Case Law Details

Chamber of Tax Consultants through its President Mr. Vijay Bhatt Vs Director General of Income Tax (systems) (Bombay High Court)

In a significant ruling by the Bombay High Court, the Chamber of Tax Consultants, through its president, Mr. Vijay Bhatt, challenged the interpretation of Section 87A of the Income Tax Act, particularly in relation to Section 115BAC. The petitioners argued that the rebate under Section 87A should be applicable not only to the tax calculated under Section 115BAC but also to taxes computed under other provisions of Chapter XII, unless expressly prohibited by the Act. According to the petitioners, the total income for tax computation includes income from all heads, and taxes should be determined based on the aggregate income, not segregated into parts.

On the other hand, the Additional Solicitor General contended that Section 87A rebate should only be applicable to the tax calculated under Section 115BAC, as the section deals with simplified tax rates for those giving up exemptions and deductions. The respondent’s argument emphasized that Section 87A rebate is meant exclusively for tax determined under Section 115BAC, which is considered a special provision. The Court, after hearing extensive arguments, found that the provisions were ambiguous and insufficiently clear, prompting it to rule that the assessee should not be precluded from making a claim for the rebate, which could be adjudicated during the assessment process under Sections 143(1) and 143(3).

The Court highlighted that the issue at hand was not about which interpretation was correct, but about whether the tax authorities could use their administrative powers to prevent an assessee from making a debatable claim. The Court stressed that such claims should be decided judicially, not administratively, as denying an assessee the right to make a claim would be a violation of constitutional principles. Furthermore, the Court affirmed that technological processes should not inhibit an assessee’s right to assert their claim, as it is within their legal entitlement to do so, aligning with the constitutional guarantees under Articles 265 and 300A.

The Court’s ruling also acknowledged the complex and evolving nature of tax law, emphasizing that both tax authorities and assessees should have the opportunity to present their arguments. It was concluded that the modification of the utility, which blocked the claim under Section 87A, was unjustified at the threshold and violated the constitutional rights of the assessee. The Court’s stance underscored that disputed claims must be adjudicated fairly and not dismissed prematurely by administrative decisions.

FULL TEXT OF THE JUDGMENT/ORDER OF BOMBAY HIGH COURT

1. Rule. The Rule is made returnable immediately at the request of and with the consent of the learned counsel for the parties.

2. This Court, led by the learned Chief Justice on 20 December 2024, granted interim relief by directing the Central Board of Direct Taxes to issue notification for extending the due date for e-filing of the income-tax return to ensure that taxpayers eligible for the rebate under Section 87A are allowed to exercise their statutory rights without facing procedural impediments. Pursuant to the said direction, the Board issued a notification on 31 December 2024 extending the last date for furnishing returns under Section 139(4)/139(5) for the assessment year 2024-25 in the case of a resident individual from 31 December 2024 to 15 January 2025. Thereafter, on the matter being mentioned, an administrative order dated 10 January 2025 was passed assigning the said PIL to this Bench.

PETITIONERS:

3. The Chamber of Tax Consultants files this Public Interest Litigation (PIL) against the respondents through its President and taxpayer assessees. Petitioner No.1 is a society registered under the Societies Registration Act of 1860 and the Bombay Public Trusts Act of 1950. It has more than 3800 members comprising of Advocates, Chartered Accountants, and tax practitioners.

4. The objectives of petitioner No.1 are (i) to spread education in matters relating to tax laws and other laws and accountancy and allied subjects of professionals’ interest; (ii) to carry on activities for the extension of knowledge in the fields of tax laws and other laws, accountancy and allied subjects of professionals’ interest; (iii) to make representations to any government or non-government authority, committees, commissions and study teams, or at conferences or similar gatherings, (iv) to seek representation and appear before the tax and other law enforcement authorities, tribunals and courts in matters of public interest and in cases of importance to professionals and assessees in general, including taking up and pursuing public interest litigation.

5. Petitioners Nos. 2 to 4 are taxpayers and assessees under the Income-tax Act, 1961 (the Act). They are aggrieved by the subject matter of the petition and have joined petitioner No.1 in filing the present petition.

6. Petitioner No.1 has in the past filed several writ petitions to pursue the common cause affecting the administration of tax in India. It is in this background that the present PIL is filed jointly.

CAUSE OF PIL:

7. The cause for filing the present PIL arose on 5 July 2024. On that date, online utility provided by the respondents denied the assessees (who are clients of the members of the petitioner No. 1), the benefit of claiming a rebate under Section 87A of the Income-tax Act for the assessment year 2024-25 while filing online return against tax computed under various sections of Chapter XII of the Act. Before 5 July 2024, the respondents’ utility permitted the assessees to make such a claim. Petitioner No.1 and various other associations made various representations to respondents on the issue of utility not providing for making a claim under Section 87A but, having failed to get justice, have approached this Court for redressal of their grievances. It is this denial on account of the modification of the utility on and from 5 July 2024, which is challenged in the present petition.

PRAYERS SOUGHT FOR :

8. The prayers sought for in the Writ Petition read as under:-

(a) that this Hon’ble Court be pleased to issue a writ of mandamus or a writ in the nature of mandamus or any other appropriate writ, direction or order directing the Respondents to modify the utilities for filing of the return of income under section 139 of the Act immediately, thereby allowing assessees to make a claim of rebate under section 87A of the Act read with the proviso to section 87A, in their return of income for the AY 2024-25 and subsequent years including revised returns to be filed under section 139(5) of the Act.

(b) that this Hon’ble Court be pleased to issue a writ of mandamus or a writ in the nature of mandamus or any other appropriate writ, direction or order directing the Respondents to allow assesses to file a manual return of income for claiming rebate under section 87A of the Act in their return of income for the AY 2024-25 and subsequent years including revised returns to be filed u/s 139(5) of the Act.

[(c) that this Hon’ble Court be pleased to issue a writ of mandamus or a writ in the nature of mandamus or any other appropriate writ, direction or order directing the Respondents to make the utilities for filing the return of income online flexible so as to allow an assessee to self compute his/her income and there should not be any restriction on making of any claim whatsoever and to direct the Respondents to not release any utilities or make any changes in the utilities for filing of the Return of Income under section 139 of the Act which does not allow any assessee to raise any claim which it seeks to make/ raise in the return of income.

(d) that this Hon’ble Court be pleased to issue a writ of mandamus or a writ in the nature of mandamus or any other appropriate writ, direction or order and be pleased to direct the Respondents to:

(i) take appropriate steps to allow a claim of rebate under section 87A of the Act from tax payable at special rates except tax levied in accordance with section 112A of the Act, where the assessees have opted for the new tax regime enacted in section 115BAC of the Act, for those assessees who could not claim such relief in their returns already filed for the AY 2024-25 and to issue consequential refund in this regard.

(ii) take appropriate steps to allow a claim of rebate under section 87A of the Act from tax payable at special rates except tax levied in accordance with section 112A of the Act, where the assessees have opted for the new tax regime enacted in section 115BAC of the Act, for those assessees who have made claim of such relief in their returns already filed for the AY 2024-25 and where such returns are yet to be processed.

(iii) withdraw or modify the intimations already issued under section 143(1) of the Act processing the return of income, denying the claim of rebate under section 87A of the Act, from tax payable at special rates except tax levied in accordance with section 112A of the Act, where the assessees have opted for the new regime enacted in section 115BAC of the Act and to direct the Respondents to allow such claim.

(e) that this Hon’ble Court be pleased to issue a Writ of Prohibition or any other Writ, Order or Direction in Article 226 of the Constitution of India ordering and directing the Respondents not to implement the intimations already issued under section 143(1) of the Act processing the return of income, denying the claim of rebate under section 87A of the Act from tax payable at special rates except tax levied in accordance with section 112A of the Act.

(f) that pending the hearing and final disposal of this petition the Respondents, their subordinates, servants and agents be directed by an order of this Hon’ble Court:

(i) to change the utilities for filing of the Return of Income under section 139 of the Act immediately and forthwith allowing assessees to make a claim of rebate under section 87A of the Act in their return of income for the AY 2024- 25 and subsequent years including revised returns to be filed u/s 139(5) of the Act.

