Introduction: On June 23rd, 2023, the Institute of Chartered Accountants of India (ICAI) made a significant announcement regarding the formulation of a New Scheme of Education and Training. This scheme aligns with International Education Standards and the National Education Policy, 2020 (NEP). The ICAI has taken into account inputs from various stakeholders and has notified the scheme in the Gazette of India, set to be implemented from July 1st, 2023.

Overview of the New Scheme of Education and Training: The New Scheme of Education and Training aims to bring the curriculum in line with international standards and the evolving needs of the accounting profession. It encompasses changes and updates that reflect the requirements of the NEP. The scheme will have a profound impact on aspiring chartered accountants, and it is important to understand its key elements and timelines.

Implementation Dates and Important Points: The ICAI has provided a comprehensive list of dates and particulars regarding the implementation of the New Scheme of Education and Training. These include registration deadlines, commencement dates for different courses, the last examinations under the existing scheme, and the commencement of practical training. It is essential for aspiring students and current candidates to take note of these dates to ensure a smooth transition into the new system.

Syllabus, Transition Scheme, and FAQs: To assist candidates in understanding and adapting to the New Scheme of Education and Training, the ICAI will host the syllabus, transition scheme, and frequently asked questions (FAQs) on July 1st, 2023. These resources will provide detailed information about the changes in the curriculum, guidelines for transitioning from the existing scheme, and answers to common queries. Additionally, the ICAI will announce the paper-wise exemption plan in due course, offering further clarity on the transition process.

Conclusion: The introduction of the New Scheme of Education and Training by the ICAI marks a significant step toward aligning with international standards and the NEP. It is crucial for students, aspiring chartered accountants, and current candidates to familiarize themselves with the scheme’s key elements, implementation dates, and resources provided by the ICAI. By embracing these changes, individuals can ensure a seamless transition and enhance their professional development in the field of chartered accountancy.

Relevant ICAI Press Release and Gazette Notification is as given below

Board of Studies (Academic)

The Institute of Chartered Accountants of India

23rd June, 2023

Announcement for New Scheme of Education and Training

The Institute of Chartered Accountants of India (ICAI) has formulated the New Scheme of Education and Training in lines with International Education Standards and National Education Policy, 2020 (NEP) after considering the inputs from various stakeholders. The New Scheme of Education and Training has been notified in the Gazette of India on 22nd June, 2023 and will come into effect from 1st July, 2023.

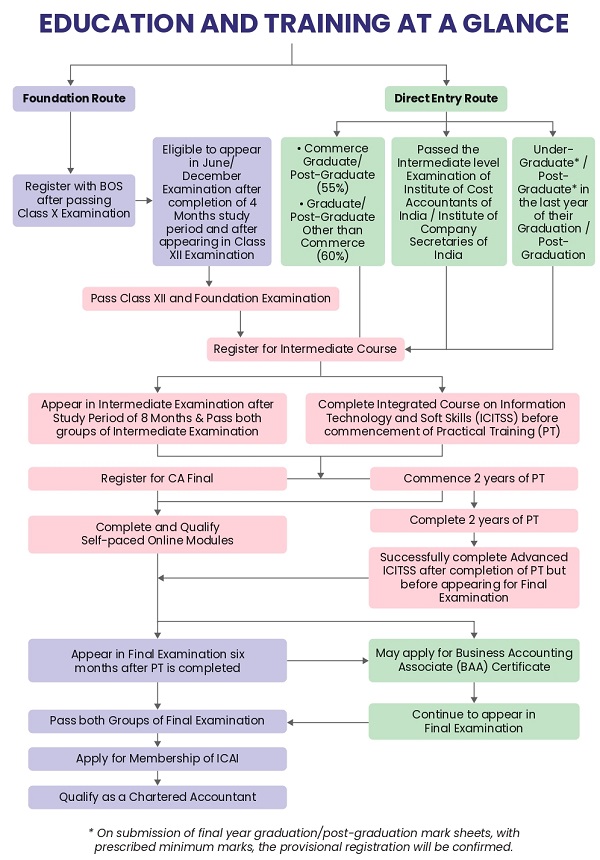

The New Scheme of Education and Training at a glance –

Important dates for the implementation of New Scheme of Education and Training are given as under:

