USE OF COST ACCOUNTING CONCEPTS, TECHNIQUES AND METHODS IN INTERNAL AUDIT

Integrating Marginal Costing, Standard Costing, Variance Analysis, Cost Control & Reduction, and Marketing Strategy Evaluation into Risk-Based Internal Audit

Executive Summary

This article analyses how cost accounting techniques empower internal audit to evolve from a compliance-centric function to a strategic value-adding partner. It explains core cost accounting concepts—marginal costing, standard costing, variance analysis, activity-based costing, target costing— and demonstrates how internal auditors can apply these techniques to identify operational inefficiencies, prevent fraud, and advise management on pricing, product-mix and cost-reduction initiatives. The document includes corporate case studies, practical audit procedures, numerical illustrations and sample tables/charts to aid auditors and audit committees. Key recommendations include embedding cost analytics within Risk-Based Internal Audit (RBIA), developing continuous monitoring dashboards for variances, and aligning audit procedures with strategic profit drivers to enable timely governance action.

Introduction

Cost accounting provides a systematic framework to collect, measure, analyse and report cost information. For internal audit, this information is indispensable—not merely for verifying compliance with budgets and controls—but for evaluating management decisions concerning pricing, product viability, resource allocation and strategic initiatives. This article assumes a professional readership of qualified chartered accountants and internal auditors, and aims to provide practical guidance, audit procedures and illustrative examples on deploying cost accounting techniques within internal audit engagements.

Marginal Costing and Its Use in Internal Audit

Marginal costing (also referred to as variable costing) segregates costs into variable and fixed components. Contribution (Sales – Variable Costs) becomes the primary decision metric. Internal auditors can use marginal costing to evaluate short-term decision making—such as accepting special orders, make-or-buy decisions, product discontinuation, and pricing during excess capacity. Key internal audit procedures using marginal costing include:

1. Verification of variable cost classification: Confirm that costs classified as variable move in direct proportion to output using statistical testing and historical analysis.

2. Contribution analysis: Reconstruct contribution per product or SKU and test assumptions used in management reports.

3. Sensitivity and break-even analysis: Verify break-even calculations and stress-test scenarios used in board papers.

Numerical Illustration (Marginal Costing):

Consider Product A sold at ₹200 per unit. Variable cost per unit ₹120. Fixed costs (plant-level) ₹6,00,000 per annum. Annual sales volume 20,000 units.

Contribution per unit = ₹80. Total contribution = ₹80 × 20,000 = ₹16,00,000. Break-even units = Fixed Costs ÷ Contribution per unit = 600,000 ÷ 80 = 7,500 units.

Audit Insight: If management proposes a promotional discount lowering price to ₹180 for a limited period to increase market share, internal auditors must test whether the marginal contribution at the discounted price (₹60) still contributes meaningfully to fixed costs and whether the increased volume assumption is realistic.

Standard Costing, Budgeting and Variance Analysis

Standard costing establishes predetermined unit costs for materials, labour and overheads. Comparison of actuals against standards yields variances (material, labour, overhead) which flag areas needing investigation. Variance analysis serves as a control and an investigative instrument to identify inefficiency, waste, pricing errors, and potential fraud.

Common variances and audit focus:

– Material Price Variance (MPV): Investigate procurement procedures, supplier contracts and invoice authenticity.

– Material Usage / Quantity Variance (MUV): Examine production records, bill of materials (BOM), wastage reports and quality control exceptions.

– Labour Rate and Efficiency Variance: Check payroll, timekeeping systems, overtime approvals and skill-mix.

– Overhead Variances: Ensure correct overhead absorption bases and investigate significant fixed overhead volume variances.

Numerical Illustration (Standard Costing & Variance Analysis):

Standard: 2 kg of raw material per unit at ₹50/kg. Standard cost per unit for material = ₹100.

Actual: 10,200 kg purchased at total cost ₹5,31,000 for 5,000 units produced.

Actual cost per kg = 5,31,000 ÷ 10,200 = ₹52.06.

Material Price Variance = (Actual price − Standard price) × Actual quantity = (52.06 − 50) × 10,200 = ₹20,712 (Adverse).

Standard quantity for 5,000 units = 5,000 × 2 = 10,000 kg. Material Usage Variance = (Actual quantity − Standard quantity) ×

Standard price = (10,200 − 10,000) × 50 = ₹10,000 (Adverse).

Audit Procedures: Verify supplier invoices, reconcile purchase ledger with receiving reports, observe physical stock counts and perform root-cause analysis for adverse variances.

