (Public Limited).

Coming to the moot point start ups are usually quagmired by the fact of paying employee salaries which is a fixed burden to the company and also it hits bottomline (PAT- Profit After Tax) adversely on account of the fact that profit shrinks due to the huge burden of providing them a fixed pay, deducting TDS (Tax Deducted at Source) having PF registrations remittance of the same is a compliance burden for the company considering the fact that it is a start up. Secondly when the person are made employees without a considerable salary a omnipresent question that comes up in almost all the board meeting with VC / Angel Investor funding a start up and having a board seat is that how will you have a control on the employee what would actually motivate him or her to stay with the company why should a performer who is performing excellently well be associated with the company ( Please note here we are discussing about start ups who find it increasingly difficult to hire a talent which would take above the market price bidding for them to digest in the company).Now to do away with this, the only option left with the company is to either take their service as employees in initial stages and if there is a significant value addition say in the form of an IPR / Depreciable Asset then on such instance sweat equity can be given to them provided they have worked in the company for a year atleast in the form of a permanent employee. For established companies the preference of ESOP goes up on all likelihood in order to exercise greater control on employees for mapping their performance management; here the concept of permanent employee comes up. Further there are more compliances such as establishment of trust to be followed depending on the type of company (Public Limited).

Also there is another route for start ups; which most likely is not a route which is to be preferred that is allotting shares other than cash under the preferential allotment rules all facets of compliance pertinent to section 42 and section 62 read with the rules have to be followed. Start up which goes for aggressive rounds of funding will usually have marked up share values so in such cases careful examination of valuation ought to be done.

Prima Facie in this write up we will look on the parts of compliance and taxation angles in detail to enable the reader to arrive at a favorable conclusion based on their individual situation.

Going by the above let us first discuss on ESOP and find out what the current companies act 2013 (‘the Act’) with its rules entails for the start ups.

ESOPS:

ESOPS can be offered to the employees of the companies as per section 62(1)(b) of the act. Now it is pertinent to note as to who are defined as employees as per the companies act 2013.

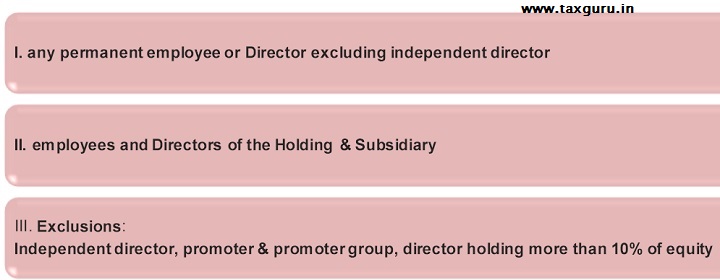

As per explanation to sub-rule 1 of Rule 12, Employee means –

(a) a permanent employee of the company who has been working in India or outside India,; or

(b) a director of the company, whether a whole time director or not; or

(c) an employee or a director as defined in sub-clauses (a) or (b) above of a subsidiary, in India or outside India, or of a holding company of the company.

To break it in to simpler terms, from the above we are absolutely clear that a Permanent Employee means someone who is on rolls of the company. There is no minimum time period prescribed though. It is also very interesting to note that employees and directors of holding or subsidiary are also covered above. Going with the aforesaid directors whether or not they are full time directors whether or not they are executive / non executive directors are all eligible for the same; only condition being independent directors can’t be part of the process.

ELIGIBILITY CRITERIA

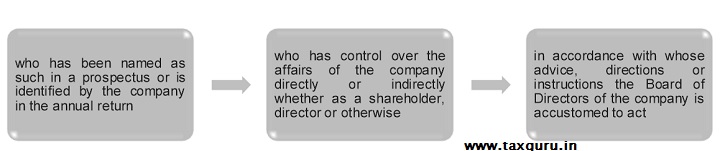

Also take note that promoters cannot be given ESOPs, to know more as to who is a promoter ref the fig below

What form of control can be exercised by the promoters on the employees:

Assurity of employee continuing in an organisation minimum of a year:

Minimum vesting period of one year is required after issue of ESOP this is as per sub-rule 6(a) of Rule 12. The company can prescribe longer vesting periods there by these sweeteners ensure longer continuation of the said employees. So this means that the promoters are assured of the services of employees minimum of a year atleast. Only after completion of vesting period, shares can be applied for.

Post the allotment of shares, ESOP lock-in and other restrictions can be enforced in ESOP scheme by the board however this is subjected to approval at the EGM. Scheme related restrictions are not provided in the act but this can however be implemented by the company as per its internal by laws

Valuation / pricing aspects

Freedom to determine the price as per sub-rule 3 of Rule 12 but only provision to look into is that the price shall be in conformity with the applicable accounting policies.

Sweat Equity

When it comes to sweat equity there is a little differentiation between who are actually eligible for it as laid down under explanation to sub-rule 1 of Rule 8 the following people are eligible for the same: –

ELIGIBILITY

“I.

a) Permanent employee of the Company who has been working in India or outside India, for at least last 1 year

b) Director of Company-Whole time director or not

c) An employee or a director as defined in sub-clauses (a) or (b) above of a subsidiary (in India or outside India) or of a holding Company.