(ii) To restore the utility which was available before 05.07.2024 for filing return of income which allowed assessees to make a claim of rebate under section 87A of the Act in their return of income for the AY 2024-25 and subsequent years including revised returns to be filed under section 139(5) of the Act;

(iii) Or in the alternate, to allow filing of a manual return of income for claiming rebate under section 87A of the Act in the return of income for the AY 2024-25 and subsequent years including revised returns to be filed under section 139(5) of the Act.

(g) that pending the hearing and final disposal of this petition the Respondents, their subordinates, servants and agents be restrained by an order and injunction of this Hon’ble Court from implementing the intimations already issued under section 143(1) of the Act processing the return of income, denying the claim of rebate under section 87A of the Act from tax payable at special rates except tax levied under section 112A of the Act.

SUBMISSIONS OF THE PETITIONERS:

9. Mr. Pardiwala, learned senior counsel appearing for all the petitioners, led the attack and made various submissions and, on our request, has filed written submissions, which are reproduced herein: “For the sake of ease, the present submission is divided into two parts as under:

A. The Tax Department should make the utilities for online filing of return of income flexible so as to allow an assessee to self- compute his/her income and there should not be any restriction on making of any claim whatsoever. The Department cannot design the return as per their understanding of the law, so as to not allow an assessee from raising any claim in the return of income to be filed.

B. Rebate under the proviso to section 87A of the Income-tax Act, 1961, (‘the Act’), is also allowable from tax payable at special rates except tax levied in accordance with section 112A of the Act, where an assessee has opted for the new tax regime enacted in section 115BAC of the Act.

A. Larger issue of flexibility in filing return of income

1. Under the Act, there is a concept of self-assessment. An assessee has to compute his own income, determine the tax liability thereon, pay such tax and then, file his return declaring his total income and the tax on such income. The same is demonstrated hereunder:

i) As per section 207 and 208 of the Act, an assessee is required to pay tax in advance in the previous year relevant to the assessment year. As per section 209 and 210 of the Act, an assessee has to estimate his current income and then calculate the amount of advance tax to be paid in installments as provided for in section 211 of the Act. On failure to pay advance tax as per the provisions of the Act, an assessee is saddled with interest u/s 234B and 234C of the Act.

ii) Section 139 of the Act requires, inter alia, an assessee to furnish a return of his income in the prescribed form. Further, an assessee has to verify his return of income in the manner prescribed.

iii) The verification clause of any return form states as under:

“I,________, son/ daughter of solemnly declare that to the best of my knowledge and belief, the information given in the return is correct and complete and is in accordance with the provisions of the Income-tax Act, 1961. I further declare that I am making this return in my capacity as______ and I am also competent to make this return and verify it. I am holding permanent account number.”

Thus, an assessee has to declare in the return that the return filed is to the best of his knowledge and belief and is correct and complete and is in accordance with the provisions of the Act.

iv) Section 140A of the Act the heading of which is “Self- Assessment”, requires an assessee to pay tax with interest payable under the Act before furnishing the return of income and the return is to be accompanied with the proof of payment of such self-assessment tax. Such furnishing of proof is now dispensed with under the e-filing regime.

v) Without paying self-assessment tax, a return of income cannot be filed. Such return is also treated as defective in terms of section 139(9) of the Act.

2. The above provisions demonstrate that under the Act, an assessee is required to self-compute the income and the tax liability thereon as per his belief and understanding. Thus, the form of the return of income has to allow an assessee to declare and compute his income as per his belief and understanding.

3. The term “return” in the context of the Act refers to the act of reporting information to the government. By filing an income tax return, the taxpayer is “returning” or reporting their taxable income and tax liabilities to the government.

4. Moreover, in the return of income, an assessee also claims refund of taxes paid where the taxes paid are more than the taxes required to be paid. A return, therefore, is also a claim for refund under the Act, where taxes have been paid in excess of what is required to be paid.

5. This Hon’ble Court in case of Samir Narain Bhojwani vs. DCIT [(2020) 115 com 70 (Bombay)], has held in para 8 as under:

“The purpose and object of e-filing of return to have simplicity and uniformity in procedure. However, the above object cannot in its implementation result in an assessee not being entitled to make a claim of set off which he feels he is entitled to in accordance with the provisions of the Act. The allowability or dis-allowability of the claim is a subject matter to be considered by the Assessing Officer. However, the procedure of filing the return of income cannot bar an assessee from making a claim under the Act which he feels he is entitled to. We accept the Assessing Officer’s submission that in terms of Rule 12 of the Rules, the returns are to be filed by the petitioner only electronically and he is bound by the Act and the Rules, thus cannot accept the paper return. However, in terms of section 139D of the Act, it is for the CBDT to make rules providing for filing of returns of income in electronic form. This power has been exercised by the CBDT in terms of Rule 12 of the Rules. However, the form as prescribed do not provide for eventuality that has arisen in the present case and may also arise in other cases. Thus, this is an issue to be brought to the notice of the CBDT, which would in case it finds merits in this submission, issue necessary directions to cover this gap.”

6. Similarly, the Hon’ble Allahabad High Court in CIT vs. N. Khan and Bro. reported in [1973] 92 ITR 338 (Allahabad), has held in para 3 as under:

“Now, under section 139(1) a duty is cast upon every person to file a voluntary return if his income exceeds the maximum amount which is not chargeable to income-tax. The question arises as to which income is contemplated by this provision, the income which the assessee believes to be his income or which is finally assessed by the Income-tax Officer. It is clear that at the time when a person is required to file a voluntary return, no assessment has yet been made against him. He is thus to be guided by what he himself believes to be his income. It is possible and it happens very frequently that an assessee may not consider a particular item to be his income and yet the Income-tax Officer may hold otherwise. In such a case, if what he considers to be his income is less than the amount which is not chargeable to income-tax, he is not required to file a voluntary return even if the income finally assessed is more than the maximum amount which is not chargeable to income-tax. Of course, the belief of the assessee must be bona fide”

7. Similar view has been taken by the Hon’ble Supreme Court in case of CIT vs. Ranchhoddas Karsondas reported in [1959] 36 ITR 569 (SC). It has held as under:

“It is a little difficult to understand how the existence of a return can be ignored, once it has been filed. A return showing income below the taxable limit can be made even in answer to a notice under section 22(2). The notice under section 22(1) requires in a general way what a notice under section 22(2) requires of an individual. If a return of income below the taxable limit is a good return in answer to a notice under section 22(2), there is no reason to think that a return of a similar kind in answer to a public notice is no return at all. The conclusion does not follow from the words of section 22(1). No doubt, under that sub-section only those persons are required to make a return, whose income is above taxable limits, but a person may legitimately consider himself entitled to certain deductions and allowances, and yet file a return to be on the safe side. He may show his income and the deductions and allowances he claims. But it may be that on a correct processing his income may be found to be above the exempted limit. No doubt, it is futile for a person not liable to tax to rush in with a return, but the return in law is not a mere scrap of paper. It is a return, such as the assessee considers represents his true income.”

8. Thus, an assessee has to file his return of income and declare his income to the best of his knowledge, understanding and belief and declare such return to be correct and true. Such a process is possible only if the return permits an assessee with the flexibility to make whatever claims he feels he can make under the Act.

9. Section 295(2)(i) of the Act, empowers the Government to provide for rules or form and manner in which return may be furnished. The Government has prescribed rule 12 in this regard. Various Forms have been notified by the Government for filing of return of income. This is an annual exercise. There are various line items in the form and a corresponding cell to fill in the figures. It is submitted that the Department is not even empowered under the Act and the Rules to design a return in a fashion to disallow an assessee from making any claim. Neither the provisions of the Act, nor the provisions of the Rules, nor the Forms per se, prohibit or restrict an assessee from making any claim or restricting an assessee from putting any figure in the form. Thus, when the utility designed by Respondent No. 1 puts such fetters, the same is ultra vires the Act, Rules and the Forms notified.

