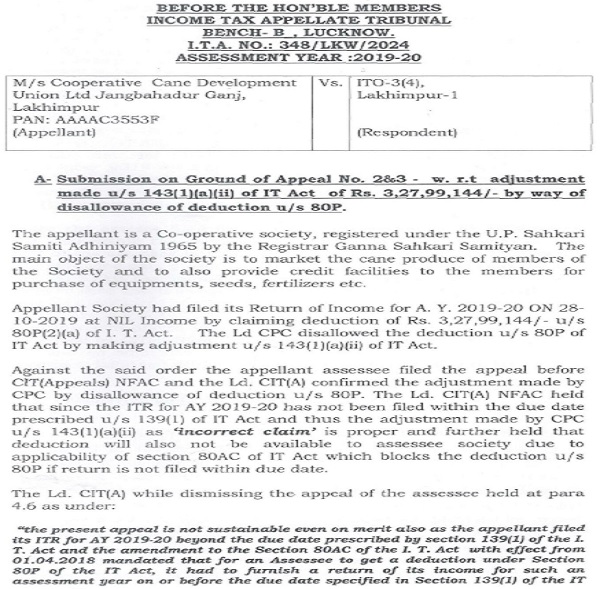

Case Law Details

Co-operative Cane Development Union Limited Vs ITO (ITAT Lucknow)

ITAT Lucknow held that delay of 4 days erroneously calculated as delay of 551 days by CIT(A). Accordingly, directed CIT(A) to consider request of condonation and if found appropriate to grant opportunity of being heard.

Facts- The return filed by the assessee was processed u/s 143(1) of the Act and an intimation dated 29/10/2020 was issued to the assessee by Revenue denying the deduction claimed u/s 80P of the Act on the ground that the return filed by the assessee was beyond the due date for filing return as prescribed u/s 139(1) of the Act. The assessee filed appeal against the aforesaid intimation issued u/s 143(1) of the Act in the office of learned CIT(A). Vide impugned appellate order dated 11/03/2024, the assessee’s appeal was dismissed on grounds of limitation and also on merits.

Conclusion- Held that undisputedly there was delay of 4 days in filing of the appeal by the appellant assessee in the office of the learned CIT(A). However, the learned CIT(A) has erroneously observed that the delay was of 551 days. In view of the foregoing, the impugned appellate order dated 11/03/2024 of the learned CIT(A) is set aside and he is directed to pass fresh order in accordance with law on the issue of assessee’s request for condonation of delay. For this purpose the learned CIT(A) is directed to respectfully follow the aforesaid order dated 10/01/2022 of Hon’ble Supreme Court. Further if the learned CIT(A) deems it proper to condone the delay on the part of the assessee in filing of the appeal in the office of the learned CIT(A), then the CIT(A) is further directed to decide the assessee’s appeal on merits. While deciding the appeal of the assessee on merits, if such a situation arises, the learned CIT(A) is further directed to give due consideration to decided precedents in the case of Income Tax Appellate Tribunal, which, as contended by the assessee, squarely covers the issue in dispute on merit in favour of the assessee.

FULL TEXT OF THE ORDER OF ITAT LUCKNOW

(A) This appeal vide I.T.A. No.348/Lkw/2024 has been filed by the assessee for assessment year 2019-20 against impugned appellate order dated 11/03/2024 (DIN & Order No.ITBA/APL/S/250/2023-24/1062407234(1) of Addl./ Jt. Commissioner of Income Tax (Appeals). In this appeal, the assessee has raised the following grounds:

“1. The Ld CIT(A) NFAC erred on facts and in law in dismissing the appeal in limine by not condoning the delay of 551 days in filing of appeal owing to Covid-19 pandemic and without considering that the delay period is covered by the judgement of Hon’ble Supreme Court in Suo moto Writ petition No. 3/2020 and also by the CBDT Circular 10/2021 dated 25.05.2021.

WITHOUT PREHUDICE TO ABOVE

2. That the Ld. C.I.T. (A), NFAC, erred on facts and in law in not allowing deduction u/s SOP of Chapter VI-A of I. T. Act o f Rs.3,27,99,144/- and in doing so failed to consider that the return was filed within the extended due date prescribed by CBDT.

3. That Ld. C.I.T. (A) NFAC had further erred on facts and in law in incorrectly stating that the Return was filed beyond the time limit specified u/s 139(1) of I.T. Act and thereby erroneously invoked the provisions of Section 80AC and upheld the disallowance of deduction as incorrect claim by way o f adjustment u/s 143(1)(a)(ii) of I. T. Act.

4. That the addition confirmed is highly excessive, contrary to the facts, law and principle of natural justice and without providing sufficient time and opportunity to have its say on the reasons relied upon by CIT(A).”

(B) This appeal has been filed beyond time limit prescribed u/s 253(3) of the I. T. Act. As per noting of the Registry, the appeal is time barred by 6 days. An application was filed from the assessee’s side for condonation of delay on the ground that the Secretary of the appellant society was on election duty. An affidavit has also been filed from the assessee’s side in support of the request for condonation of delay of 6 days in filing of this appeal. The learned D.R. for Revenue expressed no objection to condonation of delay in filing of the appeal. In view of the foregoing and having regard to section 253(3) of the I. T. Act, the delay in filing of the appeal is condoned and the appeal is admitted.

