Since the Ministry of Corporate Affairs is keen to move its attitude towards social development, they inserted a welcome provision of “CORPORATE SOCIAL RESPONSIBILITY” wide section no. 135 in new companies act, 2013.

As compared to previous act there was no such provision in the act i.e. Companies act, 1956. So it is really a great initiative by the government.

Section 135 of Companies act, 2013 provides that

1. Every company, or

2. Its holding or subsidiary, or

3. Foreign Company as per 2(42) of companies act, 2013,

Having

1. Net worth > Rs. 500 Cr. Or more,

2. Turnover > Rs. 1000 Cr. Or more,

3. Net profit > Rs. 5 Cr. Or more

During any financial year shall require to constitute a CSR Committee.

Exclusion:-

If any company having CSR committee cease to fall within the provision of Sec. 135(1) for three consecutive years then such company

1. Is not required to constitute CSR committee

2. Is not required to comply with the provisions of sec. 135.

Composition of CSR Committee:-

1. CSR Committee shall comprise

– 3 or more directors

– Out of which at least 1 shall be Independent Director (ID).

2. Unlisted Public Company or Private Company which are not require to appoint ID shall constitute the said committee without ID

3. Private Company having only two directors can have two directors in CSR committee.

4. In Case of Foreign Company

– 2 person shall be there in the committee,

– One shall be resident,

– Another shall be nominated by Foreign Company

DUTIES OF CSR COMMITTEE:-

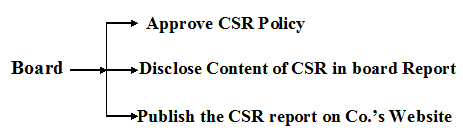

DUTIES OF BOARD:-

Content of CSR Policy:

CSR Policy formulated and recommended by board shall include

1. List of CSR projects and programs within the preview of Schedule VII of Companies Act,2013,

2. Monitoring process of such programs,

3. CSR activities should not include the activities that are undertaken in normal course of business by companies,

4. Board must ensure that activities included in CSR policy must relates with the activities included in Schedule VII,

5. Policy should state that surplus arising from such activities shall not form part of business profit.

Amount of CSR Expenditure:

2% of Average profit of the Amount of

Company during 3 immediate = CSR Expenditure

Preceding financial year

Note: – Net Profit shall be in accordance with the provision of Section 198 of the Companies act, 2013

Calculation of Net Profit for the purpose of CSR

| Particulars | Amount(In Cr.) |

| Net Profit Before tax as per books FY 2013-14 (A) | 1,000 |

| Net Profit Before tax as per books FY 2012-13 (B) | 750 |

| Net Profit Before tax as per books FY 2011-12 (C) | 500 |

| Total (A+B+C) (D) | 2,250 |

| Average Profit D/3 (E) | 750 |

| CSR Expenditure 2%*(E) | 15 |

Following points should be considered

1. Preference shall be given to local area in which company operates,

2. Reason shall be given in board’s report if company fails to spend such amount in the financial year.

3. Branch profits & dividend received from a company covered u/s 135 shall not be included in the profit,

4. For any financial year if Fin. Stat. Are prepared in accordance with the provision of Companies act 1956, then profit need not to be calculated further.

Rules Regarding CSR Activities:-

Followings are the rules applicable while carrying out CSR activities

1. Activities shall be undertaken by company as it mentioned in CSR policy excluding activities under taken in normal course of business

2. CSR Activities can be undertaken by company with its holding or subsidiary company through

-Registered trust, or

-Registered Society, or

-Section 8 company or with its holding or subsidiary or associate company.

(Note:- These Companies are required to have a track record of three years of undertaking the similar activities.)

3. CSR activities can be done with the collaboration of other companies. Provided both companies should be in the position to report separately on such projects or programs in accordance with these rules,

4. Companies may build CSR capacities if their own personnel as well as those of implementing agencies with established track record of 3 years. Such expenditure shall not be more than 5% of total CSR expenditure of a company in a financial year.

5. Direct/indirect contribution to political parties shall not be considered as CSR activities.

Clarification from Ministry General Circular No. 21/2014 Dated 18th June, 2014:-

1. Company should ensure the following

– CSR policy must relatable to schedule VII,

– Schedule VII must be Interpreted Liberally so as to capture the essence of the subject enumerated in the said schedule

2. It is also clarified that

– Activity must be conducted in project/programme mode,

– One-off event such as marathon, award, charitable contribution, advertisement & sponsorship on TV programme would not qualify for CSR expense.

3. Fulfillment of any act or statute shall not be qualify.

4. Salaries paid to

– CSR staff

– Volunteers (For CSR)

Shall qualify for CSR.

5. Expenditure by foreign holding’s allowed in relation to its subsidiary, if routed through subsidiary.

Disclosure Requirement:-

Section 134(3)(o) requires a company to give the details in its board’s report about the policy developed and implemented by the company on corporate social responsibility and initiatives taken during the year.

Penal Provisions:-

No penal provision is contained in Section 135 but still we can link it with other provisions of the act.

