Similarly most of the financial frauds in the corporate fall under asset misappropriation and the submission of fraudulent statements such as concealment of liabilities, improper asset valuation, fictitious revenues, improper disclosures, etc. are some types of frauds. These practices cause severe damage to the financial system of institutions across countries. Similarly, with the help of leakages in systems of cyber and technology, fraudsters commit financial crimes. These damage the personal finance of individuals and the entire economy.

Types of corporate fraud

⇒ Bribery and corruption

⇒ Misappropriation of assets

⇒ Manipulation of financial statement

⇒ Procedure related frauds

⇒ Corporate espionage

Financial Statement Frauds

The Association of Certified Fraud Examiners (ACFE) defines financial misstatement as deliberate misrepresentation of the financial condition of an enterprise. Some of their ways to identify financial fraud schemes include:

- Increased revenues without a corresponding increase in cash flow, especially over time

- Significant, unusual or highly complex transactions, particularly those that are closed near the end of a financial reporting period

- Unusual growth in the number of days’ sales in receivables

- Strong revenue growth when peer companies are experiencing weak sales

Fraud Triangle

The fraud triangle is a model for explaining the factors that cause someone to commit occupational fraud. It consists of three components which, together, lead to fraudulent behaviour.

1. Pressure:- This arises when an individual have some financial need and he cannot solve it through the legitimate means so he involves in illegal activities such a stealing cash or falsification of financial statements

1. Pressure:- This arises when an individual have some financial need and he cannot solve it through the legitimate means so he involves in illegal activities such a stealing cash or falsification of financial statements

2. Opportunity:- The person must see some way he can abuse his position of trust to solve his financial problem with a low perceived risk of getting caught.

Rationalization:-This is the vast majority of fraudster are first time offender with no criminal past, they do not view them self as a criminal. They see them self as ordinary, honest people who are caught in a bad set of circumstances.

Major reasons of corporate frauds in India

⇒ Weak financial controls leads to poor performance.

⇒ Poor performance companies as due to poor compensation don’t have qualified internal audit department, internal controls and checks.

⇒ Poor performance companies are defaulter of banks, financial institution.

⇒ Profit making company absorbs debts, loans and advances, fixed assets and investments to achieve tax planning.

⇒ Additional disclosure in financial statements reduces or prevent frauds.

⇒ Mergers and acquisition provide an opportunity to commit fraud.

The Top Corruption Scams in India

1. Indian Coal Allocation Scam – 2012 – 1,86,000 Crore

The basic premise of this scam was that wrongful allocation of Coal deposits by Government without resorting to competitive bidding, which would have made huge amounts to the Government (to tune of 1.86 Lakh crore). However, the coal deposits were allocated arbitrarily.

2. 2G Spectrum Scam – 2008 – 1,76,000 Crore

We have had a number of scams in India; but none bigger than the scam involving the process of allocating unified access service licenses. At the heart of this Rs.1.76-lakh crore worth of scam is the former Telecom minister A Raja – who according to the CAG, has evaded norms at every level as he carried out the dubious 2G license awards in 2008 at a throw-away price which were pegged at 2001 prices.

3. Commonwealth Games Scam – 2010 – 70,000 Crore

Another feather in the cap of Indian scandal list is Commonwealth Games loot. It is estimated that out of Rs. 70000 crore spent on the Games, only half the said amount was spent on Indian sportspersons.

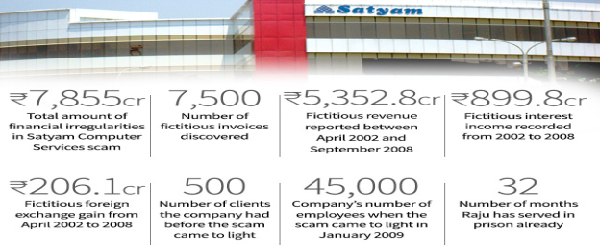

4. Satyam Scam – 2009 – 7,000 Crore

The scam at Satyam Computer Services is something that will shatter the peace and tranquility of Indian investors and shareholder community beyond repair. Satyam is the biggest fraud in the corporate history to the tune of Rs. 7000 crore

5. The Fodder Scam – 1990s – 1,000 Crore

If you haven’t heard of Bihar’s fodder scam of 1996, you might still be able to recognize it by the name of “Chara Ghotala,” as it is popularly known in the vernacular language. In this corruption scandal worth Rs.900 crore, an unholy nexus was traced involved in fabrication of “vast herds of fictitious livestock” for which fodder, medicine and animal husbandry equipment was supposedly procured

6. Harshad Mehta and ketan parekh stock market scam -1992 – 5000 crore

Although not corruption scams, these have affected many people. There is no way that the investor community could forget the unfortunate Rs. 4000 crore Harshad Mehta scam and over Rs. 1000 crore Ketan Parekh scam which eroded the shareholders wealth in form of big market jolt.

