Goodness is the only investment that never fails – Henry David Thoreau, American writer.

“Give and take” is a way of getting things done in a desired manner. When we give something, we expect something. A mom dictating a child to finish her homework gets a likely response “If I will finish this, will you give me a chocolate?” Similar was the expectation of the corporates regarding the allowance of expenditure incurred for fulfilling their social responsibilities as per the mandate of the Companies Act, 2013.

Probably for all those individuals and organisations dealing with CSR issues the most frequently asked question is the obvious – just what does ‘Corporate Social Responsibility’ mean anyway? Is it a stalking horse for an anti-corporate agenda? Something which, like original sin, you can never escape? Or what?

Different organisations have framed different definitions – although each definition that currently exists underpins the impact that businesses have on society at large and the societal expectations of them.My own definition is that CSR is about how companies manage the business processes to produce an overall positive impact on society.

The United Nations Industrial Development Organisation (UNIDO) has defined corporate social responsibility (CSR) as:

A management concept whereby companies integrate social and environmental concerns in their business operations and interactions with their stakeholders. CSR is a way in which companies achieve a balance of economic, environmental and social imperatives.

CSR in India was an activity that was performed but not deliberated.In order to streamline the philanthropic activities and ensure more accountability and transparency, the government of India made it mandatory for companies to undertake CSR activities. The Ministry of Corporate Affairs notified Section 135 and Schedule VII of the Companies Act 2013 as well as the provisions of the Companies (Corporate Social Responsibility Policy) Rules, 2014 to come into effect from April 1, 2014 which is as follows:

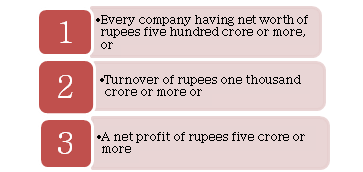

1. Every company having net worth of rupees five hundred crore or more, or

2. Turnover of rupees one thousand crore or more or

3. A net profit of rupees five crore or more

During any financial year needs to spend at least 2% of its average net profit for the immediately preceding three financial years on corporate social responsibility activities.

Let us first have a glimpse of the type of expenditures which are treated as CSR expenditures as per Schedule VII of the Companies Act, 2013:

- Eradicating hunger, poverty and malnutrition, promoting preventive healthcare,

- Promoting education and promoting gender equality,

- Setting up homes for women, orphans and the senior citizens, measures for reducing inequalities faced by socially and economically backward groups,

- Ensuring environmental sustainability and ecological balance, animal welfare,

- Protection of national heritage and art and culture,

- Measures for the benefit of armed forces veterans, war widows and their dependents,

- Training to promote rural, nationally recognized, Paralympic or Olympic sports,

- Contribution to the prime minister’s national relief fund or any other fund set up by the Central Government for socio economic development and relief and welfare of SC, ST, OBCs, minorities and women,

- Contributions or funds provided to technology incubators located within academic institutions approved by the Central Government,

- Rural development projects,

- Slum area development.

All the companies which are covered u/s 135 of Companies Act 2013 are required to disclose CSR expenditure during the year in its Board’s report as per the format given in Companies (Corporate Social Responsibility Policy) Rules, 2014

ADMISSIBILITY OF CSR EXPENDITURE

Whether a particular expenditure spent on CSR will be allowed under the Income-tax Act for the company will depend upon the nature of expenditure itself.In most of the cases which are not falling under the revenue expenditure, the Income Tax Officer will disallow these expenses.The company which is covered under the CSR Rules, will have to chalk out and analyse whether the expenditure to be incurred will be done in a tax efficient manner?

To quote an example, if a company donates towards Prime Minister’s National Relief Fund, the entire donation is allowed to be deducted from the taxable profits but one is not sure the same company if it constructs an educational institution in a village near its factory, whether tax benefit would be extended, although promotion of education is covered under the CSR activity under Schedule VII.