| S. No. | Particulars | Date/ Attempt |

| 1. | Last date for Registration in Foundation under Existing Scheme | 1st July, 2023 |

| 2. | Last date for Registration in Intermediate and Final Courses under Existing Scheme | 30th June, 2023 |

| 3. | Date of commencement of Registration and Conversion in Foundation Course under New Scheme | 2nd August, 2023 |

| 4. | Date of commencement of Registration and Conversion in Intermediate and Final Courses under New Scheme | 1st July, 2023 |

| 5. | First Foundation Examination under New Scheme | June, 2024 |

| 6. | First Intermediate and Final Examination under New Scheme | May, 2024 |

| 7. | Last Foundation Examination under Existing Scheme | December, 2023 |

| 8. | Last Intermediate and Final Examination under Existing Scheme | November, 2023 |

| 9. | Last date of commencement of three years Practical Training | 30th June, 2023 |

| 10. | Date of commencement of two years uninterrupted Practical Training | 1st July, 2023 |

Syllabus, Transition Scheme and Frequently Asked Questions (FAQs) will be hosted on 1st July, 2023. Paper wise exemption plan will be announced in due course.

****

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

NOTIFICATION

New Delhi, the 21st June, 2023

No.1-CA(7)/201/2023.—WHEREAS certain draft regulations further to amend the Chartered Accountants Regulations, 1988 were published, as required by sub-section (3) of section 30 of the Chartered Accountants Act, 1949 (38 of 1949), in the Gazette of India, Extraordinary, Part III, Section 4, dated the 2nd June, 2022, inviting objections and suggestions from persons likely to be affected thereby, before the expiry of thirty days from the date on which the copies of the Gazette containing the said notification were made available to the public;

AND WHEREAS the said Gazette was made available to the public on the 2nd June, 2022;

AND WHEREAS the objections and suggestions received from the public on the said draft regulations have been considered by the Council of the Institute of Chartered Accountants of India;

NOW, THEREFORE, in exercise of the powers conferred by section 30 of the Chartered Accountants Act, 1949 (38 of 1949), the Council of the Institute of Chartered Accountants of India, with the approval of the Central Government, hereby makes the following regulations further to amend the Chartered Accountants Regulations, 1988, namely:—

1. (1) These regulations may be called the Chartered Accountants (Amendment) Regulations, 2023.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Chartered Accountants Regulations, 1988 (hereinafter referred to as the said regulations), regulations 25C and 25D shall be omitted.

3. In regulation 25E of the said regulations, —

(a) in sub-regulation (1), after the words “by law in India”, the words “or outside India” shall be inserted;

(b) in sub-regulation (2), the following proviso shall be inserted, namely: —

“Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.”;

(c) after sub-regulation (2), the following sub-regulations shall be inserted, namely: —

“(3) A candidate who was already registered for the Common Proficiency Course under regulation 25C or Foundation Course, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall be eligible for conversion to the Foundation Course subject to such conditions as may be specified by the Council.

(4) The registration for the Foundation Course shall be valid only for a period of four years from the date of first eligible attempt in the Foundation Examination under regulation 25F after the commencement of the Chartered Accountants (Amendment) Regulations, 2023”.

4. In regulation 25F of the said regulations, —

(a) in sub-regulation (1), —

(i) for clause (a), the following clause shall be substituted, namely: —

“(a) is registered with the Board of Studies of the Institute for a minimum period of four months on or before the 1st day of the month in which the examination is held and has complied with such other requirements as may be specified by the Council from time to time; and”;

(ii) in clause (b), after the words “by law in India”, the words “or outside India” shall be inserted;

(b) in sub-regulation (2), the following proviso shall be inserted, namely: —

“Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.”.

