Ministry of Corporate Affairs vide its notification dated 13/06/2018, had notified the Companies (Significant Beneficial Owners) (SBO) Rules, 2018 along with Section 90 of the Companies Act, 2013 as amended by the Companies Amendment Act, 2017 to eradicate money laundering and to unmask the hidden owners of the company.

Further,On 08.02.2019 M.C.A has revised the SBO rules. The Rules will be effective from the date of their publication in the Gazette of India.

The purpose of this article is not to reiterate the provision rather to highlight Critical Aspect of SBO or to address the Key Issues.

Terminology

Reporting Company: means a company as defined in clause (20) of section 2 of the Act, required to comply with the requirements of section 90 of the Act.

Control : shall include the right to appoint majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner.

Majority stake: means;-

(i) holding more than one-half of the equity share capital in the body corporate; or

(ii) holding more than one-half of the voting rights in the body corporate; or

(iii) having the right to receive or participate in more than one-half of the distributable dividend or any other distribution by the body corporate;

Critical Aspect of SBO are discussed below:

a.) Exemption for Subsidiaries Companies

1.Rule 8 of the SBO rules, have granted exemption to subsidiary of Indian Holding Companies which are reporting SBO under Section 90 of the Act .The exemption is upto the shares held by those holding companies in subsidiary company.Thus, it is clear that Subsidiaries company are not totally exempted and shall need to carry on the exercise for finding SBO for the remaining percentage of shareholding .

For Ex:

A Ltd holds 52% share of BLtd ,then BLtd shall fill BEN-2 for Holding Reporting Company for 52% holding , and need to carry on the process for finding SBO for the rest 48% .

2.Whether such companies are required to issue BEN-4 as stated in Rule 2A, the answer would depend upon the status of Subsidiary company, as a wholly owned subsidiary would be not be required to issue BEN-4 as all the shares are held by a Indian Company .But for the rest it would be mandatory.

3.Addressing the issue for BEN-2 filing for Subsidiary Company, As the provision of the rules are not applicable on subsidiaries of holding reporting company, Subject to filing of BEN-2 for their holding reporting company, there is no need to take BEN-1 from the Holding Company, but a clarification may be furnish or attached to satisfy filing need of the eform.

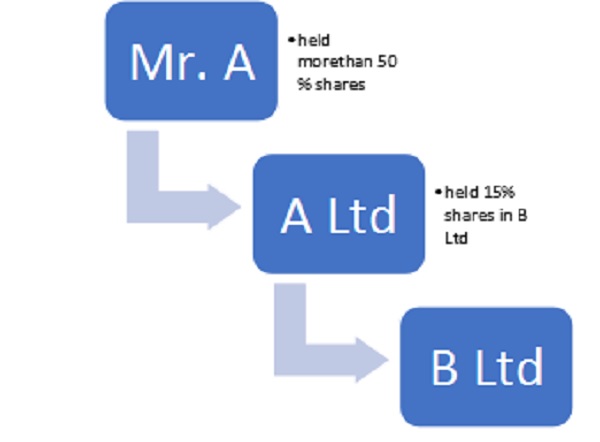

b.) Majority Stake and Calculation of Indirect Holdings.

Most of us are clueless how to calculate indirect holding for a SBO or relying upon proportioning the holding ,Let me tell you that ,it totally incorrect and its not prescribed manner for calculating SBO. Rules have made very clear that in case where member is a Body Corporate the person holding majority stake in such body corporate shall be a SBO ,In other words a Individual controlling a body corporate via its holding of more than 50% , shall be in position to control the total holding of the body corporate in SBO.

In above case, Mr. A would indirectly be holding 15% in BLtd as he holds majority stake and can easily control A Ltd.

c.) Whether is a SBO or not ?

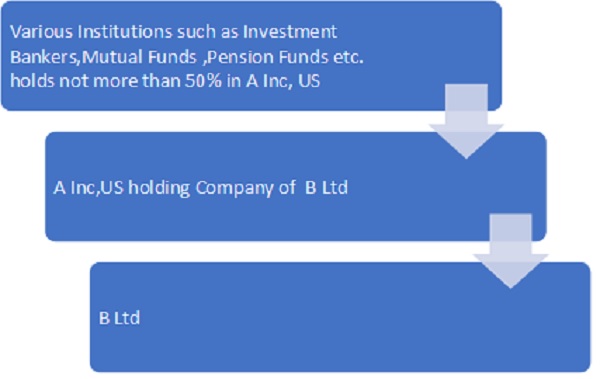

There might be some cases where a Reporting Company is belongs to Multination Corporation whose has no Individual who holds majority stake in the Ultimate Parent Company well in that case,These Companies are professionally managed and has no identifiable promoter like L&T ,in India. There would no requirement to file BEN-1 or BEN-2 as there is no SBO and the earlier provisions has relating to furnishing of BEN-1 by Senior Management Personnel of Ultimate Holding Company has been done away. A pictorial representation has been made below.

d) Impact of any Indirect holding

The definition of SBO clear states,

“(i)holds indirectly, or together with any direct holdings, not less than ten per cent. of the shares;

(ii) holds indirectly, or together with any direct holdings, not less than ten per cent. of the voting rights in the shares;”

Means, if an individual directly holds 9.5 % shares in his name and holds 0.5 % of shares through Body Corporate, HUF ,Trust or Partnership and other conditions relating indirect established for these entities than after clubbing of direct and indirect holdings , he will be consider as SBO.

Because if we go by definition, such person has indirect holdings which triggers the section and demands disclosure

e.) Person Acting Together

As per the Explanation V “- For the purpose of this clause, if any individual, or individuals acting through any person or trust, act with a common intent or purpose of exercising any rights or entitlements, or exercising control or significant influence, over a reporting company, pursuant to an agreement or understanding, formal or informal, such individual, or individuals, acting through any person or trust, as the case may be, shall be deemed to be ‘acting together.

Thus, litmus test for any person for acting together would be the “common intent” and not the relation which might be difficult to interpret and depend upon case. This is the most grey area in SBO, because a individual may not be holding majority stake in a body corporate alone but through its relatives ,he may be. So we need to check whether a set of Individuals are acting together for controlling the entity or not.

Disclaimer; The views presented in this article is solely personal and not of my organization for which, I work for. Readers are advised to refer relevant provision. The views expressed are not binding on anyone and just for informative purpose.

Author Bio