Summary: The issue concerns whether a trader can claim a refund of accumulated Input Tax Credit (ITC) under the inverted duty structure when GST rates on goods are reduced, such as from 28% to 18%. Under Section 54(3)(ii) of the CGST Act, refund of unutilized ITC is allowed when the tax rate on inputs exceeds that on output supplies, excluding nil-rated or exempted goods. “Inverted duty structure” is not defined in the GST Act but arises when such tax rate disparity occurs. Refund is limited to inputs and excludes input services and capital goods, as confirmed by the Supreme Court in Union of India v. VKC Footsteps India Pvt. Ltd. The CBIC, through Circular No. 135/05/2020-GST dated March 31, 2020, clarified that no refund is available where input and output supplies are the same but taxed differently over time due to rate revisions. This interpretation was reiterated in the FAQs following the 56th GST Council meeting. However, several High Courts—such as in Shivaco Associates v. Joint Commissioner of State Tax, Malabar Fuel Corporation v. Assistant Commissioner of Central Tax, and Indian Oil Corporation Ltd. v. Assistant Commissioner of Central Tax—have held that the circular is ultra vires the CGST Act. These rulings state that Section 54(3)(ii) does not restrict refunds to cases where input and output goods differ, and that administrative circulars cannot override statutory provisions. Therefore, while departmental authorities may deny refunds to traders citing the circular, judicial precedents affirm that refund under the inverted duty structure can be claimed by traders if the GST rate on inputs is higher than on outputs, provided the supplies are not nil-rated, exempt, or restricted under Notification No. 5/2017-Central Tax (Rate).

1. General Overview:

The topic of our discussion is ‘Whether a trader can claim refund of ITC under inverted duty structure in case the rates are reduced from 28% to 18%?’

Before, jumping straight to the conclusion, we need to have a deep understanding of the following:

i. What does the expression ‘Inverted Duty Structure’ mean in GST law and its evolution?

ii. Does the term ‘refund of inputs’ encompass refund of Input Services and Capital Goods as well?

iii. Meaning and Scope of the Expression ‘Trader’ in the Context of GST Law

iv. How has 56th GST Council Meeting resulted in creation of Inverted Duty Structure?

v. Detailed Analysis of Circular No. 135/05/2020-GST dated March 31, 2020 and the Related FAQs

vi. Judicial Pronouncements on Circular No. 135/05/2020-GST (Supra)

B. Inverted Duty Structure:

- Section 2 of the CGST Act, 2017 (hereinafter referred to as ‘CGST Act’) does not define the concept of Inverted Duty Structure.

Further, it is pertinent to note that the expression ‘Inverted Duty Structure’ has not been defined in Section 54 of CGST Act.

This naturally gives rise to an important question: what is the source of the expression “Inverted Duty Structure” within the framework of GST law?

- In this regard, a reference shall be made to Section 54(3)(ii) of the CGST Act, which is reproduced as below:

Section 54: Refund of tax

(3) Subject to the provisions of sub-section (10), a registered person may claim refund of any unutilised input tax credit at the end of any tax period:

(i) XXX

(ii) where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies), except supplies of goods or services or both as may be notified by the Government on the recommendations of the Council:

- Further, we would like to produce the provision of Section 18(4) of the CGST Act, as below:

‘(4) Where any registered person who has availed of input tax credit opts to pay tax under section 10 or, where the goods or services or both supplied by him become wholly exempt, he shall pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock and on capital goods, reduced by such percentage points as may be prescribed, on the day immediately preceding the date of exercising of such option or, as the case may be, the date of such exemption’

- Furthermore, the Central Board of Indirect Taxes and Customs (‘CBIC’), in exercise of the powers conferred under Section 54(3)(b) of the CGST Act, vide Notification No. 5/2017-Central Tax (Rate), dated 28 June 2017 (as amended), has specified the goods for which refund shall not be available on account of an Inverted Duty Structure.

It is pertinent to note that it is the first time that GST law uses the expression ‘Inverted Duty Structure.