5. Regulations 28D and 28E of the said regulations shall be omitted.

6. For regulations 28F and 28G of the said regulations, the following regulations shall be substituted, namely: —

“28F. Registration for Intermediate Course and Fees. — (1) The study course for the chartered accountancy candidates shall be named as Intermediate Course, which shall be composed of two Groups viz. Group I and Group II.

(2) No candidate shall be registered for the Intermediate Course unless he has passed the Foundation Examination under these regulations and Senior Secondary (10+2) examination conducted by an examining body constituted by law in India or outside India or an examination recognised by the Central Government or the State Government as equivalent thereto for the purpose of admission to graduation course and has complied with such other requirements as may be specified by the Council from time to time:

Provided that a candidate who has passed the Entrance Examination or the Foundation Examination or the Professional Education (Examination – I) or the Common Proficiency Test, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall be eligible for registration to the Intermediate Course under this regulation subject to such conditions as may be specified by the Council:

Provided further that a candidate who was already registered for the Intermediate Course or Professional Education (Course-II) or the Intermediate (Professional Competence) Course or the Intermediate (Integrated Professional Competence) Course, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall be eligible for conversion to Intermediate Course under this regulation subject to such conditions as may be specified by the Council.

(3) A candidate who has passed the Intermediate Examination conducted by the Institute of Cost Accountants of India set up under the Cost and Works Accountants Act, 1959 (23 of 1959) or by the Institute of Company Secretaries of India set up under the Company Secretaries Act, 1980 (56 of 1980) shall also be eligible for registration to the Intermediate

(4) Notwithstanding anything contained in sub-regulation (2), a graduate or post graduate shall be eligible for registration to the Intermediate Course, if such person is—

(a) a graduate or post-graduate in commerce having secured in aggregate a minimum of fifty-five per cent. of the total marks or its equivalent grade in the examination conducted by any recognised university (including Open University) by studying any three papers each carrying a minimum of fifty marks in a semester or year and cumulatively hundred or more marks over the entire duration of the concerned course, out of the subjects i.e., Accounting, Auditing, Mercantile laws, Corporate laws, Economics, Management (including Financial Management), Taxation (including Direct Tax Laws and Indirect Tax Laws), Costing, Business Administration or Management Accounting or similar to the title of these papers with different nomenclatures, as approved by the Board of Studies of the Institute; or

(b) a graduate or post graduate other than those referred to in clause (a), having secured in aggregate a minimum of sixty per cent. of the total marks or its equivalent grade in the examination conducted by any recognised university (including Open University).

Explanation. —For the purpose of this sub-regulation,—

(i) for calculating the percentage of marks, the marks secured in subjects in which a person is required by the University (including Open University) to obtain only pass marks and for which no special credit is given for higher marks, shall be ignored; and

(ii) any fraction of half or more shall be rounded up to the next whole number and any fraction of less than half number shall be ignored.

(5) Notwithstanding anything contained in sub-regulation (2), a candidate who is pursuing the final year of graduation or post-graduation course shall be eligible for provisional registration to the Intermediate Course which shall be confirmed only on submission of satisfactory proof of having passed the graduation or post-graduation examination with the minimum marks as provided in sub-regulation (4) before making the application for admission to the Intermediate Examination:

Provided that if a candidate fails to secure minimum marks as provided in sub-regulation (4) before making the application for admission to the Intermediate Examination, his provisional registration shall be cancelled and for the purpose of these regulations—

(i) no credit shall be given for the theoretical education undergone; and

(ii) the Council may on receipt of an application from a candidate who is unable to produce the satisfactory proof referred to in this regulation, permit refund of such amount of registration and tuition fee, as may be decided by it from time to time:

Provided further that a candidate who has already been granted the provisional registration on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023 shall be required to submit the satisfactory proof of having passed the graduation examination within such period not exceeding six months as may be decided by the Council, from the date of appearance in the final year graduation examination:

Provided also that if a candidate fails to produce the proof within the aforesaid period, his provisional registration shall be cancelled and for the purpose of these regulations—

(i) no credit shall be given for the theoretical education undergone; and

(ii) the Council may on receipt of an application from a candidate who is unable to produce the satisfactory proof referred to in this regulation, permit refund of such amount of registration and tuition fee, as may be decided by it from time to time.

