Case Law Details

Milani Swanirbhar Gosthi Vs ITO (ITAT Kolkata)

ITAT Kolkata Quashes Assessment: Invalid 143(2) Notice & NFAC Lacked Jurisdiction; Two Fatal Defects: Tribunal Rules Scrutiny Notice Invalid & NFAC Had No Power Pre-2022; Milani Swanirbhar Gosthi Vs ITO – ITAT Kolkata Strikes Down Assessment for Legal Defects; Assessment Void: Invalid Scrutiny Notice & NFAC Jurisdiction Missing, Rules ITAT Kolkata; ITAT Kolkata: CBDT Instructions Binding – Defective Notice & NFAC’s Lack of Authority Quash Assessment

Kolkata Tribunal quashed the entire assessment proceedings on two crucial grounds—(i) invalid notice issued u/s 143(2) in violation of CBDT Instruction, & (ii) absence of jurisdiction with NFAC to issue notice u/s 142(1) prior to 30.03.2022.

Facts

Assessee, a society, filed return on 15.10.2018 declaring income of ₹19.96 lakh. Case was selected for scrutiny & assessment framed u/s 143(3) on 18.03.2021. On appeal, CIT(A) NFAC dismissed assessee’s case ex-parte. Before Tribunal, assessee raised legal grounds challenging the validity of notices issued u/s 143(2) & 142(1).

Invalidity of 143(2) Notice

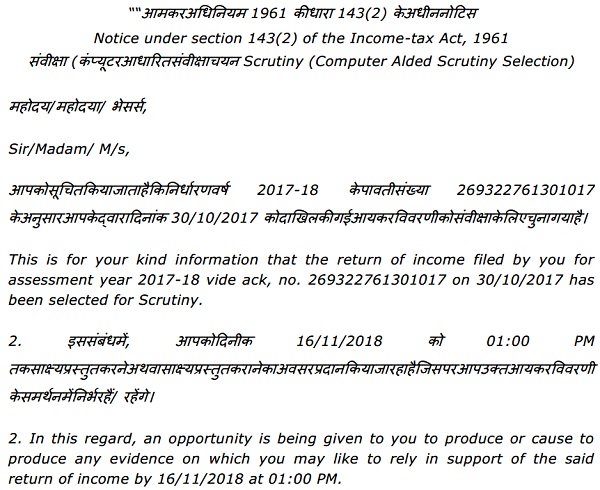

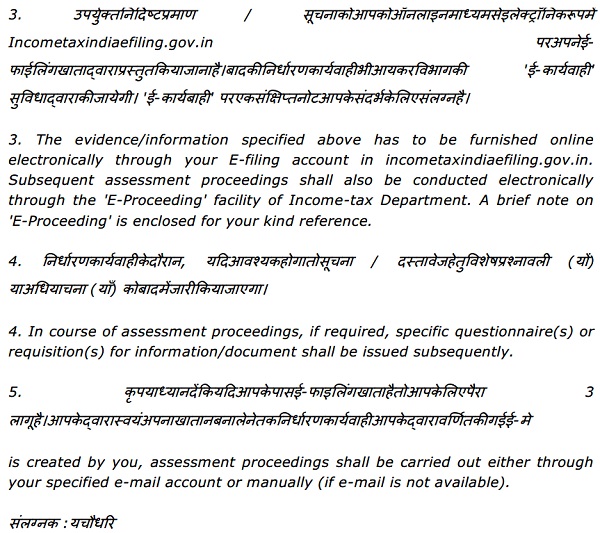

Assessee contended that notice dated 22.09.2019 was not in conformity with CBDT Instruction No. 225/157/2017/ITA-II dated 23.06.2017, since it merely mentioned “Computer Aided Scrutiny Selection” without specifying whether scrutiny was “limited” or “complete.” Tribunal, relying on coordinate bench decisions in Tapas Kumar Das vs. ITO (ITA 1660/KOL/2024, AY 2017-18) & Shib Nath Ghosh vs. ITO (ITA 1812/KOL/2024, AY 2018-19), held that such defective notice is invalid. Since CBDT instructions issued u/s 119 are binding on the Department (relying on SC in UCO Bank), violation rendered the entire assessment void ab initio.

Lack of Jurisdiction of NFAC u/s 142(1)

Assessee further argued that notice u/s 142(1) dated 13.01.2021 issued by NFAC was beyond jurisdiction since the statutory framework for faceless enquiry under s.142B was notified only on 30.03.2022 (Notification No. 19/2022). Prior to this date, NFAC had no authority to issue such notice. Tribunal accepted this contention, holding that assessment framed by NFAC was without jurisdiction & hence invalid.