- A combined reading of Section 54(b)(b) & Section 18(4) of the CGST Act, read along with Notification No. 5/2017 (supra), leads to the following conclusions:

i. Refund of Input Tax Credit shall be available in respect of inputs where the GST rate on inputs is higher than the GST rate on the outward supplies.

ii. However, no refund of inputs shall be available in the case of nil-rated or exempted supplies by virtue of Section 18(4) of the CGST Act.

iii. Further, refund of inputs shall not be available for goods specified vide Notification No. 5/2017(supra).

- Let’s break down the above into certain Practical Scenarios for better clarity:

Note: It must be noticed that in all the above scenarios it has been assumed that the GST Rate on Inward Supplies is higher than GST Rate on outward Supplies, which is trigger point for inverted duty structure.

| Inward supplies covered by NN 5/2017 | Outward Supplies covered by NN 5/2017 | Outward supplies are exempted supplies | Outward supplies are nil-rated supplies | Remarks |

| No | No | No | No | As the GST Rate on Inward Supplies is more than the GST Rate on outward Supplies.

Accordingly, refund shall be available. |

| Yes | No | No | No | As the GST Rate on Inward Supplies is more than the GST Rate on outward Supplies.

The fact that inward supplies are covered in notification is irrelevant. Accordingly, refund shall be available. |

| No | Yes | No | No | Even though the GST Rate on outward supplies is less than the GST Rate on Inward supplies, still no refund is available as the outward supplies are covered in NN 5/2017 |

| No | No | Yes | No | Outward Supplies are exempted under the GST.

Accordingly, refund shall not be available. |

| No | No | No | Yes | Outward supplies are nil-rate under GST.

Accordingly, refund shall not be available. |

C. Refund of accumulated Input Tax Credit on Input, Input Services and Capital Goods:

- In terms of Section 2(63) of the CGST Act, the ‘Input Tax Credit’ (hereinafter referred to as ‘ITC’) means the credit of input tax.

- Further, it must be noted that the ITC gets accumulated on account of input tax rate being higher than the output tax rates.

- Further, in terms of Section 2(59) of the CGST Act, ‘Input’ means any goods other than capital goods used or intended to be used by a supplier in the course or furtherance of business.

- Furthermore, in terms of Section 2(60) of the CGST Act, ‘Input Service’ means any service used or intended to be used by a supplier in the course or furtherance of business.

In terms of Section 2(19) of the CGST Act, the term ‘capital goods’ means goods, the value of which is capitalised in the books of account of the person claiming the input tax credit and which are used or intended to be used in the course or furtherance of business.

A pertinent question arises: whether refund of Input Tax Credit is available in respect of all inputs, input services, and capital goods?

- Section 54(3)(b) uses the expression ‘credit has accumulated on account of rate of tax on inputs’. It is pertinent to note that there is no mention of input services and capital goods aforesaid provision.

- Furthermore, in Union of India v. VKC Footsteps India Pvt. Ltd., Civil Appeal No. 4810 of 2021, the Hon’ble Supreme Court upheld the validity of Rule 89(5) of the CGST Rules, 2017.

Accordingly, it is a well-settled principle that no refund of Input Tax Credit shall be available in respect of input services.

- We would like to explain the above with the help of Scenario, as below:

| Scenario | Particulars | Remarks |

| 1. | X ltd manufacturer of medicine in pharma sector. It received inputs in form of chemical @ 18%.

Further, the output supply in form of medicine is taxed @ 5%. |

Input rate is higher than output rate.

Accordingly, refund of ITC shall be available. |

| 2. | Y Ltd, a BPO (call center), received the following services:

i. Renting of immovable property (commercial office lease): 18% GST ii. Telecom services – 18% GST iii. Security services – 18% GST Output services include provide the BPO services to domestic clients which is taxable @ 12 % GST. |

Input has been accumulated on account of input services rate being higher than output services rate.

