Summary: As the fiscal year 2024-25 concludes, timely completion of key year-end tasks is crucial to ensure compliance with various legal and financial regulations. Stakeholders, including promoters, directors, CFOs, and consultants, must prioritize actions across multiple domains. The article emphasizes the closure of regular books of accounts, compliance with the Income Tax Act, GST regulations, Companies Act, labor laws, and more. Essential steps include booking all purchases and expenses, addressing TDS-related matters, reconciling accounts, and ensuring Aadhaar-PAN linkage to avoid penalties. Additionally, tasks like physical verification of assets, managing outstanding dues, and addressing discrepancies in financial statements are highlighted. Businesses should also focus on accurate tax filings, updating PAN-Aadhaar details, and reviewing Annual Information Statements (AIS) for discrepancies. Proper planning, proactive reconciliation, and adherence to deadlines by March 31, 2025, are vital to avoid financial repercussions. The checklist ensures smooth year-end compliance and readiness for the upcoming fiscal year. Also Read: Year-End Compliance Action Points for FY 2024-25 – Volume 2

Page Contents

- YEAR END CLOSING – F.Y. 2024-25 – IMPORTANT ACTION POINTS – VOLUME 1

- A. Books Closure (F.Y. 2024-25):

- B. COMPLIANCE OF INCOME TAX ACT, 1961

- PAN base corrections

- Aadhaar Linkage

- Data corrections at Income Tax site

- 26AS/AIS/TIS

- Annual Returns

- TDS Returns

- Assessments, Outstanding Demands, Issued Letters, Appeals – Ist Appeal/ Tribunal/ High Courts/Supreme Courts

- Appeals – Ist Appeal/Tribunal/High Courts/Supreme Courts

- Higher Income Return but bank payments or withdrawals are less

- Cleaning of books, computers -data, duplicate files, unwanted data etc.

YEAR END CLOSING – F.Y. 2024-25 – IMPORTANT ACTION POINTS – VOLUME 1

Circular No : 3/2025 – Income Tax | Dated: 20th February, 2025

Immediate action is required by all professionals and relevant personnel within the organization. The final month of fiscal year 2024-2025 has commenced, and numerous time-sensitive tasks necessitate prompt completion to avoid financial repercussions. Several year-end closing tasks are subject to compliance deadlines.

Promoters, directors, CFOs, heads of accounts, legal counsel, and professional consultants must ensure the proper closure of their businesses and/or clients’ businesses. Post-year-end (March 31, 2025), corrective actions will be impossible. To assist, the following critical activities must be completed on or before March 31, 2025, or as relevant:

> COMPLETION & CLOSURE OF REGULAR BOOKS

> COMPLIANCE OF INCOME TAX ACT, 1961

> COMPLIANCE OF GST LAW, 2017

> COMPLIANCE OF COMPANIES ACT, 2013

> COMPLIANCE OF LABOR LAWS – PF/ESI/LWF/PT/MWA/Bonus/Gratuity etc

This article is comprehensive, covering numerous Acts and provisions. Readers should review it selectively, focusing on sections relevant to their requirements/expertise.

A. Books Closure (F.Y. 2024-25):

1. Confirm all purchases (goods/services) have been entered for the year and if any advance paid then ask for bill before 31/03/2025 if job done or goods have already been delivered.

2. Confirm all expenses have been booked/entered – properly bifurcated in “Pre-paid” etc. for the year and if any Imprest given to employees then ask for expenses bill in company name /supports before 31/03/2025.

3. Ask to directors/promoters sometime they spent money for official purposes from their own payment methods – UPI/Credit Card/Bank etc -take and compile their statements and accordingly enter in books by giving them suitable credit.

4. Re-check all payments made which attracts TDS have been deducted and deposited to the Govt.

5. Please check validity of PAN number of suppliers, had they linked with Aadhaar, if not then you have to deduct at @20% TDS instead regular rate.

6. All TDS on salary payments have been calculated/recalculated due to any variation in pay and all supports have been submitted by employees of their Investments, HRA etc. (For salary TDS please refer circular n0. 03/2025 dt.20/02/25 – attached with article).

