SHORT SUMMARY:

According to Section 137(1) (Copy of financial statement to be filed with Registrar) of the Company Act, 2013, A copy of the financial statements, including consolidated financial statement duly adopted at the annual general meeting of the company, shall be filed with the Registrar within thirty days of the date of annual general meeting.

And if where the financial statements under are not adopted at annual general meeting or adjourned annual general meeting, such unadopted financial statements shall be filed with the Registrar within thirty days of the date of annual general meeting.

According to Section 92(4) (Filing of Annual Return) of the Company Act 2013 company shall file with the Registrar a copy of the annual return, within sixty days from the date on which the annual general meeting is held or where no annual general meeting is held in any year within sixty days from the date on which the annual general meeting should have been held together with the statement specifying the reasons for not holding the annual general meeting.

Every corporation must comply with the above provision in order to preserve good governance. Many Companies registered with the MCA (Ministry of Corporate Affairs) do not follow this clause of the Company Act 2013.

MCA should take action against companies who fail to file their financial statements on time. Even Practicing Company Secretaries who certify the MGT-7 or MGT-8 must note this non-compliance in forms.

Ministry of Corporate Affairs appointed undersigned as Adjudicating Officer in exercise of the powers conferred by Section 454 of the Act, 2013

The Company Sankardev Coke Products Limited launched a Suo moto submission of an application respecting the terms of Section 92(4) And 137(1) Companies Act 2013. In this editorial we will discuss one of those order. The complete matter shall be covered here.

“Adjudication Order in the Matter of SANKARDEV COKE PRODUCTS LIMITED”

1. FACTS OF THE CASE:

1. The Company Filed the Financial Statements for FY 2016-17 on 30.06.2018 with the Delay of 244 Days and Filed Annual Return for FY 2016-17 on 30.06.2018 with the Delay of 214 Days.

2. The ROC Guwahati Filed a Complaint against the Company and its Directors before Court of Chief Judicial Magistrate, Shillong in 2018.

3. In August 2022, Company and its Directors have Suo motto filed an Application in Form GNL-1 U/s 454 of Companies act 2013 for Adjudication of Penalty and for Dropping of any further proceeding for Violation of provisions of Section 92 & 137 of Companies act 2013.

4. On behalf of the Company, Company Secretary appeared and attended the hearing on 28.06.2023 & Submitted that Company has Filed Financial Statements with the delay of 244 Days & Annual Returns with the Delay of 214 Days & Prayed for Adjudication of the penalty for such violation and for Dropping of any further proceeding for violation of above mentioned Provisions.

2. ORDER:

Under Section 137(3) If a company fails to file the copy of the financial statements before the expiry of the specified period, the company shall be liable to a penalty of Ten thousand rupees and in case of continuing failure, with a further penalty of one hundred rupees for each day during which such failure continues, subject to a maximum of two lakh rupees, and the managing director and the Chief Financial Officer of the company, if any, and, in the absence of the managing director and the Chief Financial Officer, any other director who is charged by the Board with the responsibility of complying with the provisions of this section, and, in the absence of any such director, all the directors of the company, shall be liable to a penalty of ten thousand rupees and in case of continuing failure, with further penalty of one hundred rupees for each day after the first during which such failure continues, subject to a maximum of fifty thousand rupees.

Under Section 92(5) If any company fails to file its annual return before the expiry of the period specified, such company and its every officer who is in default shall be liable to a penalty of ten thousand rupees and in case of continuing failure, with a further penalty of one hundred rupees for each day during which such failure continues, subject to a maximum of two lakh rupees in case of a company and fifty thousand rupees in case of an officer who is in default.

> Upon Receipt of the application U/s 454, The Presenting Officer submitted that keeping in mind the ease of doing business in India and the instruction of ministry regarding decriminalization the matter deserves in house adjudication.