(6) A candidate for registration for the Intermediate Course shall pay such fees as may be fixed by the Council which shall not exceed twenty-five thousand rupees along with his application in the form as may be approved by the Council:

Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.

(7) The registration of a candidate under this regulation shall be valid for a period of five years from the date of registration or conversion on or after the commencement of the Chartered Accountants (Amendment) Regulations, 2023.

Provided that a candidate shall be eligible for a one time re-validation for a further period of five years on his making an application in the form approved by the Council and on payment of such fee as may be fixed by the Council from time to time.

28G. Admission to Intermediate Examination, Fees and Syllabus.— (1) No candidate shall be admitted to the Intermediate Examination unless he is registered with the Board of Studies of the Institute and produces a certificate to the effect that he has undergone a study course for such period and in such manner as may be specified by the Council from time to time as on the first day of the month in which the examination is held:

Provided that a candidate who is registered for the Intermediate Course under sub-regulation (4) of regulation 28F shall be eligible for admission to the Intermediate Examination on fulfilling of the following criteria: —

(a) production of a certificate to the effect that he has undergone a study course for a period of not less than eight months; and

(b) submission of satisfactory proof of having passed the graduation or post-graduation examination with the minimum marks as provided in the said regulation before making the application for admission to the Intermediate Examination.

(2) Notwithstanding anything contained in sub-regulation (1), a candidate who was registered for the Intermediate Course or Professional Education (Course–II) or Intermediate (Professional Competence) Course or the Intermediate (Integrated Professional Competence) Course, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall be eligible for admission to the Intermediate Examination subject to such conditions as specified by the Council.

(3) A candidate for the Intermediate examination shall pay such fees, as may be fixed by the Council from time to time, which shall not exceed ten thousand rupees:

Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.

(4) A candidate for the Intermediate Examination, shall be examined as per the syllabus approved by the Council from time to time.”.

7. In regulation 29 of the said regulations, —

(a) in sub-regulation (2), the following proviso shall be inserted, namely: —

“Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.”;

(b) after sub-regulation (2), the following sub-regulation shall be inserted, namely: —-

“(3) The registration of a candidate under this regulation shall be valid for a period of ten years from the date of registration or conversion on or after the commencement of the Chartered Accountants (Amendment) Regulations, 2023.

Provided that a candidate shall be eligible for re-validation for a further period of ten years on his making an application in the form approved by the Council and on payment of such fee as may be fixed by the Council from time to time.”.

8. Regulations 29B and 29C shall be omitted.

9. In regulation 29D of the said regulations, —

(a) for sub-regulation (1), the following sub-regulation shall be substituted, namely: — “(1) No candidate shall be admitted to the Final Examination, unless he—

(i) is registered for the Final Course and has passed both the Groups of the Intermediate Examination held under regulation 28G;

(ii) has completed the practical training as required for admission as a member at least six months before the 1st day of the month in which the examination is held;

(iii) has successfully completed advanced Integrated Course on Information Technology and Soft Skills under regulation 51E;

(iv) has passed the self-paced online modules as per regulation 51 F; and

(v) has complied with such other requirements in such manner as may be specified by the Council from time to time.”;

(b) in the Explanation, for the word “before applying for membership of the Institute”, the words, figure and letter “and to pass the self-paced online modules under regulation 51F, and to comply with such other requirements in such manner as may be specified by the Council from time to time before applying for membership of the Institute.” shall be substituted.

10. In regulation 30, the following proviso shall be inserted, namely: —

“Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.”.

11. In regulation 31, after clause (iv), the following clause shall be inserted, namely: —

“(v) as per the syllabus approved by the Council from time to time after commencement of enrolment to Intermediate Course under regulation 28F on or after the commencement of the Chartered Accountants (Amendment) Regulations, 2023”.