10. It is submitted that vide rule 12(4), the role of Respondent No. 1 has been specified. It states “The Principal Director-General of Income-tax (Systems) or Director General of Income-tax (Systems) shall specify the procedures, formats and standards for ensuring secure capture and transmission of data and shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to furnishing the returns in the manners (other than the paper form) specified in column (iv) of the Table in sub-rule (3) and the report of audit or notice in the manner specified in proviso to sub-rule (2).”

Thus, the role of Respondent No. 1 is to only “ensure secure capture and transmission of data and for evolving and implementing appropriate security, archival and retrieval policies” in relation to furnishing the returns. It can in no manner prescribe a utility which prohibits or debars an assessee from making any claim in the return of income. This is irrespective of the fact that the claim made by an assessee may not be in accordance with the interpretation placed by the Tax Department on a statutory provision. Thus, when Respondent No. 1 designs a utility in a manner which is not allowing an assessee to make a claim under the Act, then, the said action is clearly contrary to the provisions of the Act read with the Rules.

11. It is submitted that a return cannot be designed in a fashion which prevents an assessee from making any claim of his/her choice. That is not the purpose of a return of income. The Respondents cannot design a return of income, based on their understanding of law. By not allowing an assessee to make a claim and thereby seeking from an assessee more tax than what he thinks is liable to pay, would violate the fundamental rights guaranteed under Article 14 of the Constitution of India. An assessee in such case, is compelled to show income which he does not believe to be correct and determine the tax liability which he does not believe to be correct and pay higher amount of tax and still declare and verify that the return is correct. Such an action is manifestly arbitrary and irrational and therefore, violative of Article 14 of the Constitution of India.

12. In fact, it even lead to treatment of equals as unequal’s. There are several instances where the Department does not agree with the view of the assessees taken in the return of income and make additions in the course of assessment proceeding. The return does not prohibit assessees from making the claim. However, when a particular assessee wants to make a claim in the return, which the system prohibits because as per the Department such claim is not maintainable, then he is being discriminated against as compared to the first assessee. This itself demonstrates violation of Article 14.

13. Further, it is submitted that such an action of the executive is also violative of Article 19(1)(g) of the Constitution of India which guarantees a citizen with a right to practice any profession or to carry on any occupation, trade or business. Such a fundamental right inherently includes a right to have a fair process to declare income under the Act and to pay correct tax, as per the understanding of the assessees. This is especially when the law requires an assessee to self-declare his income and tax liability.

14. Moreover, such an exercise of not allowing an assessee to make a claim in the return of income is violative of Article 265 of Constitution of India. Not following the concept of self-assessment and self- computation, by not allowing an assessee to make a claim of his choice, the Revenue would collect more tax than required, which would be violative of Article 265. Thus, the action of the Respondent No. 1 in not allowing an assessee to make a claim in the return of income per se, would be violative of Article 265 of the Constitution of India.

15. If a return of income prohibits an assessee from making a claim, then, it would amount to deciding the issue at the stage of filing return of income itself. The validity of such claim can be tested at the stage of assessment proceeding and if rejected, by agitating the matter through various appellate stages. Because of an interpretation of the Tax Department, it would be imperssible to not allow an assessee to make a claim in the return of income. The validity of a claim can be tested by an adjudicating or appellate authority including courts and tribunals. If an assessee is not allowed to make a claim per se because the Tax Department feels such a claim is not correct as per their interpretation, then, there is no requirement for appellate courts to exist. In fact, reference is made to the following provisions which show that, there are provisions to ensure that an assessee has not understated his income:

i) Section 143(1)(a) empowers the Respondent to make adjustments in the total income as disclosed in the return of income.

ii) Section 143(2) empowers the Respondent to select a case for scrutiny to ensure that the assessee has not understated the income or has not computed excessive loss or has not under- paid the tax in any manner. Such a notice is followed by an order of assessment either under section 143(3) or section 144 of the Act wherein the Assessing Officer shall, by an order in writing, make an assessment of the total income or loss of the assessee, and determine the sum payable by him or refund of any amount due to him on the basis of such assessment.

iii) Section 147 of the Act empowers an Assessing Officer to reopen an assessment if any income chargeable to tax has escaped assessment.

Thus, there are provisions to verify the correctness of the return of income filed by an assessee. Such verification or assessment should take place after a valid return of income is filed. By not allowing an assessee to make a claim in the return of income, the assessment process is given a goby and a suo moto determination made at the stage of filing of the return, which concept, is completely alien to the Act.

16. Moreover, if an assessee is not allowed to make a claim in the return of income, then, he would not be able to raise such a claim thereafter. If his case is not selected for scrutiny by issuance of a notice under section 143(2) of the Act, then, there is no remedy for making a claim. An assessee can probably opt for revision in terms of section 264 of the Act, of the intimation issued under section 143(1) of the Act by raising a new claim. However, in such revision proceeding, the Department is of the view that a new claim which is not raised in the return of income cannot be allowed to be raised for the first time. Thus, an assessee would be remediless if the revenue’s contention is upheld. If an assessee’s case is selected for scrutiny assessment, then, he cannot raise a claim for the first time in such assessment proceeding, as the Hon’ble Supreme Court in case of Goetze (India) Ltd. vs. CIT reported in [2006] 284 ITR 323 (SC) has held that no fresh claim can be raised other than by filing a revised return. Thus, it is imperative to allow an assessee to make whatever claim he wishes to make in the return of income and the utility should be designed in a fashion to allow the same. In fact, the judgment in the case of Goetze (supra) itself suggests that a claim has to be validly made in the return of income and by no other mode.

17. It is submitted that by not allowing an assessee to raise a claim in return, an assessee is denied a fundamental right to agitate an issue. This clearly amounts to violation of Article 14, 19(1)(g) and 265 of the Constitution of India.

18. It is submitted that in similar facts, this Hon’ble Court has allowed assessees to file a manual return by making a claim which was not available in the return to be filed online when the revenue refused to accede to the assessee’s request to modify the utility. The Petitioners have relied upon the orders of this Hon’ble Court in the case of Samir Bhojwani (supra) and in case of Lupin Limited vs. DCIT in WP No. 3565 of 2023 (order dated 26.03.2024). In fact, similar view is taken by this Hon’ble Court in Tata Sons Pvt. Ltd. vs. DCIT [WP No. 3109 of 2022 and 1296 of 2023] vide order dated 26.03.2024. The Ld. ASG had submitted to the contrary that in case of Tata Sons (supra), the assessee therein had withdrawn the writ petition.

19. The Ld. ASG argued that the returns cannot be modified to suit particular assessees view and that if anyone has any problem in filing of return of income, then, he can come to a Writ Court. Further, he argued that the Writ Court would decide whether the claim of the assessee is tenable or not and then, would decide whether he can make such claim in the return of income. Such an approach, it is humbly submitted, is never contemplated in law. Apart from the fact, that the Courts are already burdened with pending litigation, to ask a Writ Court to decide the issue even before such issue is ripe for consideration by an appellate court would be a travesty of justice. It is submitted that even so often various Courts hold that a person should not jump the queue, and that adjudication should be followed by the appellate process of CIT(A) and Tribunal and, only then, the matter should come to a High Court for consideration. Such a process is given a go by the Department by not allowing an assessee to make a claim and thereby, forcing such assessee to argue before this Hon’ble Court about the tenability of its claim so as to allow him to make such a claim in the return. Such a process, it is humbly submitted can be avoided, by a simple solution that the Department should allow an assessee to make a claim in return of income as per his choice and, then, to decide the tenability of such claim during the assessment proceeding.

20. In the affidavit in reply (without prejudice to our contention that the affidavit is filed by CPC, which is not the authority to deal with the designing of return of income and filing of return of income), from para 5, it can be deduced that the designing of return of income these days is based on the processing under section 143(1) of the Act. While the Petitioners are not in any manner suggesting that one should revert to a manual system and are not denying the inherent advantage of a faster processing of the return of income and faster release of refunds after processing, however, it may not be wrong to state that experience has shown that the processing of return of income under section 143(1) is not free from defects and some of the adjustments made in such processing are beyond the powers of CPC in terms of section 143(1). Moreover, any reply to the proposal to make an adjustment under section 143(1) and/ or any rectification request meets the same fate. Though no furor is raised over this as such assessees are free to approach the appellate authorities and the same is being done. Be that as it may, it is of utmost importance to note that the processing of return of income cannot be the guiding light to design the return of income. It is like the proverbial “putting a cart before the horse” concept. How the returns would be processed cannot be the basis to design the return. This itself shows the fundamental fallacy in designing the return of income.