Prevention, Detection and Deterrence in Digital Economy

Breaking the fraud triangle is the key to fraud deterrence. Breaking the fraud triangle entails removing one of the elements in the fraud triangle. In order to reduce the likelihood of fraudulent activities of the three elements, removal of opportunity is most directly affected by the system of internal controls and generally provides most actionable route to deterrence of fraud.

SAS 99

Statement on Auditing Standards No. 99 (SAS 99), Consideration of Fraud in a Financial Statement Audit, was “the first major audit standard to be released since the passage of Sarbanes-Oxley”. While the standard was intended to assist auditors in detecting fraud during a financial statement audit, its application was more pervasive. “SAS No. 99 has the potential to significantly improve audit quality, not just in detecting fraud, but in detecting all material misstatements and improving the quality of the financial reporting process”.

The SAS 99 Practice Aid discusses fraud deterrence in addition to its primary focus of fraud detection, “Because fraud prevention, detection, deterrence are management’s responsibility, the new fraud SAS now requires you to determine whether management has designed programs and controls that address identified risks of material misstatement due to fraud and whether those programs and controls have been placed in operation”. In essence, the AICPA has identified that fraud deterrence can be achieved through the implementation of controls and procedures that mitigate (Mitigating Controls) against areas already identified as risk areas.

COSO Model

In 1992, the Committee of Sponsoring Organizations of the Treadway Commission (COSO) developed a model for evaluating internal controls. This model has been adopted as the generally accepted framework for internal control and is widely recognized as the definitive standard against which organizations measure the effectiveness of their systems of internal control.

The COSO model defines internal control as “a process, effected by an entity’s board of directors, management and other personnel, designed to provide reasonable assurance of the achievement of objectives in the following categories:

- Effectiveness and efficiency of operations

- Reliability of financial reporting

- Compliance with applicable laws and regulations”

In an “effective” internal control system, the following five components work to support the achievement of an entity’s mission, strategies and related business objectives.

1. Control Environment

⇒ Integrity and Ethical Values

⇒ Commitment to Competence

⇒ Board of Directors and Audit Committee

⇒ Management’s Philosophy and Operating Style

⇒ Organizational Structure

⇒ Assignment of Authority and Responsibility

⇒ Human Resource Policies and Procedures

2. Risk Assessment

⇒ Company-wide Objectives

⇒ Process-level Objectives

⇒ Risk Identification and Analysis

⇒ Managing Change

3. Control Activities

⇒ Policies and Procedures

⇒ Security (Application and Network)

⇒ Application Change Management

⇒ Business Continuity/Backups

⇒ Outsourcing

4. Information and Communication

⇒ Quality of Information

⇒ Effectiveness of Communication

5. Monitoring

⇒ Ongoing Monitoring

⇒ Separate Evaluations

⇒ Reporting Deficiencies

These components work to establish the foundation for sound internal control within the company through directed leadership, shared values and a culture that emphasizes accountability for control. The various risks facing the company are identified and assessed routinely at all levels and within all functions in the organization. Control activities and other mechanisms are proactively designed to address and mitigate the significant risks. Information critical to identifying risks and meeting business objectives is communicated through established channels up, down and across the company. The entire system of internal control is monitored continuously and problems are addressed timely.

Conclusion

From above discussion we can conclude that Digital economy will be able to prevent and detect the fraud at the early stage but its ultimate prevention is in the hands of the key managerial personnel because the implementation of all the Systems for prevention of frauds is in their hands. Along with the effective information system there must be strong ethical environment in the organization and all the ethical measures should be put in place for discouragement of the frauds.

Suggestions and policy implications

- Strengthen of internal audit department and audit committees

- Regulation for scrutiny of auditor’s role and provision for rotation

- Implementation of corporate governance in small and medium enterprises

- Adoption of international financial reporting standards

- Conducting of due diligence by banks and financial institutions

- Setting up of corporate offence wing with criminal powers

- Provisions of approval of related party transactions by specific committee

- Publication of fraud prevention policy

- Recognition to companies for improved corporate governance

- Co ordination among various regulatory authorities

- Vesting with SEBI with powers to punish

Does lmt company can charge 6% interest for 15days as business interests if his customers has to pay due amount