VKC Footsteps (Supra)- No refund on Input Services Accordingly, No refund shall be available. |

| 3. | Z ltd is Hospital Diagnostic Centre. Hospital diagnostic centres provide taxable services. They are engaged in providing services to corporate clients

Recently, they have purchased an MRI Machine which is taxable @ 18%. Health check-up and diagnostic services to corporate clients under “health & wellness packages under GST @ 12%. |

MRI machines are capital goods which will be capitalized in the book of accounts.

Accordingly, No refund is then available. |

D. Meaning of ‘Trader’ in the GST Law:

- There is no definition of the term ‘Trader’ in the GST law, nor is there any reference to a similar expression anywhere in the statute.

- As per Rule 2(c) of the Central Excise Rules, 2002, the term ‘Dealer’ means a person who engages in the buying or selling of excisable goods for consideration and includes an importer who sells excisable goods.

- As per Section 2(b) of the Central Sales Tax Act, 1956, a ‘Dealer’ means any person who carries on, whether regularly or otherwise, the business of buying, selling, supplying, or distributing goods, directly or indirectly, for cash, deferred payment, commission, remuneration, or other valuable consideration.

- As per Section 2(J) of the Delhi VAT Act, 2004, a ‘Dealer’ means any person who carries on the business of buying, selling, supplying, or distributing goods, directly or indirectly, whether for cash, deferred payment, commission, remuneration, or other valuable consideration.

- The terms ‘dealer’ and ‘trader’ are closely related and, in general practice, have often been used interchangeably.

From the above definitions of ‘dealer’ under the earlier indirect tax regime, the term ‘trader’ can be understood to mean a person who is engaged in the business of buying, selling, supplying, or distributing goods without engaging in any manufacturing activity.

It is pertinent to note that, for the sake of clarity, traders mainly deal in goods where the GST rates on inputs and outputs are generally the same.

E. 56th GST Council Meeting- Rate Rationalization:

- Pursuant to the 56th GST Council meeting, the Central Government has reduced the GST rate from 12% to 5%, or even to nil in certain cases. Further, in most cases, the GST rate has been reduced from 28% to 18%.

- The new GST Rates can be summarized as follows:

- The reduction in GST rates effective from 22 September 2025 is likely to create a market slowdown. Until that date, customers may defer purchases, while a significant quantity of stock remains with dealers and traders, which has already been taxed at 28%.

Similarly, manufacturers are likely to hold substantial inventory of parts, also taxed at 28%, creating additional financial and logistical challenges.

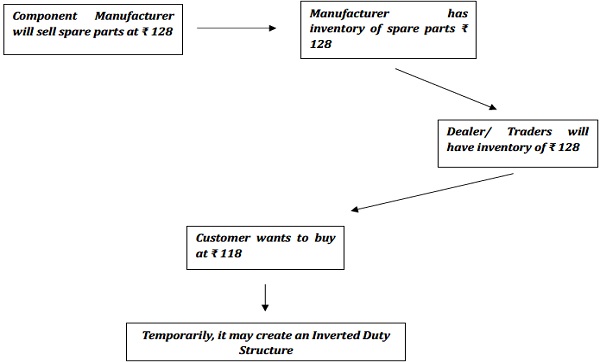

For illustration, consider the following scenario:

i. The GST rate on parts has been reduced from 28% to 18%.

ii. These parts are used by OEMs in the manufacture of small cars. Manufacturers are likely to hold substantial stock of spare parts taxed at 28% by component manufacturers.

iii. The GST rate on small cars has been reduced from 28% to 18%.

iv. Similarly, dealers and traders hold significant stock of small cars, which has been taxed at 28%.

Importantly, owing to the rate reduction announcement, customers are likely to defer purchases in anticipation of a sharp price reduction after 22 September 2025.

It is pertinent to conclude the discussion with the observation that, even in the case of traders or dealers where no manufacturing process is involved, a temporary situation of Inverted Duty Structure may arise.

This may lead to the accumulation of Input Tax Credit, depending on the margins of traders and dealers.