21. It is submitted that if the electronic return does not allow an assessee to put forth his claim basis a perception of the revenue of the correctness of such claim, then, such return has to be categorized as arbitrary. It is a settled principle that humans cannot be made slaves of technology. Time and again, this Hon’ble Court and other Courts have come down heavily on the technological impediments causing harassment to assessees.

22. Here, the Petitioners are more concerned with the action of the Respondents in disabling an assessee from making a claim, which he feels he is entitled to. This is clearly a human action, as such claim was allowed to be made before 05.07.2024. The Petitioners only request that the utility that enables the returns to be filed should be designed in a fashion so that an assessee is at liberty to make any claim which it desires to make. The provisions of the Act and the Rules relied upon, have never empowered the Respondents to design the return in a format so as to deny any person from making a claim.

23. Without prejudice to the above, it is submitted that when such issues are highlighted by way of a representation (several representations were made by several reputed bodies of tax practitioners including the ICAI in the present case), then, atleast at such stage, the utilities should be modified to allow an assessee to file its return of income by making a claim of its choice.

24. During the course of hearing, the Ld. ASG had submitted that the Petitioners are seeking to go back to a manual era. It is very important to dispel this doubt at the threshold. There should not be an iota of doubt that the Petitioners do not seek to go back to the manual era. The Petitioner No. 1 has been very vocal about its support of the electronic system and has never complained about the same in any of the representations made over several years. The Petitioners, however, feel that there should not be any sort of curbs or restrictions in the online utility from entering a figure of an assessee’s choice. The online utility should not freeze any cell and debar any assessee from entering a figure or making a claim of his choice. The same is not sought to be cured/ rectified by reverting back to filing of a manual return but the issue can be easily resolved by modifying the utility and allowing the assessees to make a claim. Just as in the present case, the return utility before 05.07.2024 allowed an assessee to claim rebate under section 87A against income taxable at special rates. The same was modified and making of such claim was disabled. On the directions of this Hon’ble Court, the same was again enabled in January 2025. This itself signifies the contention of the Petitioner that modification of the return of income would not lead to a technological mess/ chaos or downfall of the electronic system as suggested by the Ld. ASG.

25. During the course of hearing, the Ld. ASG has submitted that making a claim in the return of income as per the bonafide belief of an assessee is neither a constitutional nor a statutory right. It is submitted that the said submission of the Ld. ASG is legally and factually incorrect as submitted hereinbefore. Moreover, he also submitted that even if such a right is considered to be a statutory right then it is subject to statutory restrictions. It is submitted that the Ld. ASG did not refer to any provision of law or rules which provides for any such restriction. On the contrary, as mentioned earlier, the action of Respondent No. 1 to not allow an assessee to make a claim on the return of income is contrary to the provisions of the Act and Rules framed thereunder.

26. In light of the above submission, to avoid inconvenience to the assessees and Courts, the Petitioner prays that the Rule should be made absolute in terms of prayer clause (c).

B. Allowability of rebate u/s 87A from tax levied at special rates, where new regime is opted for

27. The Respondents have, without prejudice to their contention on merits, allowed the assessees at large from claiming rebate as per the directions of this Hon’ble Court vide order dated 20.12.2024. The Ld. ASG has argued, in great detail, that the assessees are not allowed to make a claim of rebate under section 87A if some part of their total income is taxable at special rates.

28. It is submitted that, as noted by this Hon’ble Court in the order dated 20.12.2024, this petition concerns several lower middle and middle class assesses making a claim for relief ranging from Rs. 1 to Rs. 25,000/- of the tax payable by them. This may be a minor relief from an assessee’s perspective and would not be worth fighting at the appellate stages. It is therefore, prayed, that this Hon’ble Court puts this controversy to rest in this petition, so that there is clarity in the mind of the assessees at large about the reliefs they are eligible for in terms of section 87A of the Act.

29. It is submitted that an individual assessee is entitled to claim a rebate as per section 87A of the Act. The same is to be claimed from the tax payable on total income. The method for computation of income and tax liability in terms of the Act is as under:

i) first compute the income chargeable under different heads of income under Chapter IV;

ii) thereafter aggregate income and set off of intra head and inter head losses in terms of Chapter VI and arrive at the gross total income;

iii) subsequently, claim deductions under Chapter VI-A, from the gross total income and arrive at the total income;

iv) compute the tax liability on the total income as per the rates prescribed by the Finance Act of each year and/or as per the special rates prescribed and compute the “tax on total income”;

v) claim inter alia rebate under section 87A of the Act from the tax on total income;

vi) finally determine the tax liability.

30. As per section 87A of the Act, the conditions for claiming rebate, in respect of income being offered to tax under the new regime is as under:

i) total income of the assessee is chargeable to tax under section 115BAC(1A) of the Act, meaning thereby, new regime is applied;

ii) total income should not exceed Rs. 7,00,000/- ;

iii) rebate shall be allowable by way of deduction from the amount of income-tax (as computed before allowing the deductions under the said Chapter) on his total income with which he is chargeable for any assessment year;

iv) rebate shall be the lower of 100% of such income-tax or Rs. 25,000/-;

v) if the income exceeds Rs. 7,00,000/- and the income tax payable on such total income exceeds the amount by which the total income is in excess of Rs. 7,00,000/-, then, the assessee shall be entitled to a deduction from the amount of income-tax on his total income, of an amount equal to the amount by which the income-tax payable on such total income is in excess of the amount by which the total income exceeds Rs.7,00,000/-.

Thus, rebate under section 87A of the Act, is allowed from the tax on total income irrespective of the fact, whether the same is computed at special rates.

31. The term ‘total income’ is defined in section 2(45) as total amount of income referred to in section 5, computed in the manner laid down in the Act. There can be only one total income which is the sum total of all income under various heads of income. There is no provision that income taxable at special rates are not to form part of total income or is to form a separate total income. Rebate is allowable on the tax on total income, which represents a summation of tax payable at special rates and tax payable in accordance with the rates provided for in the relevant Finance Act or section 115BAC(1A). Thus, a plain reading of section 87A shows that it does not restrict the claim of rebate only from income taxable at normal rates and prohibits the same being granted when income taxable at special rates.

32. The Ld. ASG argued that there are two total income viz., one taxable u/s 115BAC(1A) of the Act and other total income taxable at special rates. It is humbly submitted that there is no such concept of two total income. In fact, the word “total” itself suggests that total income is the sum total or aggregate of all income of an assessee. The provision for different computation mechanisms under different heads of income and different rates of tax, are for different purposes. However, at the end of the day, there is only one total income comprising of all income. This also becomes clear from the title of Chapter VI i.e., “Aggregation of income and set off or carry forward of loss”. Further, section 80B (5) of the Act defines “gross total income” to mean the total income computed in accordance with the provisions of this Act before making any deduction under Chapter VIA of the Act. Moreover, this contention of the Ld. ASG is clearly not tenable in view of the express provisions of various sections of Chapter XII dealing with income taxable at special rates. All the sections which levy tax at special rates on a particular category of income like 111A, 112, 112A, 115A, 115AB, 115AC, 115ACA, 115AD, 115B, 115BB to 115BBJ clearly specify in the opening portion of relevant sections that “Where the total income of an assessee includes any income chargeable ….”. Thus, even the law contemplates that all income, whether taxable at special rates or normal rates, are part of total income. Reference may also be made to section 111A (2), 112(2), 112A(5) of the Act, wherein exception is made to not allow deduction under Chapter VIA from the special category of income. This was necessitated since deduction under Chapter VIA is allowable from gross total income and such gross total income includes income taxable at special rates.

