A. As per Companies Act 2013

RULE 9 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014

The Ministry of Corporate Affairs(MCA) vide its Notification dated January3, 2020, mandated every Company(including Private Company):-

- having outstanding loans or borrowings from banks or public financial institutions of

one hundred crore rupees or more. (Rs. 100 Cr or more) *

shall annex with its Board’s report a Secretarial Audit Report, given by a Company Secretary inPractice with effect from financial year 2020-21 onwards.

The materiality of this section lies in its applicability to Private Companies as well and the same shall be effective from 1st April 2020, which implies the “first audit period” of Private Companies with Debt outstanding as mentioned above, will be from 1st April 2020 to 31st March 2021, also the “First Secretarial Audit Report” will be required to be annexed with the Board’s Report of financial year 2020-21.

Further, it is to be noted significantly, that, the First Secretarial Audit Report will be issued by the Company Secretaries in Practice to the above Private Companies “DURINGTHE FINANCIAL YEAR 2021-22”.

Previously, as per Section 204 of Companies Act 2013 read with Rule 9 of Companies (Appointment and Remuneration of Managerial Personnel) Rules 2014, Secretarial Audit was applicable to only following class of Public Companies (Listed /Unlisted):-

- Every Listed Company; or

- Every public company having a Paid-up share capital of fifty crore rupees or more (Rs. 50 Cr or more); or

- Every public company having a Turnover of two hundred fifty crore rupees or more (Rs. 250Cr or more);

Additionally, it is hereby clarified in the amendment that, above mentioned limits of the Paid-up Share Capital/Turnover/Outstanding Loans or Borrowings as existing on the “last date” of latest audited financial statement will be taken into consideration.

In the Current/First Audit Period of Private Companies, date of latest audited financial statement will be 31st March 2020 to check the applicability of the secretarial audit “for the financial year 2020-21” which falls in the financial year 2021-22”.

B. SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015

Securities and Exchange Board of India, mandated Secretarial Audit to “Material unlisted Subsidiary” of listed entity by inserting Reg 24A in the SEBI (Listing Obligations and Disclosure Requirements), Regulations, 2015, w.e.f. 31st March 2019.

Regulation 24A of LODR readsas under:-

- Every listed entity and its material unlisted subsidiaries incorporated in India shall undertake secretarial audit and shall annex with its annual report, a secretarial audit report, given by a company secretary in practice, in such form as may be specified with effect from the year ended March 31, 2019.

It is hereby clarified that in “Material Subsidiary Companies”,Private Companies are also included.

Material Subsidiary: –It means a subsidiary, whose income or net worth exceeds ten percent of the consolidated income or net worth respectively, of the listed entity and its subsidiaries in the immediately preceding accounting year.

CONCLUSION: – In a nutshell, we can conclude that, Secretarial Audit is now applicable to below mentioned Private Companies: –

1. A Company having outstanding loans or borrowings from banks or public financial institutions of one hundred crore rupees or more. (Rs. 100 Cr or more);

2. A Company which is a Material Subsidiary of any listed entity.

–

SCOPE OF SECRETARIAL AUDIT

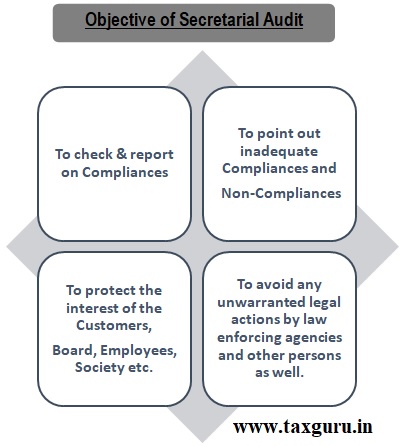

Secretarial Audit is a mechanism which gives necessary comfort to the management, regulators and the stakeholders, as to the compliance by the company of applicable laws and the existence of proper and adequate systems and processes in the company. It postulates verification on a test basis of records, books, papers and documents to check compliance with the provisions of various statutes, laws and rules & regulations by a Company Secretary in Practice to ensure compliance of legal and procedural requirements and processes.

Companies who are mandated to file a secretarial audit report under the Companies Act, 2013. For the secretarial audit report, compliance should meet requirements under the following regulations: –

1. Companies Act, 2013 and the rules made thereunder;

2. Securities Contracts (Regulation) Act, 1956 and the rules made thereunder;

3. Depositories Act, 1996 and the rules made thereunder;

4. Foreign Exchange Management Act, 1999 and rules and regulations made thereunder to the extent of foreign direct investment, overseas direct investment, and external commercial borrowings;

5. Secretarial Standards Issued by ICSI (“Institute of Company Secretaries of India”); and

6. Business Specific Laws Applicable, if any.

Disclaimer:- The information of this article are for information purposes only and do not constitute advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. All information is provided in good faith, to create awareness of legal provisions, compliance and procedures and are solely for knowledge sharing purpose.Readers are requested to check and refer to relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up.

Author Bio

Quite informative!

Very insightful. Thank you, Deepak Patel.