If we see the case laws of past years it shows ambiguity, for example in the case of CIT Vs Infosys Technologies Ltd (2014) (360 ITR 714) the Karnatka high court allowed the expenditure incurred for installing traffic signal by company under social initiative. Court said the traffic signal used by its employee so it relates to business activity hence allowed u/s 37(1)

But in the case of CIT Vs.Wipro Ltd (360 ITR 658)(kar) expenditure for community development near its factory ,court does not find any nexus for its business activity hence disallowed such expenditure u/s 37(1).

Section 37 of income Tax Act, 1961 is a residuary section which allows deduction of business expenditures not covered specifically under sections 30 to 36. Since the admissibility of CSR expenditure as business expenditure under section 37 was not clear due to differing Court rulings, the Budget proposals were expected to clarify the same, which it did, however not in the interest of the corporate sector.

In order to clarify, the Finance (No.2) Act, 2014 has inserted an Explanation to section 37 which is reproduced as under:

“Explanation 2.—For the removal of doubts, it is hereby declared that for the purposes of sub-section (1), any expenditure incurred by an assessee on the activities relating to corporate social responsibility referred to in section 135 of the Companies Act, 2013 shall not be deemed to be an expenditure incurred by the assessee for the purposes of the business or profession.”

But as per the Companies (Corporate Social Responsibility Policy) Rules, 2014 it has been clarified in rule 4(1)that CSR spends excludes “activities undertaken in pursuance of the normal course of business of the company”

All this long and flowery explanation definitely demands an example.

XYZ Ltd. Is a company that manufactures hand sanitizers and falls within the ambit of section 135 and hence is required to fulfill its social responsibility. For the purpose of which it launched a healthcare campaign in which it distributed free hand sanitizers to ensure and promote well-being and hygiene of the society. Since this expenditure amounted to brand building, the company claimed the same as expenditure u/s 37(1) of Income tax Act, 1961. Now the question arises that whether such expenses be allowed?

Since all the CSR expenditure incurred by the company during the year subject to the activities specified in schedule VII of Companies Act, 2013 are required to be disclosed in the Board’s report and once such expendituresare declared as CSR expenditure then they cannot be claimed as expenditure u/s 37 of Income Tax Act as it does not deems such CSR expenditures as expenditures incurred for the purpose of business. Whereas on the other hand, Companies Rules requires that CSR spends should exclude activities undertaken in pursuance of the normal course of business of the company.

This seems to indicate that the Government wants to eat the cake and keep it too.

The memorandum explaining the provisions of the Finance (No.2) Bill, 2014 clearly provides that:

If such expenses are allowed as tax deduction, this would result in subsidizing of around one-third of such expenses by the Government by way of tax expenditure.

DOORS FOR CSR EXPENDITURE – CLOSED OR PARTIALLY OPEN?

With the introduction of explanation II in section 37, CSR expenditures are not allowed only u/s 37. Which means that apart from section 37,certain sections, within sections 30 to 36 of the Income-tax Act, 1961 provide for specific deductions in respect of certain expenditures which are NOT business expenditures in true sense. In case the expenditure incurred in accordance with the provisions of section 135, read with Schedule VII of the Companies Act, 2013 fulfils the requirements of these sections, they would automatically get a deduction for such expenditure under the provisions of the Income tax Act.

Hence, as per the present understanding of the law, some of the options available to the corporates for claiming benefit under the provisions of Income-tax Act, 1961 are as follows:

| Income Tax Section | Tax treatment of expenditure & Quantum of deduction |

| Sec 80G | Donation directly or to registered NGO or to PM national relief fund,or for promoting family planning etc. 100% (50% in some cases) of such deduction allowed . Donation in kind is not allowed. |

| Sec 35AC | Expenditure incurred on project or scheme for promoting the social and economic welfare or up liftment of the public as approve by the national committee set up for this purpose ,100% of such expenditure is admissible.But the activity of association whom the donation made should be stated under Schedule VII of comp Act. |

| Sec 35 CCD | Expenditure on skill development project as notified by the board is eligible with weighted deduction of 1.5 times of such expenses. |

Considering available options, the corporates may think and act on the following lines:

Corporates already expending on CSR activities through creation of trusts and institutions, etc., will continue since they are already set-up and might be claiming exemptions under sections 11 and 12 of the Income-tax Act, 1961.