12. In regulation 32 of the said regulations, the words “electronically or” shall be omitted.

13. Regulation 36A of the said regulations shall be omitted.

14. Regulation 37C of the said regulations shall be omitted.

15. In regulation 37D of the said regulations, —

(a) for sub-regulation (2), the following sub-regulation shall be substituted, namely: —

“(2) A candidate shall ordinarily be declared to have passed the Intermediate Examination, if he passes in both Group I and Group II.”;

(b) sub-regulation (3) shall be omitted.

(c) after sub-regulation (8), the following sub-regulations shall be inserted, namely:—

“(9) If a candidate has exhausted the exemption granted to him under sub-regulation (8) and he was not able to pass the said Group or Unit, he may opt for the continuing of said exemption to the subsequent examinations:

Provided that such candidate shall be required to obtain a minimum of fifty per cent. marks in each of the remaining paper or papers of that Group or Unit in order to declare him to have passed in that Group or Unit.

(10) The Council may adopt the criteria of negative marking in a paper or papers having objective type questions in such manner as may be specified by it from time to time.”.

16. Regulations 38B and 38C of the said regulations shall be omitted.

17. For regulation 38D of the said regulations, the following regulation shall be substituted, namely: —

“38D. Requirements for passing Final Examination.— (1) A candidate may appear in Group I or Group II or in a

Unit comprising of a set of papers of Group I or Group II simultaneously or one Group or Unit in one examination and the remaining Group or Unit at any subsequent examination and shall ordinarily be declared to have passed the Final Examination if he passes in both the Groups.

(2) A candidate shall ordinarily be declared to have passed in both the Groups or Units, as the case may be, simultaneously, if he—

(a) secures at one sitting a minimum of forty per cent. marks in each paper of each of the Groups or Units and minimum of fifty per cent. marks in the aggregate of all the papers of each of the Groups or Units; or

(b) secures at one sitting a minimum of forty per cent. marks in each paper of both the Groups or Units and a minimum of fifty per cent. marks in the aggregate of all the papers of both the Groups or Units taken together.

(3) A candidate shall be declared to have passed in a Group or Unit if he secures at one sitting a minimum of forty per cent. marks in each paper of the Group or Unit and a minimum of fifty per cent. marks in the aggregate of all the papers of that Group or Unit.

(4) A candidate who has passed in any one but not in both the Groups or Units of the Final Examination under the syllabus approved by the Council under regulation 31 or of the Final Examination as per the syllabus under paragraph 3 or 3A of Schedule B to these regulations or paragraph 3 of Schedule BB to the Chartered Accountants Regulations, 1964 (two Groups or Units scheme after January 1, 1985) enforced at the relevant time shall be eligible for exemption in that particular Group or Unit and shall be required to appear and pass in the remaining Group or Unit in order to pass the Final Examination.

(5) The Council may frame guidelines to continue to award exemption in a paper or papers to a candidate, granted earlier under the syllabus approved under clause (iv) of regulation 31 for the unexpired chance or chances of the exemption in the corresponding paper or papers in which he had secured exemption, if the corresponding paper or papers exist in the new syllabus of the Final Examination approved by the Council under clause (v) of regulation 31.

(6) On appearing in the examination of the corresponding paper or papers in which he had failed, he shall be declared to have passed the examination, if he secures at one sitting a minimum of forty per cent. marks in the corresponding paper or papers in which he had failed earlier and a minimum of fifty per cent. marks in the aggregate of all the papers of the Group or Unit including the marks of the paper or papers in which he had earlier been granted exemption by the Council.

(7) Notwithstanding anything contained in sub-regulations (1) to (6), a candidate who has appeared in all the papers comprised in a Group or Unit and fails in one or more papers comprised in a Group or Unit but secures a minimum of sixty per cent. marks in any paper or papers of that Group or Unit shall be eligible to appear at any one or more of the immediately next three following examinations in the paper or papers in which he secured less than sixty per cent. Marks:

Provided that he shall be declared to have passed in that Group or Unit, if he secures at one sitting a minimum of forty per cent. marks in each of such papers and a minimum of fifty per cent. of the total marks of all papers of that Group or Unit including the paper or papers in which he had secured a minimum of sixty per cent. marks in the earlier examination referred to above:

Provided further that he shall not be eligible for any further exemption in the remaining paper or papers of that Group or Unit until he has exhausted the exemption already granted to him in that Group or Unit.