7. Check for all Directors/promoters if their emoluments/earnings you want to increase/pay then this is high time to book by deducting proper TDS- 31/5/2025 Financial Year Closing Month March 2025–

8. Nowadays so many investments – SIP/Shares/Pvt/Public/F & O/Trading etc are being done by businessmen or employees – their accounting for tax purposes is must before 31st March, otherwise late payments of advance tax will attract interest/penalties.

9. Match your earnings by Form 26AS till Dec 2024, because TDS return of March 25 qtr will be filed by payers up to 31/05/2025 so you have to wait till that date for March, 25 payments.

10. Confirm all Invoices have been raised to the client, and specially confirm any short payment came to you, is any credit note required to be issued and corresponding correction in March 25 GST return required or if it is bad debt then also issue Credit Note for the same and your GST returns are open for corrections for the year 24-25.

Imp to note- a new system in GST has been introduced where you can accept/reject/hold Invoices raised by your supplier and like wise your client can also do; You can check at GST portal under Services Heading Sub Heading IMS Dashboard system Inward/Outward Supplies and accordingly correct your books by issuing debit or credit note.

11. Any capitalization left in books – check if any payments made to contractors for work under work progress or any advance paid for Capital Assets is un-adjusted all be careful and do it in same month for getting adequate Depreciation or ITC on the same.

12. Reconcile with Statement of Accounts of your suppliers & clients or customers for F.Y.24-25 up to Feb, 2025 so that anything being left can be accounted for within March 25.

13. Kindly sent “Statement of Accounts” to your clients for reconciliation.

14. Check outstanding dues – they should not be time barring – i.e. 3 years from their due date, if anyone is time barring then immediate contact to your lawyer and issue a legal notice. (outstanding from Feb 2022 are time barred in March 25 cannot file court case)

15. Plan physical verification of fixed assets, movable assets, inventory, stocks, consumables etc. If you have pan-India offices then start immediate action.

16. Do all bank reconciliations, including abroad accounts if any.

17. Branch accounts reconciliations – their trails up to Feb 25 and opening balances.

18. Kindly re-verify opening balances from audited accounts of F.Y. 2023-24.

19. Re-check any claim is pending to recover – from Govt or non Govt because at year end grants returned by departments.

20. Check all vouchers, bills have been certified and checked by concerning authorities.

21. Complete your filings – recheck all notices, office orders have been placed and indexed accordingly.

22. Get approvals of any shortages in funds, inventory etc from concerning authorities.

23. Check – replies of your directors for qualifications in last year audit reports or internal audit reports that has been complied or not otherwise in next year same observations shall be repeated by auditors.

24. Re-check back up of all accounting, office, TDS, GST, HR, IT software have been taken by computer man or not, check by yourself do not believe on their versions.

25. It is better to prepare salary paid/accrued during the year in format of employee ID, Name, Designation, PAN, Aadhaar, Bank a/c no., amount paid/credited.

B. COMPLIANCE OF INCOME TAX ACT, 1961

It can be further sub divided in to:

- PAN base corrections

- Aadhaar Linkage

- Data corrections at Income Tax site

- 26AS/AIS/TIS

- Annual Returns

- TDS Returns

- Assessments

- Outstanding Demands

- Issued Letters

- Appeals – Ist Appeal/Tribunal/High Courts/Supreme Courts

- Cleaning of books, computers -data, duplicate files, unwanted data etc.

PAN base corrections

Check by logging IT portal then go to profile section, this is situated at extreme right. Click at your name then below icons will be opened, then select “My-Profile”

At profile section, check is your pan address is same as your business or IT address is actually going on or it has been left inadvertently to correct it. If you are an individual then also compare it with Aadhaar Base by clicking on – it will take some authentications and if all fields of Aadhaar and PAN are same ignore it and if major difference then please correct PAN by Aadhaar details. (Note -Aadhaar may have been linked with PAN it does not mean you are free to give wrong information to the department.)