Activity‑Based Costing (ABC) and Driver Analysis

Traditional absorption costing may distort product costs when overheads are significant and products consume resources disproportionately. Activity‑Based Costing assigns overheads to activities and then to products based on cost drivers. For internal audit, ABC offers:

– More accurate product profitability analysis.

– Insights into non-value-adding activities for cost reduction.

– Better basis to evaluate product pricing, make-or-buy and outsourcing decisions.

Audit Use-Cases: Test the selection of cost pools, validate driver measures, and test data integrity for activity volumes (machine hours, setups, inspections). Confirm that allocation logic is consistent with observed operations.

Cost Control and Cost Reduction: Audit Perspective

Cost control is the process of monitoring and ensuring costs remain within approved budgets. Cost reduction aims at permanently lowering costs while preserving product/service quality. Internal audit distinguishes between one‑time savings and sustainable reductions.

Audit techniques:

– Trend analysis and KPI monitoring for raw material yield, OEE (Overall Equipment Effectiveness), scrap rates.

– Process mining and controls review in procurement and inventory systems to detect leakages.

– Review of contracts (logistics, utilities) to identify renegotiation opportunities and automatic price escalation clauses.

Case Example: Logistics Reengineering in an FMCG Company

An FMCG company reduced distribution cost by 8% by moving to a hub-and-spoke model, renegotiating freight slabs, and consolidating dispatches. Internal audit corroborated the reported savings by sampling freight invoices and matching them to shipment manifests.

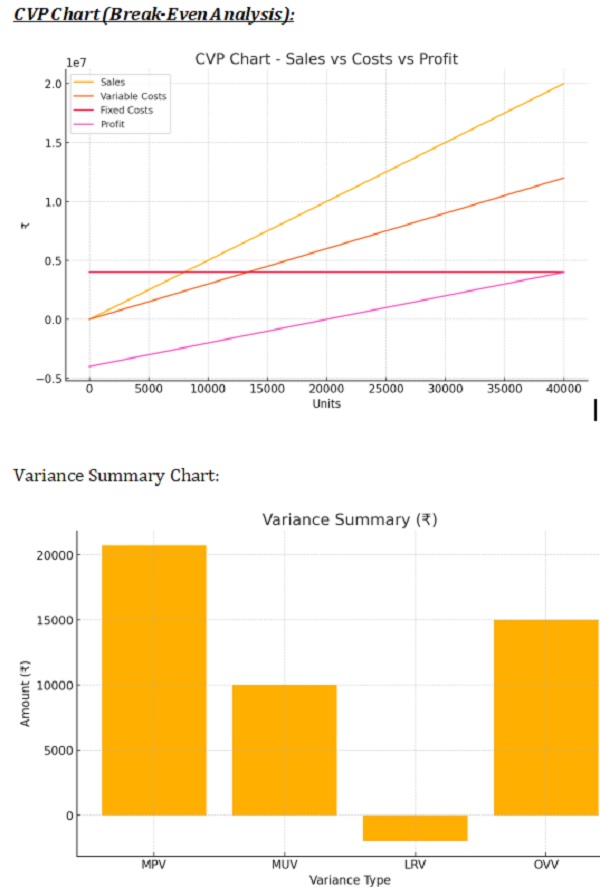

Cost‑Volume‑Profit (CVP) Analysis and Break‑Even Evaluation

CVP links cost behaviour with sales volume to study profit sensitivity. Internal auditors validate the assumptions behind CVP models—price elasticity, variable cost proportion, and fixed cost classification.

Practical audit actions:

– Recalculate break-even points for key products and run scenario tests.

– Validate assumptions used in management’s ‘what‑if’ analyses in board presentations.

– Where revenue recognition timing affects contribution, verify cut‑off procedures.

Numerical Example (CVP):

Company sells Product X at ₹500; variable cost ₹300; contribution ₹200. Fixed costs ₹40,00,000.

Break-even units = 40,00,000 ÷ 200 = 20,000 units. At proposed price discount to ₹460 (contribution ₹160), break‑even becomes 25,000 units. Internal audit should test sales forecasts supporting such pricing actions.

Marketing Strategy, Pricing and Audit Examination

Marketing strategies—promotions, bundle pricing, channel discounts—impact contribution and product profitability. Internal audit must extend cost analytics to review marketing ROI and ensure that trade discounts and promotional allowances are properly authorised and reconciled.

Audit points:

– Reconcile trade discount provisions and promotional accruals with supporting campaign data.

– Assess margin erosion from channel incentives and unauthorised discounting by field sales.

– Verify that customer segmentation and price discrimination are based on robust contribution analysis.