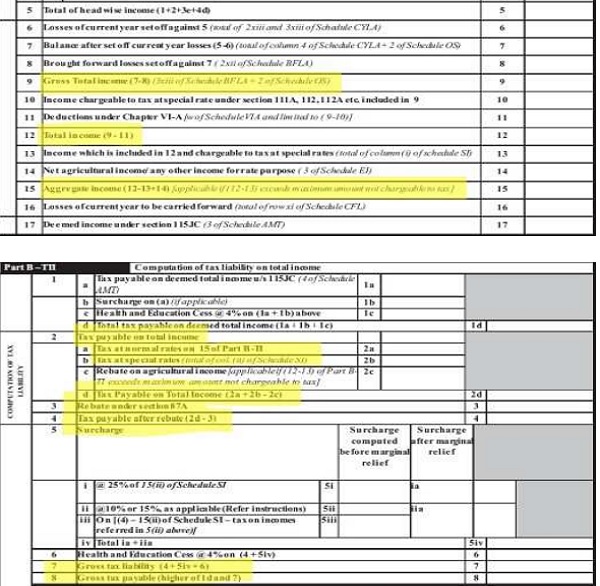

33. It will also be apposite to refer to the ITR form prescribed by the Central Government, especially the part which deals with computation of tax liability. For the sake of ease, an extract is brought out hereunder:

From the above also, it can be discerned that there is only one total income and one tax liability.

34. It is submitted that the concept of two “total income” is completely alien to the Act. In fact, acceptance of such an argument would have its own perils like:

a. Deductions under Chapter VIA are allowed from total income. While understanding total income, which income is to be seen?

b. Penalty is levied u/s 270A if there is any variation from total income. A formula is laid down for how to compute under- reporting of income where total income forms the starting point. While understanding total income, which income is to be seen?

35. It is submitted that wherever, the Legislature intended to not give any benefit to any category of income which forms part of total income or from tax at special rates, specific exceptions have been prescribed without violating the definition of the term “total income”. For instance, see section 80AB, 111A (2), 112(2), 112A(5) and 112A(6).

36. It is thus submitted that; rebate is allowable from total income including tax levied at special rates. If the Legislative Intent were to deny the rebate, then, a specific provision would have to be made either in section 87A or the relevant provision of Chapter XII providing for a special rate. There is no provision in section 87A of the Act that rebate shall not be allowed in respect of tax computed at special rates, say section 111A or 112 etc. of the Act. The proviso to section 87A deals with allowability of rebate to an assessee who has opted for the new regime. The proviso has nothing to do with the section under which the income is charged to tax. Clause (a) of the proviso, in no uncertain terms, state that “the assessee shall be entitled to a deduction from the amount of income-tax (as computed before allowing for the deductions under this Chapter) on his total income with which he is chargeable” Thus, rebate is allowable from the income tax on total income. It does not specify that such rebate is not available in respect of tax levied under section 115BAC(1A). The Respondents, therefore, are not right in taking a view that rebate is not allowable from tax levied at special rates either under the old regime or new regime.

37. The Respondent has harped on the opening wordings of the proviso i.e., “Provided that where the total income of the assessee is chargeable to tax under sub-section (1A) of section 115BAC” It is submitted that such opening portion is only a qualifying condition to enter the proviso, but the rebate is available from the income tax payable on total income as per clause (a) and (b). Further, the qualifying condition is that the person has opted for the new regime. The income tax payable on total income is the summation of the tax payable having regard to the applicable rates for different items of income.

38. Even section 115BAC is very clear to this effect. An extract of Section 115BAC(1A) is brought out hereunder:

“Notwithstanding anything contained in this Act but subject to the provisions of this Chapter, the income-tax payable in respect of the total income of a person, being an individual or Hindu undivided family or association of persons (other than a co- operative society), or body of individuals, whether incorporated or not, or an artificial juridical person referred to in sub-clause (vii) of clause (31) of section 2, other than a person who has exercised an option under sub-section (6), for any previous year relevant to the assessment year beginning on or after the 1st day of April, 2024, shall be computed at the rate of tax given in the following Table, namely: —

……………….”

Thus, it can be seen that the total income of a person is taxable under section 115BAC(1A). It is only for rate purposes in respect of certain categories of income, one has to go to other sections of Chapter XII, otherwise, total income is taxable under section 115BAC(1A) of the Act. A combined reading of the proviso to section 87A and section 115BAC(1A) also gives the same interpretation that where a person opts for new regime rebate shall be allowed from tax on total income, irrespective of the fact that any income is taxable at special rates.

39. Section 115BAC (2) provides for conditions to fall within section 115BAC(1A). A person, to opt for a new regime, has to give up on various deductions / exemptions/ allowances etc. However, reference to rebate under section 87A is conspicuously absent in section 115BAC(2). In fact, vide Finance Act 2023, the Legislature provided for higher rate of rebate for a person opting for new regime. Thus, there is no express bar from claiming rebate from tax chargeable at special rates.

40. It is submitted that the sections providing for payment of tax at special rates also do not provide for non-allowability of rebate in terms of section 87A as a condition to be fulfilled for availing of the special rate. There are specific provisions made in sections111A, 112 etc., which provide that a deduction under Chapter VIA would not be allowed if the special rate is applied. Likewise, section 115BAC provides that no set off of loss is also permissible. However, there is no specific mention of rebate under section 87A not being allowed against tax levied under these sections. It is most important to note that only section 112A of the Act, which provides for the rate of tax applicable on the capital gains arising on the transfer of a long term capital asset being an equity share in a company or a unit of an equity oriented fund or a unit of a business trust, provides for non-allowability of rebate under section 87A of the Act. A fortiorari, a rebate under section 87A has to be allowed from tax levied at special rates under other sections. Thus, the view of the Respondent that rebate is not allowable from tax which is taxable at special rates is not valid and should not be countenanced.

41. Moreover, the interpretation of the Respondents is in fact, contrary to the intention of the Legislature which is evident from the explanatory memorandum to the Finance Bills and also the Budget Speech of the Hon’ble Finance Minister. The same, for the sake of convenience, is brought out hereunder:

i) Budget Speech for the FY 2013-14

“125. The rates of personal income tax have survived four Finance Ministers and four Governments. The current slabs were introduced only last year. Hence, I am afraid, there is no case to revise either the slabs or the rates. Besides, even a moderate increase in the level of threshold exemption will mean that hundreds of thousands of tax payers will go out of the tax net and the tax base will be severely eroded. Nevertheless, I am inclined to give some relief to the tax payers in the first bracket of `2 lakh to `5 lakh. Assuming an inflation rate of 10 percent and a notional rise in the threshold exemption from `2,00,000 to `2,20,000, I propose to provide a tax credit of `2,000 to every person who has a total income upto `5 lakh. 1.8 crore tax payers are expected to benefit to the value of `3,600 crore”

ii) Explanatory memorandum to Finance Bill 2013

“With a view to provide tax relief to the individual tax payers who are in lower income bracket, it is proposed to provide rebate from the tax payable by an assessee, being an individual resident in India, whose total income does not exceed five lakh rupees.”

iii) Budget Speech for the FY 2016-17

“Relief to small tax payers 118. In order to lessen tax burden on individuals with income not exceeding `5 lakhs, I propose to raise the ceiling of tax rebate under section 87A from `2,000 to `5,000. There are 2 crore tax payers in this category who will get a relief of `3,000 in their tax liability.”

iv) Explanatory memorandum to Finance Bill 2016

“Rationalization of limit of rebate in income-tax allowable under Section 87A The existing provisions of section 87A of Income-tax Act, provide for a rebate of an amount equal to hundred per cent of such income-tax or an amount of two thousand rupees, whichever is less, from the amount of income-tax to an individual resident in India whose total income does not exceed five hundred thousand rupees. With the objective to provide relief to resident individuals in the lower income slab, it is proposed to amend section 87A so as to increase the maximum amount of rebate available under this provision from existing Rs.2,000 to Rs.5,000.”