(8) If a candidate has exhausted the exemption granted to him under sub-regulation (7) and he was not able to pass the said Group or Unit, he may opt for the continuing of said exemption to the subsequent examinations:

Provided that such candidate shall be required to obtain a minimum of fifty per cent. marks in each of the remaining paper or papers of that Group or Unit in order to declare him to have passed in that Group or Unit.

(9) The Council may adopt the criteria of negative marking in a paper or papers having objective type questions in such manner as may be specified by it from time to time.”.

18. In regulation 39, in sub-regulation (1), for clause (a), the following clause shall be substituted, namely: —

“(a) The result of each examination indicating whether a candidate has been successful or unsuccessful in the said examination shall be made available on the website of the Institute;”.

19. In regulation 40, in sub-regulation (1), the words “Accounting Technical Level” shall be omitted. 20. After regulation 40 of the said regulations, the following regulation shall be inserted, namely:—

“40A. Business Accounting Associate Certificate. — (1) A candidate shall be eligible for Business Accounting Associate Certificate, if he—

(a) passes both Group I and Group II of the Intermediate Examination;

(b) successfully completes Integrated Course on Information Technology and Soft Skills;

(c) completes the practical training as provided in these regulations; and

(d) successfully completes the self-paced online modules as provided in these regulations.

(2) A candidate shall pay such fees as may be fixed by the Council from time to time which shall not exceed five thousand rupees, along with an application in the form approved by the Council for the grant of Business Accounting Associate Certificate:

Provided that a candidate who is residing outside India shall pay such fees as may be fixed by the Council from time to time.

(3) A candidate, who has passed either the Intermediate Examination or Intermediate (Integrated Professional Competence) Examination or Integrated Professional Competence Examination or Intermediate (Professional Competence) Examination or Professional Competence Examination or Professional Education-II Examination, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, and was eligible for Accounting Technician Certificate, shall be eligible for making an application for Business Accounting Associate Certificate on fulfilling such other requirements as may be specified by the Council, from time to time.

(4) A candidate may apply for Business Accounting Associate Certificate on fulfilment of the criteria as specified by the Council from time to time.”.

21. In regulation 45 of the said regulations, in sub-regulation (1), —

(i) in clause (a), after the word and figures “regulation 43,”, the words “having regard to” shall be inserted;

(ii) in clause (b), in sub-clause (i),the words “either or” shall be omitted.

22. In regulation 48 of the said regulations, in sub-regulation (1), for the Table, the following Table shall be substituted, namely:—

“TABLE

| Classification of the Normal place of service of the articled assistant | During the first year of training | During the second year of training | During the third year of training | |||

| (1) | (2) | (3) | (4) | |||

| (i) Cities/Towns having population of twenty lakhs and above | Rs.4000/- | Rs.5000/- | Rs.6000/- | |||

| (ii) Cities/Towns having population of five lakhs and above but less than twenty lakhs | Rs.3000/- | Rs.4000/- | Rs.5000/- | |||

| (iii) Cities/Towns having a population of less than five lakhs | Rs.2000/- | Rs.3000/- | Rs.4000/- | ”. | ||

23. In regulation 50 of the said regulations, —

(i) in clause (i), for the words “three years”, the words “two years” shall be substituted;

(ii) for the proviso, the following proviso shall be substituted, namely: —

“Provided that a candidate who was registered as an articled assistant for a period of three years, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall be eligible to continue and complete the remaining period of practical training as per the deed of articles executed under these regulations irrespective of any break in the continuity of training.”.