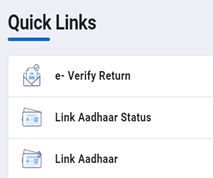

Aadhaar Linkage

Although everyone must have already done this exercise but I found at many occasions, still some persons have not still linked with Aadhaar and letter from TDS department is coming at higher rate of TDS @20%; Just check by without logging https://www.incometax.gov.in/iec/foportal/ and go to quick links as under:

Here you can check status as well link by paying late fee. Link steps are very easy.

Data corrections at Income Tax site

Read carefully all contents of main IT site after logging in and check whether all details of profile – name, address, e-mail, telephone, communication address all are correct or not.

Further, in TRACES also check all detail are Ok or not also add DSC here too so that you can digitally sign the documents. Also, now a days on same e-filing portal TDS return filing facility is also available. It is very easy no need to go anywhere or at Alankit etc.

26AS/AIS/TIS

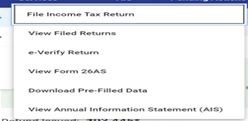

This is very helpful tool available at E-filing portal – in future 26AS is going to be discontinued, you will get all at TIS/AIS. How can you access it – simply login at normal IT portal it will bring you other site – steps are as under:

STEP 1: Click E Filing < Income Tax Returns < Form 26 < View Annual AIS

STEP 2: When you will go to View Annual Information tab then it will ask you “On click of ‘Proceed’ button, you will be redirected to the Compliance Portal” then proceed.

There you will get 2 tabs 1- TIS & 2 AIS.

> The TIS is summary of information – it contains – your billings – business receipts, TDS details, your investments Shares, FDRS, SIP etc, your earnings dividend, interest, salary, interest on refund of IT Act, your cash deposits etc. Actually, it is actually a complete जनम पत्री of your financial transactions for the F.Y. 2024-25.

> The Annual Information Statement (AIS) provides a mechanism for reviewing and rectifying financial transactions. For instance, an erroneous PAN entry by a third party, unrelated to the taxpayer, will appear as an anomaly within the AIS. Failure to address such discrepancies may result in a notice from the Income Tax Department. Consequently, the AIS offers a means to correct data entry errors within the Government of India’s systems. The process for correction is as follows:

Step 1- You have been directed to AIS and you have proceeded there.

Step 2 – Click at download button on AIS

Step 3 – Select download for – Annual Information Statement (AIS) – JSON (for AIS Utility)

Step 4 – At AIS portal – click Resource > Utility > Download as per Window or Mac

Step 5 – When you down loaded J son file at step 3 above then open it in software loaded at step 4 above.

Step 6 – After loading it will be opened and press tab TDS/TCS Information under Part B of AIS check seriously all entries and if you have any doubt then press arrow > of that item then further details will be opened here you will see extreme right 2nd last tab–

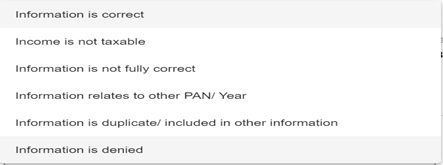

“Active Feedback” which is optional –

Step 7 – A separate window will be opened – all details shall be appeared and then you will be able to give feed back of it’s correctness in drop down of Feedback Type – as under:

Step 8 – Now select correct feedback and submit, this will exonerate you from giving or accepting any wrong information.

Why it is a necessary part of year closing exercise because you can on time inform to your counter part so that he can also correct his records on time and will be from any wrong doings.

Annual Returns

Every year this exercise is being done as per the time prescribed by the Income Tax department. Here, two points have to be considered:

1st – You may have left or your client left to file the return of f.y. 2023-24 or earlier or as per the information available at portal or by notice of Income Tax or any new fact came in your knowledge you have become eligible to file return or you want to revise upward your income through filing of return again. So, new section has been introduced in IT Act -i.e. 139(8A) – an updated return. So, last date for filing updated return is 31/03/2025 is for f.y.2021-22; 31/03/2026 is for f.y. 2022-2023; 31/03/2027 is for f.y. 2023-24 with max 50% additional tax and if within one year then 25% additional tax in addition interest is also payable.