F. Circular and FAQs References on Inverted Duty Structure:

- The CBIC has issued a Circular 135/05/2020 – GST dated March 31, 2020, the relevant extract of the circular is as follows:

Refund of accumulated input tax credit (ITC) on account of reduction in GST Rate

‘3.1 It has been brought to the notice of the Board that some of the applicants are seeking refund of unutilized ITC on account of inverted duty structure where the inversion is due to change in the GST rate on the same goods. This can be explained through an illustration. An applicant trading in goods has purchased, say goods “X” attracting 18% GST. However, subsequently, the rate of GST on “X” has been reduced to, say 12%. It is being claimed that accumulation of ITC in such a case is also covered as accumulation on account of inverted duty structure and such applicants have sought refund of accumulated ITC under clause (ii) of sub-section (3) of section 54 of the CGST Act.

3.2 It may be noted that refund of accumulated ITC in terms clause (ii) of sub-section (3) of section 54 of the CGST Act is available where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies. It is noteworthy that, the input and output being the same in such cases, though attracting different tax rates at different points in time, do not get covered under the provisions of clause (ii) of sub-section (3) of section 54 of the CGST Act. It is hereby clarified that refund of accumulated ITC under clause (ii) of sub-section (3) of section 54 of the CGST Act would not be applicable in cases where the input and the output supplies are the same’.

The circular precludes the refund in scenarios where, due to a sudden change in GST rates, the GST rates on inputs and outputs are the same, but Input Tax Credit accumulates on account of inventory holding arising from changes in consumer purchasing behaviour.

- Furthermore, in the recent FAQs issued by the CBIC with respect to the 56th GST Council Meeting and relevant extract of the FAQs with respect to our matter is as follows:

‘10. Will I be allowed to take refund of accumulated credit arising out of inverted duty structure for supplies effected upto the date of effect of revised rate as notified?

The said issue has been clarified vide Circular 135/05/2020-GST dated 31.03.2020 (as amended), which states that refund of accumulated ITC in terms of clause (ii) of first proviso to section 54(3) of the CGST Act, is available where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies.

However, the input and output being the same in such cases, though attracting different tax rates at different points in time, do not get covered under the provisions of clause (ii) of the first proviso to sub-section.’

The FAQs issued continue to maintain the same position regarding the availability of Input Tax Credit refunds to traders.

G. Legality of Circular 135/05/2020-GST Dated March 31, 2020:

- Section 54(3)(ii) of the CGST Act uses the expression ‘where the rate of tax on inputs is higher than the rate of tax on outward supply’. The statutory text does not qualify that such rate differential must arise only on account of the inherent nature of the business, nor does it exclude cases where the inversion results from a subsequent change in GST rates by the Government.

When the language of a taxing statute is plain, it must be strictly construed, and no words or limitations can be read into it.

However, Circular No. 135/05/2020-GST seeks to restrict refund under the inverted duty structure only to manufacturers, and that too where the inversion is attributable to the nature of business. Such a restriction, being extraneous to the statute, appears to travel beyond the scope of Section 54(3)(ii) of the CGST Act.

- Similar facts were discussed in case of Shivaco Associates Vs Joint Commissioner of State Tax, Directorate of Commercial Taxes, P.A. No. 54 of 2022, decided on 11-3-2022, wherein the petitioner sold certain goods at GST Rate of 18 percent and sells the goods at GST rate of 5 percent. But, subsequent to the Notification, the GST rate on inputs were also reduced to 5 percent. This led to a situation of inverted duty structure for the Petitioner and accordingly, applied for refund.

The refund application by the Petitioner was rejected by the Respondent on account of views expressed in circular 135/05/2020-GST, dated March 31, 2025.

The Hon’ble High Court (‘HC’) held that Act does not restrict refund only in respect of supplies which are different at input and output stage, accordingly, the said Circular is not applicable and bad in law. The relevant extract of the judgement is as follows:

‘26. In the present case, the Act does not mention about non-granting of the benefit of accumulated Input Tax Credit where the input and output supplies are the same. The circular is trying to restrict the refund to a particular set of supplies. The circular is trying to create a class inside the class, which is impermissible. According to the Act, refund is permissible in respect of all classes where the input tax is higher than the output tax. By way of the circular, the Board is curtailing the said benefit and making refund permissible only if the input and output supplies are different. The same amounts to overreaching the provisions as laid down in the Act.’