Tribunal’s Decision

Notice u/s 143(2) dated 22.09.2019 not being in prescribed format was invalid. Consequently, the assessment order dated 18.03.2021 stood quashed. Additionally, even the notice u/s 142(1) issued by NFAC was without jurisdiction, as statutory backing under s.142B & s.144B came only from 30.03.2022 onwards. Appeal of assessee allowed in full.

This ruling reiterates that CBDT’s procedural instructions are binding, & any deviation renders assessment invalid. Further, NFAC had no jurisdiction to issue notices u/s 142(1) before 30.03.2022, making such assessments void. The decision strengthens the position of taxpayers facing scrutiny notices not in prescribed format or issued by an authority lacking jurisdiction.

FULL TEXT OF THE ORDER OF ITAT KOLKATA

This is an appeal preferred by the assessee against the order of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Ld. CIT (A)”] dated 16.01.2025for the AY 2018-19.

2. The issue raised in ground no.1 is against the invalid notice issued u/s 143(2) of the Act dated 22.09.2019, in violation of CBDT instruction no. F. No. 225/157/2017/ITA-II Dated 23-06-2017.

3. The facts in brief are that the assessee filed the return of income on 15.10.2018, declaring total income of ₹19,96,730/-. The case of the assessee was selected for complete scrutiny and accordingly, notice u/s 143(2) and 142(1) of the Act, along with questionnaire were issued and served upon the assessee. Finally, the assessment was framed vide order dated 18.03.2021, passed u/s 143(3), read with section 143(3A) and 143(3B) of the Act.

4. In the appellate proceedings, the appeal was decided ex-parte in limine when the assessee failed to comply with the notices issued by the appellate authority.

5. The assessee has challenged the very basis of the assessment on the ground that the statutory notices u/s 143(2) of the Act dated 22.09.2019, was not in conformity with CBDT instruction no. F. No. 225/157/2017/ITA-II Dated 23-06-2017 and therefore, the entire proceedings, including the assessment order framed is nullity and bad in the eyes of law. The ld. AR in defense of his arguments relied on the decision of Tapas Kumar Das Vs. ITO in ITA No. 1660/KOL/2024 vide order dated 11.03.2025 for A.Y. 2017-18, wherein similar issue has been decided in favour of the assessee. The ld. AR therefore prayed that the additional ground raised by the assessee may kindly be allowed

6. The ld. DR on the other hand submitted that this is a computer-generated notice and the non-mentioning of the fact of either limited or complete scrutiny or compulsory manual scrutiny would not render the issuance of notice u/s 143(2) of the Act as invalid. Therefore, ground raised by the assessee may kindly be dismissed.

7. After hearing the rival contentions and perusing the materials available on record, we find that undisputedly the notice issued u/s 143(2) of the Act dated 22.09.2019, specified only computer aided scrutiny selection which neither mentioned it either to be a limited or a complete scrutiny nor compulsory manual scrutiny. Thus, the said notice has been issued in violation of the instruction issued by CBDT as noted above. In our opinion, the revenue authorities have to follow the instruction issued by CBDT and violation thereto would certainly render the notice as invalid with the result all the consequential proceedings would also be invalid. The case of the assessee find support from the decision of the co-ordinate Bench in the case of Tapas Kumar Das Vs. ITO (supra), wherein a similar issue has been decided in favour of the assessee. The operative part of the same is extracted below: –

“After hearing the rival contentions and perusing the materials available on record, we find that particularly the notice was issued u/s 143(2) of the Act, a copy of which is available at page no. 25 of the Paper Book. We note that the said notice has not been issued in consonance with the CBDT Instruction F No. 225/157/2017/ITA-II Dated 23.06.2017. The said notice is extracted below for the sake of ready reference:-

Enclosure as above

7. In our opinion, the notice issued u/s 143(2) of the Act which is not in the prescribed format as provided under the Act is an invalid notice and accordingly, all the subsequent proceedings thereto would be invalid and void ab initio. The case of the assessee find support from the decision of Shib Nath Ghosh Vs. ITO in ITA No. 1812/KOL/2024 for A.Y. 2018-19 vide order dated 29.11.2024, wherein the coordinate Bench has held as under:-