From Budget 2025 it has increased to 4 years – with rider 1 year late 25% additional tax, 2 years 50% additional tax, 3 years 60% additional tax & 4 years with 70% additional tax – in addition interest is also payable

Note – In updated returns you can up your income and you cannot file for any refunds; also it is with additional tax @25% if filed within 12 months & 50% within 24 months of extended filing time + interest + late filing fee.

So, just give a thought if you cross the limit of 12 months then sudden liability will be increased to double & if you miss the date of 31/03/25 then you will lose the filing opportunity for f.y. 2021-22.

TDS Returns

Regularly you must be filing TDS returns, but as a quick approach to know for any default in filing the returns of TDS or late filing is – when you go to check Form 26AS then a window of defaults opened at normal IT portal without going to TRACES.

Check and correct the defaults. Further, also check any penalty for invalid PANs have come then correct through console file and deduct more money of your supplier from his bills against these liabilities imposed by department. Because, TDS deposited by you @20% will also be reflected in supplier account and he will get refund.

In March 25 month please check carefully all such defaults and recover your money from supply and safeguard your money.

Assessments, Outstanding Demands, Issued Letters, Appeals – Ist Appeal/ Tribunal/ High Courts/Supreme Courts

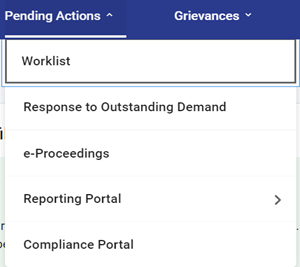

These details are available at E Filing Income Tax portal. For this you have to first log in and then press tab “Pending Actions” then following selections tabs will be displayed:

In this area of portal all tabs have their own very relevant meanings.

- WORKLIST: will show you your pending actions – like approvals as assessee to your auditor’s reports, or your approvals for appointments of consultants etc. So, check anything if pending then execute as soon as possible.

- RESPONSE TO OUTSTANDING DEMAND: This is mostly not checked by accountants, most of the times they do not have password to access and consultants have less time. Therefore, demands lied unentertained by assessee and interest liability piles up.

- E-PROCEEDINGS: Here you will find two tabs – one “For your information” & “For your action”. These are self-explanatory and you will find in for your action tab may you come across with many more letters, notices etc. Where you have notice option, reply option-where you can see your earlier replies also. If you have forgotten to reply earlier and if you find again same letter then if you reply current notice then it will cover earlier too.

In March 2024 check it seriously because there may be time barring as at 31/03/2025.

Appeals – Ist Appeal/Tribunal/High Courts/Supreme Courts

This details you will find in your portal under “Income Tax Forms” where you can see your filed appeals and at “for your action” tab you can see letter for appearing or reply for appeal. It is many time left to check and e -mail is also overlooked so again I will insist to check in March 24 to avoid any delay or time barring of any reply.

Higher Income Return but bank payments or withdrawals are less

The IT department’s current practice involves issuing scrutiny letters to taxpayers whose reported income on their ITR filings significantly exceeds their documented banking transactions. This discrepancy raises concerns about undisclosed income or cash transactions used for daily expenses, household needs, and travel. Therefore, it is advisable to utilize bank funds for all expenditures and avoid holding excessive unutilized cash. Check passbook and if withdrawals in 2024-25 are less then withdraw and spent

Cleaning of books, computers -data, duplicate files, unwanted data etc.

This topic I have covered under Income Tax deliberately because whenever Survey, Search & Seizer is conducted by IT department then they take books/computers/supports etc in their possession. So, not only year end this is actually should be done every month because unwanted raw data left in drives, computers etc and hard copies of unrelated, unwanted documents left in the premises of the organisation. Therefore, only correct, actual and related data/documents/files/back ups etc should be kept in the premises.

Many MISs made to check as estimates/budgets/proposals etc which are not near to actual results and then in investigation it becomes difficult to explain to the authorities about their correctness & sanctity. Even some time personnel bring their personal data to the computer of companies/ many photos etc are also uploaded in company computers which should also be check and removed from the premises of company.

In my opinion only true books should be kept at the premises of company or at business premises.

>>>>>> My volume 2 for other aspects of GST/Companies Act/Labour Laws for closing of the year 2025 will be published very soon, till then take care of above given action points & procedures.

Author Bio