- The Similar facts were again discussed in case of Malabar Fuel Corporation Vs Assistant Commissioner, Central Tax and Central Excise, Kannur, P. (C) Nos. 26112, 20511 and 36699 of 2023, decided on 11-1-2024, wherein the Hon’ble HC held that refund of accumulated input tax credit was to be allowed under Section 54 of the CGST Act where credit accumulated on account of rate on inputs was higher than rate of tax on output supplies. Therefore, Act does not restrict refund only in respect of supplies which are different at input and output stage. However, by way of above circular, Board was curtailing said benefit and making refund only if input and output supplies are different, which amounted to overreaching provisions as laid down in Act. The relevant extract of the judgement is as follows:

‘10. In almost similar facts and circumstances of these cases, the aforesaid Circular has been considered by the aforesaid four High Courts in the following cases:

All the four High Courts have held that the condition laid down in clause 3.2 of the Circular, which denies refund of credit accumulated to a dealer as a result of higher tax on inputs than the output supplies, when the input and output supplies are one and the same, would have to be ignored.

-

- Again, the similar facts were discussed in case of Indian Oil Corporation Ltd. Vs Assistant Commissioner of Central Tax, Writ Petition No. 14414 of 2024 (T-RES), decided on 20-8-2024, wherein the Hon’ble HC held that Section 54(3)(ii) doesn’t restrict refund to cases where rate on main input is higher than rate on principal output; refund permissible where ITC accumulated due to any inputs attracting higher rate than output Circular No. 135/05/2020-GST to contrary extent has no application, accordingly, impugned orders quashed. The relevant extract of the judgement is as follows:

‘15. As held in the aforesaid judgments by the Delhi High Court and other High Courts, Section 54(3)(ii) of the CGST Act does not proscribe/forbid the grant of refund where the input and the output are the same and that clause (ii) of proviso to subsection (3) of Section 54 of the CGST Act does not contemplate comparing rate of tax on the principal input with the rate of tax chargeable on the principal output supply; further, there is neither any reason nor any scope to further confine the refund of unutilised ITC only to cases where the rate on main input is higher than the rate of tax on the principal output.

- In case of Eveready Spinning Mills Pvt. Ltd. Vs Assistant Commissioner, Central Gst & Central Excise Dindigul, W.P. (MD) No. 10033 of 2024 and W.M.P. (MD) No. 9066 of 2024, decided on 16-7-2024, Wherein the refund application of petitioner was dismissed on similar grounds and Hon’ble HC declares that Circular (supra) as ultra vires to the provision of the Section 54(3)(ii) of the CGST Act.

- Apart from the above, there are numerous High Court judgements that clearly state that Paragraph 3.2 of the Circular (supra) is ultra vires the GST Act and invalid in law.

Further, it appears that the circular has sought to create an exclusive category and to interpret the law in a restrictive manner.

H. Final Conclusion: Whether the refund of accumulated ITC shall be available to the Traders:

- The expression ‘Inverted Duty Structure’ was first used in the Notification No. 5/2017 (Supra). The concept evolves from Section 54(3)(ii) of the CGST Act which simply explains that refund of credit shall be available where the rate of ‘inputs’ being more than the rate of outputs.

- The expression ‘inputs’ used in the statute signifies that no refund shall be available for input services, which is further affirmed by the Hon’ble SC in VKC Footsteps.

No refund is further possible in case of capitals goods.

- This means that under inverted duty structure refund is available only in case ITC on account of accumulated ‘inputs’ provided that outward supplies should not be covered by Notification 5/2017 (Supra).

Further, the outward supplies should not be any nil-rate or exempted supplies.

- In case the above conditions are satisfied, an applicant including a Trader can apply for refund under Inverted Duty Structure.

Department may not directly grant the refund in view of Circular 135/05/2020-GST which was further affirmed in FAQs issued by the Council.

But, In such cases, an Applicant can approach directly approach to the Writ courts challenging the legality of the Circular (Supra).

Author Bio