v) Budget Speech for Interim Budget for the FY 2019-20

“60. Reducing the tax burden on middle class has always been our priority ever since our Government took over in 2014. We increased the basic exemption limit from Rs. 2 lakh to Rs. 2.5 Lakh and gave tax rebate so that no tax was payable by persons having income up to Rs.3 lakh.”89. Individual taxpayers having taxable annual income up to ` 5 lakhs will get full tax rebate and therefore will not be required to pay any income tax. As a result, even persons having gross income up to ` 6.50 lakhs may not be required to pay any income tax if they make investments in provident funds, specified savings, insurance etc. In fact, with additional deductions such as interest on home loan up to ` 2 lakh, interest on education loans, National Pension Scheme contributions, medical insurance, medical expenditure on senior citizens etc., persons having even higher income will not have to pay any tax. This will provide tax benefit of ` 18,500 crore to an estimated 3 crore middle class taxpayers comprising self employed, small business, small traders, salary earners, pensioners and senior citizens.”

vi) Budget Speech for FY 2019-20

“Moderation of tax rates: It is an ongoing endeavour of the Government to moderate the tax rate in order to reduce the tax burden and increase compliance. In this direction, following major steps have been taken: (i) 100% tax rebate was provided to individuals having taxable income up to Rs. 5 lakh. Thus, no income-tax is payable by an individual having taxable income up to Rs. 5 lakh.”

vii) Budget Speech for FY 2023-24

“146. The first one concerns rebate. Currently, those with income up to ` 5 lakh do not pay any income tax in both old and new tax regimes. I propose to increase the rebate limit to` 7 lakh in the new tax regime. Thus, persons in the new tax regime, with income up to ` 7 lakh will not have to pay any tax.

Annexure to Part B of the Budget Speech 2023-24

Resident individual with total income up to ` 5,00,000 do not pay any tax due to rebate under both old and new regime. It is proposed to increase the rebate for the resident individual under the new regime so that they do not pay tax if their total income is up to ` 7,00,000.”

viii) Explanatory memorandum to Finance Bill 2023 “IV. Rebate under section 87A

ix) Under the provisions of section 87A of the Act, an assessee, being an individual resident in India, having total income not exceeding Rs 5 lakh, is provided a rebate of 100 per cent of the amount of income-tax payable i.e., an individual having income till Rs 5 lakh is not required to pay any income-tax.

x) From assessment year 2024-25 onwards, an assessee, being an individual resident in India whose income is chargeable to tax under the proposed sub-section (1A) of section 115BAC, shall now be entitled to a rebate of 100 per cent of the amount of income-tax payable on a total income not exceeding Rs 7 lakh”

Thus, from the above, it can be deduced, that the intention always was that rebate is to be allowed from tax on total income without any conditions, whether any income is taxable at a special rate or the normal rate. The purpose of the rebate is to provide reliefs to small taxpayers whose income does not exceed say Rs. 5,00,000/- or Rs. 7,00,000/-. Instead of increasing the basic exemption limit, rebate is provided, so that such assessees would get the benefit whereas the assessees whose income exceed such limit for claiming rebate, they do not get any relief, and they still have to pay tax on the income below such limit of Rs. 5,00,000/- or Rs. 7,00,000/-. The treatment of the Respondents of not providing rebate under section 87A from tax chargeable at special rate under the new regime, is neither flowing from the plain interpretation of section 87A, nor from the intention of the Legislature. Merely because some income is taxable at different rates, does not mean that the rebate should be denied in respect of such income. Therefore, such an interpretation of the Respondents should not be countenanced.

43. If the interpretation of the Department is accepted, which is what the utility is doing right now, then, even an assessee with short term capital gains of Rs. 10,00,00,000/- on which the tax payable would be in accordance with the provisions of section 111A and income of Rs. 7,00,000 taxable at the rates provided for in section 115BAC(1A) would be eligible to a rebate of Rs. 25,000/-. Thus, even if the assessee is a rich man having substantial income, still the Departments interpretation is allowing rebate to such person, which is contrary to the avowed object of allowing rebate to small persons.

44. In fact, the first proviso to section 87A allows rebate being lower of amount of tax or Rs. 25,000/- whichever is less. If the tax is levied under section 115BAC(1A), then, the tax would never be more than Rs. 25,000/- on income upto Rs. 7,00,000/- Tax would be more than Rs. 25,000/- only if income is taxed at special rates. This itself suggests that the Act contemplates that rebate is also available on tax calculated on income taxable at special rates.

45. The Respondents have accepted that if income is taxable under the old regime, then, rebate is available against all categories of income. All income which is taxable at special rates i.e., under section 111A, 112, 112A etc. continue to apply, whether under old regime or under new regime. Thus, to allow rebate under the old regime and not allow the same under the new regime in respect of tax levied at special rates, itself is discriminatory and violative of Article 14. This is also against the intention of the Legislature to push people to go under new regime.

46. There is no legal basis to say that the plain reading of the proviso to section 87A gives only one interpretation that rebate is available only in respect of tax leviable under section 115BAC(1A) of the Act. The Petitioner has also annexed to the Petition, representations made by other professional bodies which makes it clear that the professional fraternity including the ICAI, are of the same view in contrast to the view of the Respondent

47. Thus, clearly, the interpretation of the Respondent is not tenable and therefore, should not be countenanced. The benefits available under the Act to small taxpayers should be allowed to them without any fetters.

48. An intimation under section 143(1) denying such claim of rebate, is in contravention of law, is invalid and, therefore, ought to be quashed and set aside. Further, the Respondents should be directed to not make any such disallowance in any future processing and to reverse the disallowance of claim already made by the Respondents. Consequential refunds to the assessees should be granted immediately with interest as per law.

49. In light of the above submission, the Petitioners humbly pray that the Rule should be made absolute in terms of prayer clause (a) and (d).

SUBMISSIONS OF THE RESPONDENTS :

10. Mr. Venkatraman learned Additional Solicitor General (ASG) of India, vehemently defended the action of the respondents and has filed written submissions which read as under:

1. The main clause of Section 87A of the Income Tax Act, 1961 provided a tax rebate of Rs. 12,500 for such of those individuals whose income was below Rs. 5 Lakhs. The Section provided a maximum rebate of Rs. 12,500. The rationale behind this incentive is two-fold. There is a threshold exemption from Income-tax up to Rs. 2.5 lakhs. Between Rs. 2.5 Lakhs and Rs. 5 Lakhs, the Rate of tax is 5%, which would be Rs. 12,500. Instead of extending the exemption limit up to Rs. 5 Lakhs, the Act conceives the mechanism of a rebate to ensure that Assessees earning an income of Rs. 5 Lakhs do not pay Income-tax, yet those assessees whose income is above Rs. 2.5L would still file returns, but would be granted a rebate from Income-tax.

2. With effect from April 2021, Parliament brought a new optional scheme for payment of Income-tax by individuals and HUFs on gross income basis, but at reduced rates of tax through Section 115BAC(1) of the Act. Broadly, this optimal scheme envisaged the following:

a. It would apply to individuals and HUFs.

b. those who avail Section 115BAC shall have to forgo certain deductions and exemptions as stipulated under Section 115BAC(2).

c. Such assessees are entitled to pay tax at the reduced rate on their total income.

3. However, Section 115BAC(1) envisaged a non-obstante clause overriding all the provisions of the Income Tax Act, 1961, of course subject to the provisions under Chapter 12. In other words, the override was against the entire Act, except the provisions of Chapter 12.

4. With effect from 01.04.2024, Parliament introduced clause (1A) to Section 115BAC which envisaged the following:

a. With effect from 01.04.2024, Section 115BAC(1A) became the default scheme for payment of Income-tax, unless otherwise an assessee chooses to opt the old regime and does so in terms of Section 115BAC(6) of the Act.

b. This default scheme became mandatory unless opted out by virtue of Sub-clause (6) to individuals, HUF, Association of persons (other than a cooperative society), Body of individuals whether incorporated or not or an Artificial Juridical Person referred to in Sub-clause (vii) of Clause (31) of Section 2 of the Act.

c. Sub-clause (1A) again could override all the provisions of the Income Tax Act, 1961 except the provisions of this Chapter namely Chapter 12. This is self-evident by virtue of the expressions “notwithstanding anything contained in this act but subject to the provisions of this chapter”.

d. Those who come under this default scheme of Section 115BAC(1A) would have to forgo those deductions and exemptions stipulated under clause (2) and would be entitled to pay Income-tax at the reduced rates as prescribed in sub-clause 1A of the said Section.

