1. Introduction

Related party transactions (RPTs) have long been viewed as potential sources of financial misstatements, manipulation, and conflict of interest. In response, regulators worldwide, including the ICAI, have prescribed accounting standards to ensure transparency in financial statements. In India, Accounting Standard 18 (AS 18) governs the disclosure requirements for related party relationships and transactions under the AS framework, whereas Ind AS 24, aligned with IAS 24, applies under the Ind AS regime.

2. Fundamental Concepts and Objectives

The primary objective of AS 18 and Ind AS 24 is to ensure that financial statements contain the disclosures necessary to draw attention to the possibility that the reported financial position and performance may have been affected by the existence of related parties and by transactions with such parties.

Key objectives include:

– Enhancing transparency of financial transactions.

– Ensuring comparability and faithful representation of financial statements.- Detecting potential conflict of interest and influence over financial results.

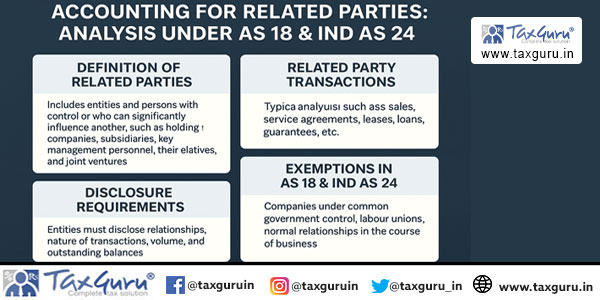

3. Definitions and Scope

AS 18 provides a relatively narrower definition of related parties, focusing on legal relationships, while Ind AS 24 adopts a broader, principle-based definition emphasizing substance over form. Ind AS 24 includes persons or close members of their families having control, joint control, or significant influence over the entity, and considers entities part of the same group or joint arrangements.

Key differences include:

– Coverage of relatives: Narrow in AS 18, broader in Ind AS 24

– Dual reporting: Not required in AS 18, mandatory in Ind AS 24.

– Post-employment benefit plans: Covered in Ind AS 24 only.

– Control assessment: Based on legal control in AS 18; includes de facto and joint control in Ind AS 24.

4. Recognition and Disclosure Requirements

Under AS 18, disclosures are required only where transactions have occurred. It includes relationship descriptions, nature of transactions, and outstanding balances. In contrast, Ind AS 24 mandates disclosure even without transactions, requiring additional details like terms, pricing mechanisms, and KMP compensation breakdown.

5. Real-Life Complexity: Illustration from Corporate Practice

Consider XYZ Ltd., where the promoter Mr. A holds 55% and influences ABC Pvt. Ltd. Transactions involving sales, consultancy fees, and leases with relatives illustrate broader coverage under Ind AS 24 compared to AS 18. Ind AS 24 requires disclosure based on substance, including terms and involvement of close family members.

6. Challenges in Practical Application

Practical challenges include:

– Identifying informal influence or control.

– Judging significant influence beyond shareholding.

– Assessing arms-length pricing.

– Managing non-disclosure risks, which can lead to audit qualifications and regulatory penalties.

7. Regulatory Linkages

RPTs are governed not only by accounting standards but also intersect with:

– Companies Act, 2013: Section 188.

– SEBI LODR Regulations: Material RPTs and audit committee approvals.

– Income Tax Act, 1961: Transfer pricing provisions for specified domestic transactions.

8. Concluding Thoughts

The shift from AS 18 to Ind AS 24 signifies India’s evolution towards a substance-driven disclosure framework. Chartered accountants must exercise professional judgment in mapping relationships, interpreting influence, and coordinating with internal teams to ensure comprehensive and compliant disclosures. Robust related party disclosures are central to financial transparency and governance.

*****

Author: Rahul Sharma – Qualification: FCA, MBA (Finance), LLB, CAIIB – ICAI Membership No: 402506

Author Bio