“10. After hearing both the sides and the materials available on record, we find that the notice issued u/s 143(2) dated 9th August, 2017 was not in any of the formats as provided in the CBDT instruction F.No.225/157/2017/ITA-II dated 23.06.2017. We have examined the notice, copy of which is available at page no.1 of the Paper Book and find that the same is not as per the format of CBDT Instruction F.No. 225/157/2017/ITA-II dated 23.06.2017 as stated above. In our opinion, the instruction issued by the CBDT are mandatory and binding on the Income tax authorities failing which the proceedings would be rendered as invalid. Hon’ble Apex Court in case of UCO Bank (supra) held that the circular issued by CBDT in exercise of its statutory powers u/s 119 of the Act, are binding on the authorities. The Hon’ble Apex court held as under:-

“The Central Board of Direct Taxes under section 119 of the Income-tax Act, 1961, has power, inter alia, to tone down the rigour of the law and ensure a fair enforcement of its provisions, by issuing circulars in exercise of its statutory powers under section 119 of the Act which are binding on the authorities in the administration of the Act. Under section 119(2)(a), however, the circulars as contemplated therein cannot be adverse to the assessee. The power is given for the purpose of just, proper and efficient management of the work of assessment and in public interest. It is a beneficial power given to the Board for proper administration of fiscal law so that undue hardship may not be caused to the assessee and the fiscal laws may be correctly applied. Hard cases Which can be properly categorized as belonging to a class, can thus be given the benefit of relaxation of law by Issuing circulars binding on the taxing authorities.

In order to aid proper determination of the income of money lenders and banks, the Central Board of Direct Taxes issued a circular dated October 6, 1952, providing that where interest accruing on doubtful debts is credited to a suspense account, It need not be included in the assessee’s taxable income, provided the Income-tax Officer is satisfied that recovery is practically improbable. Twenty-six years later, on June 20, 1978, in view of the judgment of the Kerala High Court In STATE BANK OF TRAVANCORE v. CIT [1977] 110 ITR 336, the Board by another circular, withdrew with immediate effect the earlier circular. However, by circular dated October 9, 1984, the Board decided that Interest in respect of doubtful debts credited to suspense account by banking companies would be subjected to tax but Interest charged in an account where there has been no recovery for three consecutive accounting years would not be subjected to tax in the fourth year and onwards. The circular also stated that if there is any recovery in the fourth year or later, the actual amount recovered only would be subjected to tax in the respective years. This procedure would apply to assessment year 1979-80 and onwards.”

8. Considering the facts of the instant case in the light of the decision of the coordinate bench, we are inclined to hold that notice issued u/s 143(2) of the Act is invalid notice and accordingly, the assessment framed consequentially to that is also invalid and is hereby quashed.”

8. Since the facts of the assessee’s case are similar to one as decided by the co-ordinate Bench extracted above, we therefore, respectfully following the same hold that the notice issued u/s 143(2) of the Act is invalid notice and accordingly, the assessment framed consequentially is also invalid and is hereby quashed. The ground no.1 of appeal is allowed.

9. The assessee has also challenged the assessment framed by the national faceless assessment unit on the ground of not having any jurisdiction to frame the assessment. The ld. Counsel for the assessee submitted that the notice u/s 142(1) of the Act was issued by NFAC on 13.01.2021, without having any jurisdiction / power to issue such notice and finally the assessment was framed u/s 143(3) vide Order dated 18.03.2021. The ld. Counsel for the assessee submitted that there is a separate section for issuance of notice u/s 142B of the Act which was inserted from 01.11.2020 for faceless enquiry and valuation.The ld. Counsel for the assessee submitted that u/s 142B of the Act faceless enquiry or valuation scheme 2022 were duly notified on 30th March, 2022, vide notification no.19/2022/F. No.370142/15/2022.TPL for issuing notice u/s 142(1) of the Act in faceless manner through automated allocation in accordance with and to the extent provided u/s 144B of the Act with reference to making faceless assessment of total income or loss of the assessee. Accordingly, section 144B of the Act was also stipulated by Finance Act, 2022, with effect from 01.04.2022, to include provisions for issuance of notice u/s 142(1) of the Act vide clause (iii) of Section 144B of the Act. Accordingly, therefore submitted that national faceless assessment center has no power to issue notice u/s 142(1) of the Act prior to 30th March, 2022, because the scheme of faceless enquiry u/s 142B of the Act for issuance of notice u/s 142(1) by NFEAC was notified on 30.03.2022, vide notification no.19 /2022.

10. The ld. DR on the other hand strongly opposed the argument of the assessee by submitting that the notice u/s 142(1) was issued from the portal of the department and assessee has no locustandi to challenge the said notice.

11. Even on this limb of the argument, we find merit and accordingly, hold that the order passed by the NFAC, is without jurisdiction. In the result, the appeal of the assessee is allowed.

Order pronounced in the open court on 28.08.2025.

Author Bio