5. On the introduction of Clause 1A to Section 115BAC which was with effect from 01.04.2024, Parliament simultaneously introduced a proviso to Section 87A which also came into effect from 01.04.2024 extending the threshold rebate to a total income of Rs. 7 lakhs and doubling the quantum of rebate from Rs. 12,500 to Rs. 25,000, in line with the schedule of rates prescribed under Sub-clause 1A to Section 115BAC.

6. Therefore, post 01.04.2024, assessees whose income is less than 5L could claim a rebate of 12,500 in terms if the Main clause of Section 87A and those Notified under Section 115BAC(1A) would be entitled to a rebate of Rs. 25,000 upto an income of Rs. 7 Lakh by virtue of the proviso to Section 87A.

7. Sub-clause (b) to the proviso to Section 87A gives a reduced marginal rebate beyond Rs. 7 Lakhs and up to Rs. 7.4 Lakhs (this issue is inconsequential in this matter and therefore not elaborated further).

8. Following questions arises for consideration and interpretation by this Hon’ble Court:

a. What does the expression “subject to the provisions of this chapter” in Clause 1A of Section 115BAC would mean and whether this rigor would apply even to the proviso to Section 87A in computing the total income of Rs. 7 Lakhs?

b. How should the expression “total income” be construed in light of the expression “subject to the provisions of this chapter”?

9. Taking the 1st question, clause 1A of Section 115BAC though overrides all other provisions of the Income Tax Act, 1961, is still subject to the provisions of this chapter (namely provisions of Chapter 12).

10. Now taking the 2nd question, the interplay of the expression “total income” with the expressions “subject to the provisions of the Act”, Clause 1A in no uncertain terms, makes it clear that total income as specified in the said sub-clause would only mean total income subject to the provisions of this Chapter.

11. There is no contest or disputes by either sides that the total income which is spread over many heads such as, salary, income from house property, capital gains, income arising out of search, unaccounted income etc., have all been captured independently under various provisions of Chapter 12. Chapter 12 comprises of Sections 110 to 115BBJ and have captured short term capital gains, long term capital gains, royalties, profits and gains of life insurance business, tax on lotteries, anonymous donations, incomes referred to in Sections 68, 69, 69A, 69B, 69C and 69D (Section 115BBE), income from transfer of carbon credits, Income from virtual digital asset etc., as special incomes with independent rates of taxation.

12. There is no dispute on the fact that incomes falling under various Sections of Chapter 12 (Section 110-115BBJ), would all finally get assimilated to form total income.

13. Two things are therefore apparent and evident from a plain reading of clause 1A of Section 115BAC:

a. Total income is one which is scattered over various provisions of Chapter 12 and what is taken into reckoning for reduced rates of taxation are only such categories of total income which would fall under clause (1A) of Section 115BAC, excluding every other total income falling under other Sections of Chapter 12. This interpretation is inevitable for the simple reason that though clause (1A) is a notwithstanding clause, and the override is across the Income Tax Act, 1961 but with one singular limitation that the same is still subject to the provision of Chapter 12. In other words, clause (1A) does not override Sections 110 to 115BBJ of Chapter 12.

b. Once this is clear, the second inference in natural and consequential. Only such of those total income which falls under clause (1A) will get the benefit of reduced rate of taxation while such of those total income falling under other provisions of Chapter 12 will continue to be taxed at the specified rates referred to in those respective provisions.

14. Even though both sets of income, one falling under clause (1A) and the rest falling under other provisions of Chapter 12 would constitute elements of total income, the segregation and treatment for such total income falling under clause (1A) and rest of the provisions of Chapter 12 are distinct and different.

15. Once this interpretation passes the muster, let us turn our attention to the proviso to Section 87A.

16. The unambiguous expression employed in the proviso to Section 87A is as follows:

“Provided that where the total income of the assessee is chargeable to tax under sub-section (1A) of section 115BAC, and the total income”

17. It is clear from the above that the benefit of rebate of Rs. 25,000 on a total income of Rs. 7 lakhs would only mean such total income which falls under clause (1A) of Section 115BAC and would not include total income falling under other provisions of Chapter 12, namely Sections 110-115BBJ.

18. The computation form available in the portal is perfectly in synch with clause (1A) of Section 115BAC read with the proviso to Section 87A. An illustration would explain the provisions adequately. If an individual earns a total income of Rs. 6 lakhs constituting as total income under clause (1A) of Section 115BAC and an income of Rs. 1 Lakh as found under Section 115BBE, the later income falling under Section 115BBE cannot constitute as total income under clause (1A) of Section 115BAC. It would nevertheless be total income, but not total income falling under clause (1A) of Section 115BAC.

19. Therefore in terms of the proviso to Section 87A, the extent of rebate under clause (1A) of Section 115BAC can be extended only up to Rs. 6 Lakhs and cannot be extended to the income falling under Section 115BBE. This interpretation is legal and legitimate emanating from the plain language of clause (1A) of Section 115BAC read with the proviso to Section 87A.

20. The interpretation sought to be made by the assessees that clause (1A) of Section 115BAC is only for rates and cannot be taken cognizance of, for total income is unsustainable in law and the fallacy is self-revealing in view of the following:

a. Income Tax Act, 1961 can apply rates only on total income and not in abstract.

b. Chapter 12 comprises of Section 110-115BBJ envisages income from various streams which would form part of total income for the purpose of taxation.

c. The assumption that clause (1A) of Section 115BAC has assimilated all the income arising out of Chapter 12 as total income within one single bucket, namely clause (1A) is clearly wrong. The contrary is well espoused by clause (1A). It makes it abundantly clear that only such total income other than the total income falling under other provisions of chapter 12 would alone get captured under clause (1A) and only those total income would have the preferential rate of taxation, while the rest of the total income spread across chapter 12 would be get assessed as per those provisions.

21. It is therefore very clear that both in the case of total income as well as preferential rate of taxation, a clear distinction is made between clause (1A) of Section 115BAC and rest of the provisions, and therefore the submissions by the assessees that clause (1A) is only with reference to rates and not total income is unsustainable.

22. Now coming to the proviso to Section 87A, here again the reference is only to total income falling under clause (1A) of Section 115BAC, whereas the assesses contended that the same should be read as total Income of the assessees chargeable to tax under Chapter 12. Such an interpretation goes contrary to the plain language of Section 87A, and an invitation to such an interpretation through a judicial order is nothing but suggesting a rewriting of a Parliamentary provision through a judicial pronouncement which is unacceptable in our jurisprudence. Judicial legislation is an impermissible exercise and a clear encroachment of the sovereign powers of the Parliament, and therefore such an interpretation needs to be eschewed by this Hon’ble Court.