Case Study: Retail Chain Promotion Audit

A retail chain’s aggressive promotions led to same-store-sales growth but shrinking gross margins. Internal audit analysed SKU‑level contribution before and after promotions and discovered that deep-discount promotions on high-volume but low-margin SKUs reduced overall contribution. Audit recommended narrowing promotions to higher contribution items and using loyalty-linked targeted discounts.

Relevance to Banking and Service Organisations

Although traditional cost accounting is manufacturing-centric, banks and service organisations benefit from cost analysis through unit cost of service, branch profitability, and activity-based costing for support functions. Internal audit in a bank context (for example, UCO Bank branches) should:

– Analyse cost-to-income ratios per branch and per product (retail loans, deposits, trade services).

– Use ABC to allocate IT and treasury overheads to business units based on drivers like transaction counts and complexity.

– Assess pricing of fee-based services using contribution analysis and competitor benchmarking.

Numerical Illustration (Bank Branch Profitability):

Branch A: Interest income ₹12,00,000; Fee income ₹1,50,000; Direct expenses ₹3,50,000; Allocated overheads ₹4,00,000. Net contribution = (12,00,000 + 1,50,000) − (3,50,000 + 4,00,000) = ₹6,00,000.

Integrating Cost Accounting into Risk‑Based Internal Audit (RBIA)

RBIA prioritises audits based on risk exposure and materiality. Cost analytics enhance RBIA by quantifying financial exposure from cost variances and margin erosion. Steps to integrate:

1. Identify high-impact cost drivers—raw material prices, labour mix, logistics.

2. Map drivers to processes and controls; determine control objectives and key risk indicators (KRIs).

3. Develop continuous monitoring rules and exception reporting for significant variances.

Sample Audit Programme Items:

– Test accuracy of standard cost rates and update cycle for standards.

– Evaluate the process for costing new product introductions and pilot production.

– Review the mechanism for approving promotional pricing and estimating incremental volumes.

Cost Analytics as a Fraud Detection Tool

Aberrant variances, unexplained cost spikes, or unusually consistent rounding patterns may indicate manipulation or collusion. Examples of red flags:

– Repeated adverse material usage variances concentrated in a particular shift or plant.

– Unusual labour efficiency variances coinciding with overtime approvals.

– Round-number invoice totals or consistent price increases from a single vendor without competitive bidding.

Audit response: Perform detailed transactional testing, data analytics (Benford analysis where suitable), and forensic interviews. Coordinate with legal and forensic teams when necessary.

Corporate Case Studies and Real‑Life Examples

Case Study 1: Steel Manufacturer – Standard Costing Investigation

A large steel manufacturer recorded an adverse material usage variance of 5% in hot-rolled coil production. Internal audit verified BOMs, inspected supplier quality certificates and discovered that a 3% portion of scrap was being misclassified as finished goods due to a system mapping issue. Corrective actions included system patching, supplier quality monitoring and a strengthened receiving inspection.

Case Study 2: Textile Mill – Marginal Costing for Product Mix

A textile mill produced two variants: Basic Fabric (low margin, high volume) and Premium Fabric (high margin, lower volume). Internal audit recalculated contribution margins and advised shifting limited dyeing capacity towards premium fabric during peak demand months. This raised overall plant contribution by 6% without additional fixed costs.

Case Study 3: FMCG Distribution Optimization

An FMCG company used internal audit to validate management’s claim of logistics savings after distribution redesign. Audit performed sample-based verification of freight invoices and labour records, and confirmed sustainable savings of 7.8% annually.

Practical Internal Audit Procedures & Checklists

Below is a consolidated checklist audit teams may adapt:

– Verify classification of costs (variable/fixed, direct/indirect).

– Recompute standard rates and perform material/labour/overhead variance reconciliation.

– Test integrity of cost allocation bases and ABC driver data.

– Reconcile production records with inventory movement and P&L consumption.

– Validate pricing decisions with contribution analysis and CVP scenarios.

– Sample test promotions, trade discounts and provisioning for promotional liabilities.

– Review contract terms for cost escalation and unilateral price changes.

– Evaluate KPI design and thresholds for continuous monitoring.

Tables and Charts

This document provides numerical tables and illustrative charts: a standard costing variance table, a CVP break-even chart and a cost reduction trend chart. These visual aids support audit findings and are recommended for inclusion in audit reports to the Audit Committee.

Conclusion and Recommendations

Cost accounting techniques substantially increase the effectiveness of internal audit. By enabling auditors to quantify inefficiency, test management assertions and provide decision support, cost analytics transform audit into a strategic partner. Key recommendations:

1. Embed cost analytics in RBIA with automated variance thresholds.

2. Train audit staff in cost accounting techniques and data analytics.

3. Use ABC selectively for complex overhead structures.

4. Collaborate with finance and operations for periodic standard updates.

5. Present audit findings with clear contribution, ROI and implementation timelines for remedial actions.

For banks and service organisations, adapt the same principles using service unit costing and activity drivers relevant to transactions and customer touchpoints.