Investing in sections 35CCD and 35CCC activities may still be unpredictable, since there are no precedents and no clarification has been issued by the Ministry of Corporate affairs as to whether the same will be considered as an expenditure on CSR activity?

Agriculture based companies might claim expenditure mentioned in section 35CCC (expenditure on agricultural extension project). Since it may amount to expenditure undertaken in respect of activities in course of business, it is doubtful as to whether such expenditure would be considered as an expenditure on CSR activity under section 135 of the Companies Act, 2013?

Creation of trust and society while complying with the requirements of the Companies Act, 2013 and also Income-tax Act, 1961 for claiming exemptions under section 80G as also under sections 11 and 12 is a challenging task in itself.

Investing in trusts and societies registered under section 12AA would provide a benefit under section 80G only of 50% of the contribution made, which is not a very attractive proposition.

Legal and procedural hassels in getting approvals/registrations, etc., might keep the corporates away from real CSR activities.

From the view point of corporates, Contribution to the Prime Minister’s National Relief Fund is the easiest and the safest mode of investing in CSR activities.

NO CHANGE PROPOSED IN MAT PROVISIONS – A BLESSING IN DISGUISE

The statement of Profit and Loss as per Schedule III to the Companies Act, 2013 does not consider CSR expenditure as appropriation of profits and, thus, allows it as business expenditure while computing profits. This profit as per Companies Act, 2013 forms basis of MAT provisions under section 115JB of the Income-tax Act, 1961. Since there is no budget proposal to add back this CSR expenditure for the purpose of computation of MAT under section 115JB of the Income-tax Act, 1961, the same has come to the advantage of the coporates. Since such expenditure is 2% of the profits, the corporates falling under the MAT regime are expected to make huge tax savings on this ground. This inconsistency between two laws, no doubt, will be located and plugged in soon.

CONCLUSION

Considering the prevailing economic scenario, one can be sure that in no case a corporate will incur expenditure on CSR activities for which it is not able to claim tax benefit. But the larger question that arises is: Whether the whole purpose of mandating CSR activities is lost, since majority of corporates may opt for contributing to Prime Minister’s National Relief fund and thereby, relieve themselves of their further accountability to ensure proper utilisation of funds towards CSR activities. While the concerns of both, the Government and the corporate assessees, are appreciable, it is felt that something more needs to be done. Even though allowing this expenditure as business expenditure is not the solution, not providing benefit to the person sharing the responsibility is also not right. Infact, there is a need to provide more options in the Income-tax Act, 1961 so that the corporates are incentivized to invest directly in CSR activities. Since our Hon’ble Prime Minister is capable of finding a way out for every problem, we are sure something would be done in the coming “happy and good days”.

Hi,

Is an in-kind donation by a company under their CSR of new electronic kits for children to a trust eligible for any tax benefit?

Maam,

Company provide a vehicle to NGO as CSR.

If that vehicle expencess like repairs also covered in CSR or not?

Are expenses relating to CSR activities like travelling or Dearness allowance or dining & lodging expenses considered as CSR expenses?

approved charities/funds. correction required.

The summum bonum of the above writeup is that CSR activities related to assessee business only are allowed deduction u/s 37. One can claim deduction U/s 80G if donated to approved chities/funds.

well explained and highly informative article and very useful to readers. please send your other article through my email-id. cwaabhimanyu@gmail.com

Nice and insightful article.

Thank you Nitisha for your effort.

very good article

Theoretically speaking, income tax is an immoral tax as it is imposed on surplus remaining with persons AFTER they have paid numerous indirect taxes. Worse, it has a graded system which violates the principle of equality before law.

Mandatory imposition of CSR and then non- deduction of such expense under income tax has taken such immoral stance to a new high level. Tom-tomming about reduction in corporate taxes in very budget by BJP govt and then increasing tax rates instead has left enterprises gasping and its supporters stunned and angry. Similar is the case of Swachh Bharat Cess. Finance Minister will prove to be a proverbial trojan horse in BJP camp.

A very informative article. Was wondering how and what my company is doing under CSR and what all Tax exemptions they are getting.