CA Anshika Patni

Overview of various sections for Auditor’s responsibility under Companies Act, 2013 and detailed analysis of Section 139.

Certain Sections of Companies Act, 1956 which are now not in existence as per Companies Act, 2013 are as follows:

Section 224A: Auditor not to be appointed except with the approval of the Company by Special resolution in certain cases.

Section 233A: Power of Central Govt. to direct Special Audit in certain cases

New Sections relating to Auditors:

| Section Name | Section No. as per New Companies Act,2013

|

Section No. as per Old Companies Act, 1956 |

| Appointment of Auditor

|

139 | 224 |

|

Removal, resignation of Auditor and giving of special notice |

140 |

225 |

| Eligibility, Qualifications & Disqualifications of Auditors

|

141 | 226 |

| Remuneration of Auditor

|

142 | 224 |

| Powers and Duties of Auditor and AS

|

143 | 227, 228 |

| Auditors not to render certain services. | 144 | New insertion |

| Auditor to sign Audit report

|

145 | 229,230 |

| Auditor to attend General Meeting | 146 | 231 |

| Punishment for contravention

|

147 | 232, 233 |

| Central Govt. to specify audit of items of cost in respect of certain Companies.

|

148 | 233B |

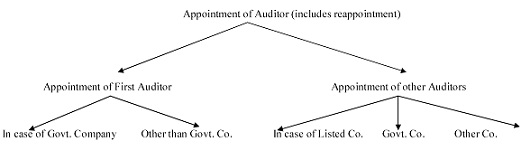

Section 139 :

Overview of Section:

| Rules regarding Appointment of First Auditor: | |

| In case of Govt. Company | Incase of other than Govt. Company |

|

Appointment of Auditor by BOD within 30 days of Registration of Company. In case of failure by BOD, members of The company will appoint within 90 days at an EGM who shall hold office till the conclusion of first AGM. |

Rules regarding Appointment of Other Auditor:

It includes rules regarding rotation, reappointment and filing of casual vacancy.

1. Appointment of Auditor:

a. In case of Govt. Company:

Auditor will be appointed by the C&AG within 180 days from the commencement of the Financial Year, who shall hold office till the conclusion of the AGM.

b. In case of other than Govt. Company:

- Every other company shall at the first AGM appoint an individual or a firm as an Auditor who shall hold office from the conclusion of that AGM till the conclusion of its sixth AGM and thereafter till the conclusion of every sixth meeting.

- Even if the auditor is appointed for 5 years, then also members of the Company should ratify such appointment at every AGM.

- The manner and procedure of the appointment of the Auditor is prescribed by CG.

- Before the appointment of the auditor the written consent of the auditor to such appointment and certificate showing compliance of Section 141 and other conditions as prescribed, should be obtained.

- Notice of Appointment of Auditor should be filled with the Registrar within 15 days of the meeting in which the auditor is appointed.

2. Some other Provisions regarding re appointment of Auditor:

a. A retiring auditor may be re- appointed at an AGM, if:

i. He is not disqualified for re-appointment

ii. He has not given the company a notice in writing of his unwillingness to be re appointed

iii. A special resolution has not been passed at that meeting appointing some other auditor or providing expressly that he shall not be appointed.

3. Where at an AGM, no auditor is appointed or re-appointed, the existing auditor shall continue to be the auditor of the Company.

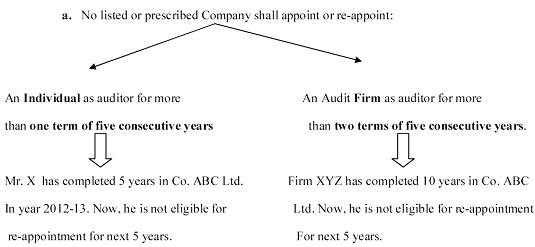

4. Provisions for Listed and other prescribed Company:

If Mr. X is a common partner in firm XYZ and Firm VWX , then Firm VWX is also not eligible for appointment as auditor in Co. ABC Ltd. For that 5 years (i.e. from 2013-14 ).

Already existing Company shall comply with these provisions of listed company within three years from the date of commencement of this Act.

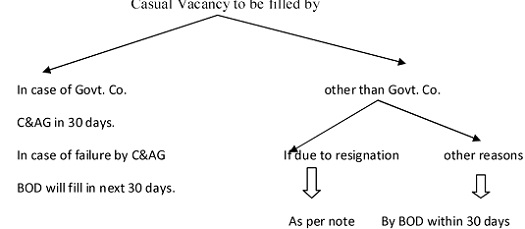

5. In case of Casual Vacancy:

Note: In case of resignation by auditor:

Note: In case of resignation by auditor:

Casual Vacancy to be filled by BOD within 30 days but the same should be approved by the members in a general meeting (EGM) to be convened within 3 months of the recommendation of the Board. He shall hold office till the conclusion of next AGM.

Excellent job. It helps professionals as well as others to get information on new Companies Act & Rules. Keep the good work going.

good job….i appreciate it

Good information ,keep it up.

CA. Subhash Chandra Podder

Kolkata

23/04/2014