24. In regulation 51 of the said regulations, —

(i) in sub-regulations (1), (4) and (9), for the words “eighteen months” at all the places where they occur, the words “twelve months” shall be substituted;

(ii) in sub-regulation (11), after the words, “industrial training”, the words “subject to a minimum of fifteen thousand rupees per month” shall be inserted;

(iii) after sub-regulation (11), the following sub-regulation, shall be inserted, namely: —

“(12) Notwithstanding anything contained in this regulation, an articled assistant who is already undergoing industrial training, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall be eligible to continue and complete the remaining period of industrial training as per agreement of training entered into under sub-regulation (6).”.

25. For regulation 51E of the said regulations, the following regulation shall be substituted, namely: —

“51E. Advanced Integrated Course on Information Technology and Soft Skills.— (1) An articled assistant shall undergo an Advanced Integrated Course on Information Technology and Soft Skills for such duration and in such manner as may be specified by the Council from time to time after completing the period of his practical training as per clause (i) of regulation 50 but before appearing in the Final examination.

(2) An articled assistant, registered on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall undergo an Advanced Integrated Course on Information Technology and Soft Skills for such duration and in such manner as may be specified by the Council from time to time, during the last two years of his practical training without any break in continuity.

(3) A candidate who has passed the Final Examination but not completed the Course on General Management and Communication Skills under these regulations, shall be required to complete the Advanced Integrated Course on Information Technology and Soft Skills before applying for membership of the Institute.”.

26. After regulation 51E of the said regulations, the following regulation shall be inserted, namely: —

“51F. Self-paced online modules.— (1) A candidate who has passed both the Groups of the Intermediate Examination shall be required to undergo and pass self-paced online modules consisting of such number of modules and in such manner as may be specified by the Council from time to time.

(2) A candidate shall be declared to have passed in the self-paced modules if he obtains a minimum of fifty per cent. marks in each module.”.

27. In regulation 54 of the said regulations, — in sub-regulation (5), for the word “eighteen”, the word “twelve” shall be substituted;

28. After regulation 54A of the said regulations, the following regulation shall be inserted, namely: —

“54AA. Practical Training of a candidate residing outside India.— (1) A candidate who is residing outside India, and registered for Final Course under these regulations, may undergo the practical training for the purposes of these regulations under an eligible member of such other accounting institutions or bodies outside India recognised by the International Federation of Accountants in such manner as may be determined by the Council from time to time.

(2) A candidate who has completed his practical training under sub-regulation (1) shall not be entitled to have his name entered in the register of members unless he has fulfilled such other criteria as may be specified by the Council from time to time.”.

29. In regulation 56 of the said regulations, in sub-regulation (1), for the first proviso, the following proviso shall be substituted, namely: —

“Provided that in the first year of such training, the articles so engaged may, by agreement between the articled assistant and his principal, be terminated and during the second year of training, the termination of articles shall be permitted if the articled assistant opts for industrial training or under such exceptional circumstances or conditions, as may be decided by the Council.”.

30. In regulation 59 of the said regulations, —

(i) for sub-regulation (1), the following sub-regulation shall be substituted, namely: —

“(1) An articled assistant shall be eligible for leave of twelve days in each year of his practical training.”;

(ii) sub-regulations (2), (4) and (5) shall be omitted;

(iii) in sub-regulation (7), in the Explanation, —

(a) in clause (1), for the words “Course on Information Technology Training, and Course on General Management and Communication Skills”, the words, figure and letter “course under regulation 51E” shall be substituted;

(b) clause (2) shall be omitted;

(iv) after sub-regulation (7), the following sub-regulation shall be inserted, namely:—

“(8) An articled assistant who is already registered, on or before the commencement of the Chartered Accountants (Amendment) Regulations, 2023, shall continue to be governed by the provisions of this regulation which were in force prior to their amendment and as per the deed of articles executed under these regulations.”.

CA. (DR.) JAI KUMAR BATRA, Secy.

[ADVT.-I I I/4/Exty./21 7/2023-24]

Note.—The principal regulations were published in the Gazette of India, Extraordinary, dated the 1st June, 1988 vide Notification number 1-CA(7)/134/88, dated the 1st June, 1988 and lastly amended vide Notification No. 1-CA(7)/198/2021, dated the 4th March, 2022.

Author Bio

Seems to be good for CA Students.