23. Now coming finally to the omnibus prayer of the Petitioners that they are entitled to file a return as per their belief and choice, the same again is unsustainable for the following reasons:

d. Canons of interpretation had reiterated the well settled principle as to when would a mandamus be issued. A mandamus would lie only when:

i. A party has an enforceable right

ii. Or an authority has statutory duty, obligation or a public duty to discharge and has failed to do so

iii. Consequently, enforcement of a Mandamus would arise only when there is a right available and there has been a failure to discharge and statutory duty or obligation.

e. A plain reading and interpretation of clause (1A) to Section 115BAC read with the proviso to Section 87A, and the electronic form to be filled up by the assessee would show a perfect synch and harmony without any disparity or inconsistency.

f. When the form in question is in line with the statutory provisions, where does the assessee get a right, and that too, an enforceable right of Mandamus to file a claim which can even be a wrong or illegitimate claim.

g. Reliance placed by assessees on judgements rendered during the pre-electronic era would have no bearing in a regime wherein the portal envisages filing of returns by crores and crores of assessees in line with the statutory mandate.

h. More than 8.5 crore assessees file returns online and there are more than 25 High Courts in this country. None of the assessee have come forward to challenge the existing electronic digitised system with least manual interference capturing returns, processing them and issuing deliverables on time with absolute accuracy.

i. Homogeneity and uniformity besides consistency are much needed virtues for a highly digitised system or gateway to function, may it be an income-tax portal or a GST portal, which are considered the largest gateways in the world.

j. The contention of the petitioners that even if law gets settled against the petitioners, still they should be vested with a right to file a return which they believe it to be correct has to be rejected outright in an electronic regime, which has exhibited high level of accuracy and performance. If returns have to allowed to be filed based on one’s belief and not based on statutory provisions and mandate, endless and countless types of returns would get filed which cannot be assimilated and processed in a digitised mechanism.

k. Constitutional democracy permits only enforcement of rights guaranteed either as Constitutional Right or Fundamental Right or as a Statutory Right. The exposition that one’s belief should accrue as a right to a citizen is too vulnerable and dangerous a proposition to be sustained.

l. If every belief of an assessee becomes an automatic right under the Income Tax Act, 1961, it would be the end of era of Constitutional democracy and beginning of era of Constitutional anarchy. This whole attempt is to push a well-functioning digitised system into a stone age, make it dysfunctional, unworkable and meaningless, and all of this is at what price? only to nurture the belief of an assessee and not the right of an assessee.

m. Upholding this plea would sabotage the existing farmwork of operation and implementation leading to disastrous consequences, more so when the Writ Petition is pursuing an academic exercise without any underlying issue in principle and wants to secure an omnibus open ended relief for times to come without any assessee being aggrieved in any manner.

n. Such open ended mandamus is uncalled for and undesired. Constitutional courts should never decide academic questions nor should grant reliefs without an underlying issue to deal with.

o. Weighing the options, grant of relief prayed for would collapse the digital operation and implementation when no one has found fault with it.

p. With a sense of responsibility that this pursuit is not made anywhere else in any other High Court, but being tried consistently before this Hon’ble Court.

q. The petitioners placed reliance on the interim order passed in the case of Lupin Limited v. Deputy commissioner of Income Tax, W.P(L) 38926 of 2022, dated 16.12.2022, wherein this Hon’ble Court permitted the assesses to file paper returns as an interim measure. A copy of the order dated 16.12.2022 is annexed herewith and marked as EXHIBIT R-1. Attention is also drawn to a similar order dated 2711-2022 in WP (L) No. 2570 of 2022 [Final No. WP/3109/2023] passed in the case of Tata Sons Pvt Ltd in WP wherein they were permitted to file paper returns. A true copy of the said order dated 16.12.2022 in WP (L) No. 2570 of 2022 in Tata Sons Pvt Ltd is annexed herewith and marked as EXHIBIT R-2. Both these matters came up for final hearing before this Hon’ble court on 26.03.2024.

r. Attention is also drawn to a similar order in the case of Tata & Sons v. Deputy commissioner of Income Tax in WP No. 3109 of 2022 wherein they were permitted to file paper returns. Both these matters came up for final hearing before this Hon’ble court on 26.03.2024 and in the case of Lupin (supra), since the assessments were completed based on the decision of the Hon’ble Supreme Court, the returns were processed and nothing remained pending in the Writ Petition and the same was disposed of. A copy of the said order passed on 26.03.2024 in WP No.3565/2023 in Lupin Ltd is annexed herewith and marked as EXHIBIT-R-3.

s. Whereas, in the case of Tata (supra) , the same Bench on the very same day allowed the petitioners to withdraw and purse alternative remedy. The assessees had to resort to this remedy since it was pointed out that there was no fallacy in the law or in the digitised system, However, in both these matters, the core argument which was attempted was the right to file a return in any manner based on one’s belief. A copy of the said order dated 26-03-2023 in WP No. 3109 of 2022 in Tata Sons Pvt Ltd is annexed herewith and marked as EXHIBIT-R- 4.

t. This Hon’ble court after hearing both parties for a full day decided not to grant the prayer of the petitioners and as petitioners advocate advanced the argument of pursuing an alternate remedy available to them, this Hon’ble Court allowed the petitioners to have the writ petitions and in accordance closed Writ Petition No. 3109 of 2022, and whereas the same was also followed in the case of Lupin in Writ Petition No. 3565 of 2023 & Writ Petition No. 32741 of 2023 since assessments stood completed already.

u. This Hon’ble Court did not recognise or approve the contentions of the petitioners for an open ended filing of returns after taking on record the detailed affidavit filed by the Revenue bringing out the operational mechanisms of the digitised systems.

v. Knowing fully well that this Hon’ble court had not yielded, one more vexatious attempt is sought to be made seeking the same prayer and relief for the 3rd time.

w. This attempt to frustrate a well performing digitised system needs to be rejected and its therefore most humbly prayed that this Writ Petition needs to be rejected.

ANALYSIS AND REASONING:

11. Relevant provisions which arise for our consideration are Section 87A and Section 115BAC which read as under:

Section 87A- Rebate of Income-tax in case of certain individuals:-

An assessee, being an individual resident in India, whose total income does not exceed [five hundred thousand] rupees, shall be entitled to a deduction, from the amount of income-tax (as computed before allowing the deductions under this Chapter) on his total income with which he is chargeable for any assessment year, of an amount equal to hundred per cent of such income-tax or on amount of [twelve thousand and five hundred] rupees, whichever is less:]

[Provided that where the total income of the assessee is chargeable to tax under sub-section (1A) of section 115BAC, and the total income-

(a does not exceed seven hundred thousand rupees, the assessee shall be entitled to a deduction from the amount of income-tax (as computed before allowing for the deductions under this Chapter) on his total income with which he is chargeable for any assessment year, of an amount equal to one hundred per cent of such income-tax or an amount of twenty-five thousand rupees, whichever is less; (b) exceeds seven hundred thousand rupees and the income-tax payable on such total income exceeds the amount by which the total income is in excess of seven hundred thousand rupees, the assessee shall be entitled to a deduction from the amount of income-tax (as computed before allowing the deductions under this Chapter) on his total income, of an amount equal to the amount by which the income-tax payable on such total income is in excess of the amount by which the total income exceeds seven hundred thousand rupees.

Section 115 BAC- Tax on income of individuals [, Hindu undivided family and others]

(1) …………………

(1A) Notwithstanding anything contained in this Act but subject to the provisions of this Chapter, the income-tax payable in respect of the total income of a person, being an individual or Hindu undivided family or association of persons (other than a cooperative society), or body of individuals, whether incorporated or not, or an artificial juridical person referred to in sub-clause(vii) of clause (31) of section 2, other than a person who has exercised an option under sub-section (6), for any previous year relevant to the assessment year beginning on or after the 1st day of April, 2024, shall be computed at the rate of tax given in the following Table, namely:-

TABLE

| Sr. No. (1) | Total income (2) | Rate of tax (3) |

| 1. | Upto Rs. 3,00,000 | Nil |

| 2. | From Rs. 3,00,001 to Rs. 6,00,000 | 5 per cent |

| 3. | From Rs. 6,00,001 to Rs. 9,00,000 | 10 per cent |

| 4. | From Rs. 9,00,001 to Rs. 12,00,000 | 15 per cent |

| 5. | From Rs. 12,00,001 to Rs. 15,00,000 | 20 per cent |

| 6. | Above Rs. 15,00,000 | 30 per cent |

Following sub-section (1A) shall be substituted for the existing sub-section (1A) of section 115BAC by the Finance (No. 2) Act, 2024, w.e.f. 1-4-2025:

(1A) Notwithstanding anything contained in this Act but subject to the provisions of this Chapter, the income-tax payable in respect of the total income of a person, being an individual or Hindu undivided family or association of persons (other than a co-operative society), or body of individuals, whether incorporated or not, or an artificial juridical person referred to in sub-clause (vii) of clause (31) of section 2, other than a person who has exercised an option under sub-section (6),-

(i) for any previous year relevant to the assessment year beginning on the 1st day of April, 2024, shall be computed at the rate of tax given in the following Table, namely:-

TABLE