References & Further Reading

1. Horngren, C.T., Datar, S.M., and Rajan, M.V., ‘Cost Accounting: A Managerial Emphasis’.

2. IIA Position Papers on Risk‑Based Internal Auditing and Continuous Monitoring.

3. ICAI Guidance Notes and Standards for Internal Audit in Banks and Financial Institutions.

Detailed Expansion: In-depth analysis of application, controls and audit evidence.

1.On Marginal Costing—Expanded: When assessing marginal costing assertions, auditors should obtain a representative sample of months covering peak and trough production, re-perform variable cost regressions against output levels to confirm variable behaviour, and compare purchasing price movement to commodity indices. Consider seasonal raw material contracts and hedging conclusions when evaluating variable cost exposures.

2. On Standard Costing—Expanded: The validity of standards depends on their governance—documented approval, periodic review and linkage to engineering BOMs and time & motion studies. Auditors must test the standard-setting process, confirm sample-signoffs and review board minutes for material changes.

3. On ABC and Cost Drivers—Expanded: For ABC projects, test mapping rules from transactions to activities; validate source systems (MES, ERP, T&A) and sample driver rates. Assess the stability of drivers and quantify allocation distortions by comparing ABC-derived unit costs to historical absorption costs.

4. On Fraud Detection—Expanded: Use data analytics to profile suppliers and labour patterns. Implement Benford tests on invoice amounts and sample vendor master changes to detect ghost vendors. Cross-reference procurement approvals with vendor master creation logs for segregation of duties breaches.

5. On Marketing & Pricing—Expanded: Recreate promotional ROI calculations, discount elasticities and channel profitability using SKU-level contribution. Insist on campaign documented hypotheses and post-campaign measurement. For trade schemes with intermediaries, confirm that accruals for promotional liabilities reconcile to subsequent claim settlements.

6. On Bank Branch Costing—Expanded: Allocate IT and HR overheads using ABC drivers such as transactions processed, active accounts, or teller transactions. Test the driver volumes and reconcile to system logs.

Standard Costing – Variance Summary (Illustrative)

| Particulars | Standard Qty/Rate | Actual Qty/Rate | Variance (₹) | Nature |

| Material Price Variance | ₹50/kg | ₹52.06/kg | ₹20,712 | Adverse |

| Material Usage Variance | 10,000 kg | 10,200 kg | ₹10,000 | Adverse |

| Labour Rate Variance | ₹200/hr | ₹195/hr | ₹-2,000 | Favourable |

| Overhead Volume Variance | – | – | ₹15,000 | Adverse |

CVP Illustration – Break-Even Calculation

| Item | Amount (₹) | Units | Remarks |

| Selling Price per unit | 500 | – | |

| Variable Cost per unit | 300 | – | |

| Contribution per unit | 200 | – | |

| Fixed Costs | 4,000,000 | 20,000 | Break-even units |

Illustrative Charts

CVP Chart (Break‑Even Analysis):

Cost Reduction Trend Chart:

Cost Reduction Trend Chart:

Additional Corporate Case Studies (Sector-Specific)

Additional Corporate Case Studies (Sector-Specific)

Banking Sector Case Study – Loan Processing Cost Analysis

In a mid-sized Indian bank, internal audit applied Activity-Based Costing (ABC) to loan processing. Audit discovered that 40% of back-office costs were consumed by small-ticket personal loans, while only 15% of contribution was generated from this segment. Audit recommended migrating small-ticket loans to digital platforms to reduce manual interventions. The bank implemented straight-through processing (STP), reducing processing cost per loan by 22% within a year.

Textile Sector Case Study – Standard Costing and Labour Efficiency

A large textile mill experienced consistent adverse labour efficiency variances in its dyeing department. Internal audit traced the issue to excessive machine downtime due to preventive maintenance schedules not aligned with production cycles. By recommending rescheduling of maintenance during off-peak shifts, the mill reduced downtime by 15% and improved overall labour efficiency. Audit validated the savings by comparing machine-hour utilization reports pre- and post-change.

FMCG Sector Case Study – Marketing Strategy and Contribution Analysis

A leading FMCG brand launched an aggressive discount campaign to counter competition. Internal audit analysed SKU-level profitability using marginal costing and found that flagship products’ contribution margins were diluted below breakeven. Audit advised narrowing discounts to secondary SKUs and focusing on value packs instead. Within two quarters, contribution margins improved by 9% while retaining competitive market positioning.

Author Bio