II.

The expression value additions means actual or anticipated economic benefits derived or to be derived by the company from an expert or a professional for providing know how or making available rights in the nature of intellectual property rights by such person to whom sweat equity is being issued for which the consideration is not paid or included in the normal remuneration payable under the contract of employment in the case of an employee’’

Shareholders Approval–A special resolution is required in this regard and a point worthy to be noted is that within 12 months of passing such a resolution the allotment of shares ought to be done. Another point that captures the attention is sweat shares cannot be a new class of shares which means only an existing class of shares can be offered as sweat shares with no additional rights or preferences.

- Time line – A year should have lapsed between the commencement of business and issue of such shares.

- Valuation– For the purpose of issue of shares the valuation ought to be done by the registered valuer and further if there is an intellectual property which forms part of the whole deal then such IPR should also be valued to arrive at FMV of the shares

The report so obtained has to be circulated and should form part of the notice to be sent out to the shareholders to pass such resolution.

Accounting Aspect – This can be best described in the form of a pictorial representation.

a) If non-cash consideration takes a form other than depreciable or amortizable asset- – Shall be expensed as provided in the accounting standards.

Details to be furnished in the Directors Report- The board shall disclose the following in the boards report:-

a) The class of director or employee

b) Class of shares issued as sweat equity shares

c) Reasons for such issue, terms and conditions of such issue,total number of shares arising post such issue,% of sweat equity in total post and paid up capital, to whom it is issued ( directors,kmp/other employees), consideration (including other than cash) received or benefit accrued to the company, diluted EPS post such issue.

Register of Sweat Equity Shares– Company shall maintain a register of sweat equity shares in form no SH.3 and shall enter the particulars of sweat equity shares as entailed in sub-rule 14(a) of Rule 8. The enteries so made shall be authenticated by the company secretary or such other person who is authorized by the board.The Register shall be maintained at the Registered office of the company or such other place as may be decided by the board.

Comparative Analysis of ESOP and Sweat Equity

| ESOP | Sweat Equity Shares | |

| Employee | The term employee is defined in the rules | The term employee is defined in the rules |

| Permanent Employee | As per ESOP related rules no minimum of 1 year prior work in the company is necessitated | In this Permanent Employee means one who has already worked in the company for 1 year. |

| Exclusion of Independent Director | Under ESOP rules an independent director is specifically excluded .This means he is not entitled to it | There is no such exclusion given under the rules for independent directors. |

| Allotment | ESOP Allotment are based on completion of vesting period and also based on the performance. | Sweat Equity Shares are allotted immediately with no such vesting period prescribed under the act. |

| Promoters | Specific Exclusion of promoters and promoter group from the ESOP | No such exclusion has been given under this so even the promoters can ask for sweat equity shares. |

| Existing holder’s eligibility | If the above said director holds 10% or more shares prior to the ESOP then they become ineligible for the said process | Indirect control of total holding to the maximum of 25% at any given point of time |

| Dilution of exiting investors | Dilution happens on the basis of completion of vesting period and on the exercise of the options. | Dilution happens on account of immediate shares being allotted to the persons covered under the section 54 |

| Lock in post allotment for transfer of shares | No such criteria prescribed as per act or rules | 3 years |

| Maximum Cap for ESOP | No such % cap in ESOP | There is a prescribed maximum of 25% as a total of paid up capital in the company’s life time and a maximum yearly cap of 15% or 5cr of issue value whichever is higher. |

Conclusion:

A committee set up by the government to review issues arising out of implementation of the Companies Act, 2013 has suggested the limit on sweat equity for start ups could be raised to 50% from 25% of paid up capital, improving the incentives for innovators and giving a boost to the Startup India initiative.

The government may also allow issuance of ESOPs to promoters working as employees or whole time directors of startups, which would help promoters to gain from increase in future valuation.

Nonetheless what ever may be the outcome the above addresses the retention aspects for a company.

ABOUT THE AUTHOR

Mr. K. Gaurav Kumar is an Associate Member of ICSI with an MBA (Finance) Full time graduate from the Loyola Institute of Business Administration, Chennai. He has vast experience in the secretarial field and consulting.

Mr. K. Gaurav Kumar is an Associate Member of ICSI with an MBA (Finance) Full time graduate from the Loyola Institute of Business Administration, Chennai. He has vast experience in the secretarial field and consulting.

He has been actively involved in various client engagements involving billion dollar companies and also covering varied line of business. He is also an active contributor to SIRC’s Newsletters of ICSI. He is also an active speaker at various professional forums and has been a recipient of various awards for his contributions towards the knowledge sharing quotient pertaining to his domain expertise.

He has worked with one of the big fours in the consulting division and gained vast experience in connection with Company Law and Foreign Exchange Management Act.

(Author is a chennai based practicing company secretary he can be reached at csgauravkumarjain@gmail.com)