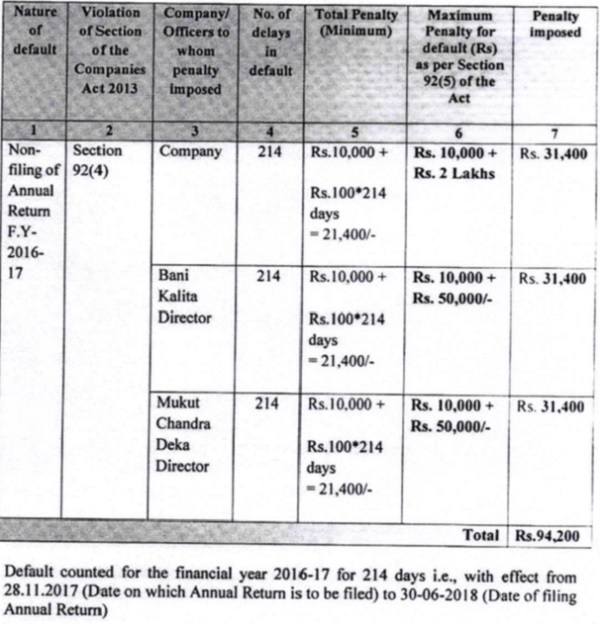

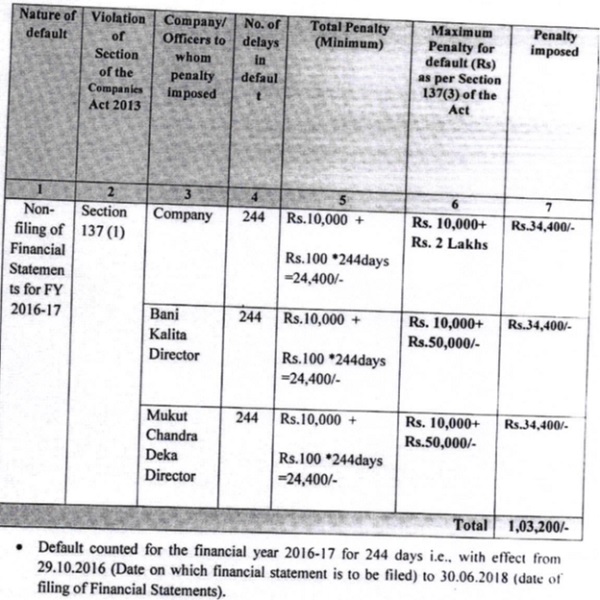

> The Adjudicating Officer Carefully Perused the Reply Made by the Company and imposed penalty under Section 137(3) on Company and its Directors as per Table below for violation of Section 92(5) of the Companies Act, 2013.

–

|

Company/ Officers to whom Penalty imposed |

Total Period of Default | Penalty for defaults (Rs.) as per section 92(5) of the company act 2013 | Total Penalty (Rs.) | Penalty Imposed (Rs. |

| On Company For Non-Filing of Annual Return | 214 Days | Rs. 10,000+

Max. 2,00,000

|

Rs. 10,000+

Rs. 100*214=21,400 |

31,400 |

| On Bani Kalita, Director, For Non-Filing of Annual | 214 Days | Rs. 10,000+

Max. 50,000 |

Rs. 10,000+

Rs. 100*214=21,400 |

31,400 |

| On Mukut Chandra, Director, For Non-Filing of Annual Return | 214 Days | Rs. 10,000+

Max. 50,000 |

Rs. 10,000+

Rs. 100*214=21,400 |

31,400 |

| Total | 94,200 |

–

|

Company/ Officers to whom Penalty imposed |

Total Period of Default | Penalty for defaults (Rs.) as per section 137(3) of the company act 2013 | Total Penalty (Rs.) | Penalty Imposed (Rs. |

| On Company For Non-Filing of Financial Statements | 244 Days | Rs. 10,000+

Max. 2,00,000 |

Rs. 10,000+

Rs. 100*244=24,400 |

34,400 |

| On Bani Kalita, Director, For Non-Filing of Financial Statements | 244 Days | Rs. 10,000+

Max. 50,000 |

Rs. 10,000+

Rs. 100*244=24,400 |

34,400 |

| On Mukut Chandra, Director, For Non-Filing of Financial Statements | 244 Days | Rs. 10,000+

Max. 50,000 |

Rs. 10,000+

Rs. 100*244=24,400 |

34,400 |

| Total | 1,03,200 |

3. CONCLUSION:

Financial Statement and Annual Returns are statements that provides an outlook of a company’s performance for a given year and its financial position. It contains detailed information about a company, its nature of business, its current financial status, its executive officers etc.

Therefore, for good corporate governance, Companies should timely file their Financial Statements and Annual Returns with the ROC to avoid adjudication and penalties.

Further, Every Company Secretary and auditor of the Company should report this non-compliance in MGT-7, MGT-8, and their Statutory Audit report to avoid future penalties.

*****

Author – CS Divesh Goyal, GOYAL DIVESH & ASSOCIATES Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com).

Disclaimer: The whole content of this document was created using pertinent laws and the information available at the time of creation. I take no responsibility despite the fact that every effort has been made to assure the accuracy, reliability, and completeness of the material supplied. Users of this information are expected to consult the pertinent, currently in effect laws. The information’s user acknowledges that it is not expert advise and that it is subject to change at any time. I disclaim all liability for the results of using such information.

I will never be responsible for any direct, indirect, incidental, special, or consequential damages that result from, arise from, or are related to the use of the information.

Author Bio