1. Section 134(8) non disclosure in board’s report,

– Fine of 50,000 to 25,00,000,

– Officers in default shall be punishable with fine of Rs. 50,000 to 5,00,000 or Imprisonment of more than 3 years or both

2. Section 450 Punishment where no special penalty or punishment is provided

– Every officer of the company shall be punishable fine of 10,000

– If the default continued for more than 1 year penalty shall be 1,000 Rs. Such day

Auditor’s Responsibility regarding CSR:-

If company is not complying with the provisions of section 135 of companies act, 2013 i.e. CSR, then auditor is required to report the fact in his report under “Emphasis on Matter Paragraph” As per SA-706.

Relationship of CSR with Income Tax:-

A) Following donation are allowed subject to Maximum of 10% of Adjusted Gross total Income;

1. Donation to govt. for promoting family planning etc.- 100% allowed.

2. Donation eligible for 50% deduction

– Donation to govt for other charitable purpose,

– Donation for other housing accommodation/ improvement of cities, towns or village etc.

B) Eligible of 100% deduction w/o maximum limit;

1. Donation to PM national relief fund,

2. Donation to state govt fund for medical relief to the poor,

3. National illness assistant fund,

4. Chief minister’s of Lt.’s relief fund,

5. Approved university or educational institution of national eminence, etc.

Advantages of CSR:-

1. It is treated as expense hence TAX BENEFIT is available.

2. CSR improves environment in which company operates.

3. Benefits the business in indirect manner.

FORMAT FOR THE ANNUAL REPORT ON CSR ACTIVITIES TO BE INCLUDED IN THE BOARD’S REPORT:-

1. A brief outline of the company’s CSR policy, including overview of projects or programs proposed to be undertaken and a reference to the web-link to the CSR policy and projects or programs.

2. The Composition of CSR committee.

3. Average Net Profits of the company from the last three years.

4. Prescribed CSR expenditure (2% of the Average net profits of three preceding financial years).

5. Details of CSR spent during the year.

– Total amount to be spent for the financial year

– Amount unspent; if any;

– Manner in which the amount spent during the financial year is detailed below;

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| S. No. | CSR project or activity identified | Projects or programs(1) Local area or other

(2) Specify the state & district where projects and programs was undertaken |

Amount outlay (budget) projects and programs wise | Amount spent of the projects and programsSub Heads

1.) Direct expenditure on projects and program 2.) Overheads |

Cumulative expenditure upto the reporting period | Amount spent direct or through implementing agency |

| 1 | ||||||

| 2 | ||||||

| 3 | ||||||

| Total |

Details of implementing agency is also required.

6. In case the company has failed to spent the 2% of the average Net Profits of the company from the last three financial years or any part thereof; the company shall provide the reason for not spending the amount in its Board’s Report.

7. A responsibility statement of CSR committee that the implementation and monitoring of CSR policy, in with compliance with the CSR objective and policy.

| Sd/-(Chief Executive

Officer or Managing Director or Director) |

Sd/-(Chairman CSR

Committee) |

Sd/-(Person specified under

clause (d) of sub-section (1) of section 380 of the Act) (wherever applicable) |

Schedule VII

Clause I

1. eradicating hunger,

2. poverty and malnutrition,

3. promoting preventive health care and sanitation

4. making available safe drinking water

Clause II

1. promoting education,

2. including special education and,

3. employment enhancing vocation skills

4. Especially among children, women, elderly, and the differently abled and livelihood enhancement projects;

Clause III

1. promoting gender equality,

2. empowering women,

3. setting up homes and hostels for women and orphan,

4. setting up old age homes, day care centres and such other facilities for senior citizens and

5. Measures for reducing inequalities faced by socially and economically backward groups.

Clause IV

1. ensuring environmental sustainability,

2. ecological balance,

3. protection of flora and fauna, animal welfare, agro forestry,

4. conservation of natural resources and maintaining quality of soil, air and water

Clause V

1. protection of national heritage, alt and culture including restoration of buildings and sites of historical importance and works of art;

2. setting up public libraries

3. promotion and development of traditional arts and handicrafts

Clause VI

1. Measures for the benefit of armed forces veterans, war widows and their dependents.

Clause VII

1. training to promote rural sports, nationally recognised sports, Paralympic sports and Olympic sports

Clause VIII

1. contribution to the Prime Minister’s National Relief Fund or any other fund set up by the Central Government for socio-economic development and relief and welfare of the Scheduled Castes, the Scheduled Tribes, other backward classes, minorities and women

Clause IX

1. Contributions or funds provided to technology incubators located within academic institutions which are approved by the Central Government.

Clause X

1. Rural development projects

Calculation of Profit u/s 198

| Particulars | Amount |

| Profit before Tax as per Statement of Profit and Loss | xxxx |

| Less: | |

| Profits by way of premium on shares or debentures of the company | xxxx |

| Profits on sales by the company of forfeited shares | xxxx |

| Profits of a capital nature including profits from the sale of the undertaking | xxxx |

| Profits from the sale of any immovable property or fixed assets of a capital nature | xxxx |

| Any change in carrying amount of an asset or of a liability recognized in equity reserves | xxxx |

| Add: | |

| Income-tax and super-tax payable by the company under the Income-tax Act, 1961 | xxxx |

| Any compensation, damages or payments made voluntarily | xxxx |

| Loss of a capital nature including loss on sale of the undertaking or any of the undertakings of the company | xxxx |

| Any change in carrying amount of an asset or of a liability | xxxx |

| Profits eligible for CSR calculation | xxxx |

(Author is a CA Final Student and can be reached at piyushkumargoel798@gmail.com)