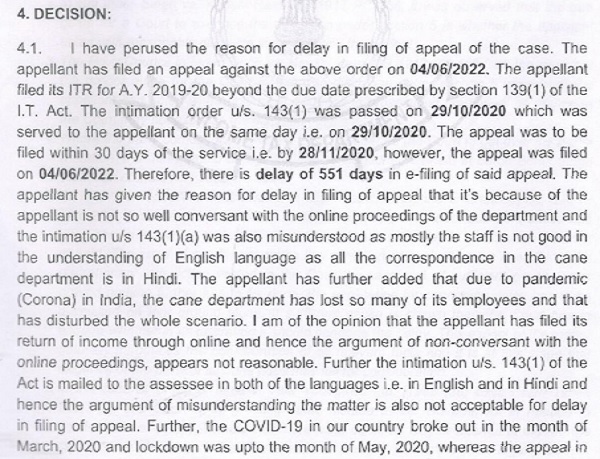

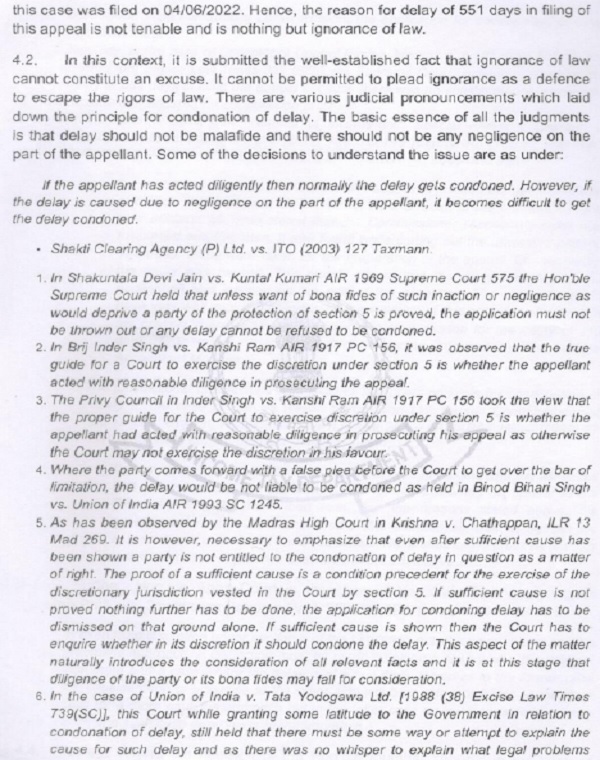

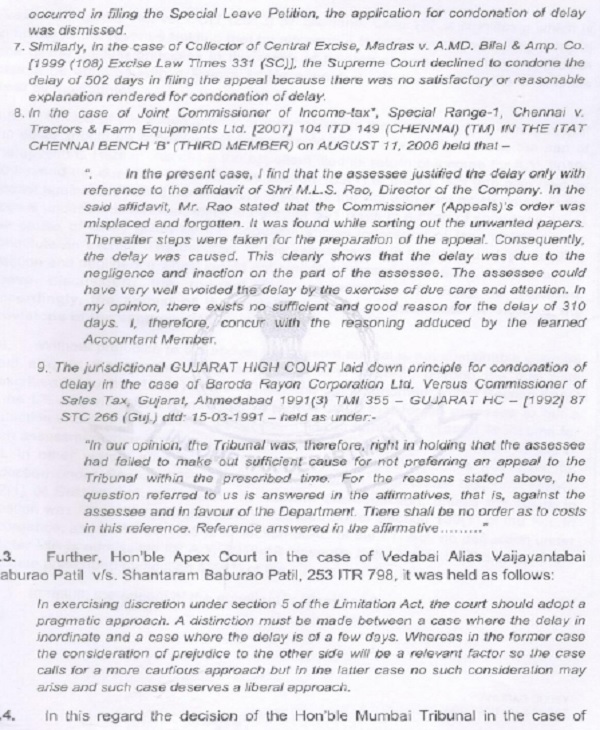

(C) In this case the return filed by the assessee was processed u/s 143(1) of the Act and an intimation dated 29/10/2020 was issued to the assessee by Revenue denying the deduction claimed u/s 80P of the Act on the ground that the return filed by the assessee was beyond the due date for filing return as prescribed u/s 139(1) of the Act. The assessee filed appeal against the aforesaid intimation issued u/s 143(1) of the Act in the office of learned CIT(A). Vide impugned appellate order dated 11/03/2024, the assessee’s appeal was dismissed on grounds of limitation and also on merits. The relevant part of the order of the learned CIT(A) is reproduced below:

–

–

(D) At the time of hearing before us, the learned A.R. for the assessee submitted that the learned CIT(A) erroneously observed that there was delay of 551 days in filing of the appeal in the office of the learned CIT(A) against the aforesaid intimation issued u/s 143(1) of the Act. He submitted that the actual delay was of only 4 days. It was submitted that even on merits, the order of the learned CIT(A) was erroneous because the due date of filing of return was extended upto 31/10/2019, and the assessee had filed return well before that date i.e. on 28/10/2019. In this regard, the learned A.R. for the assessee drew our attention to the written submissions, which is reproduced below for the ease of reference:

Act. In other words, after 01.04.2018, even if the asseessee makes this claim for deduction under Section 80P in a return filed within time under Section 139(4), 142(1) or section 148, he will not be allowed the deduction, unless the return in question was filed within the due date prescribed under Section 139(1) of the Act. In accordance, as per the provisions of section 8OAC of the IT Act, no deduction under chapter VIA is admissible for AY 2018-19 onwards, if the return is filed beyond the due date prescribed by section 139(1) of the I. T. Act”.

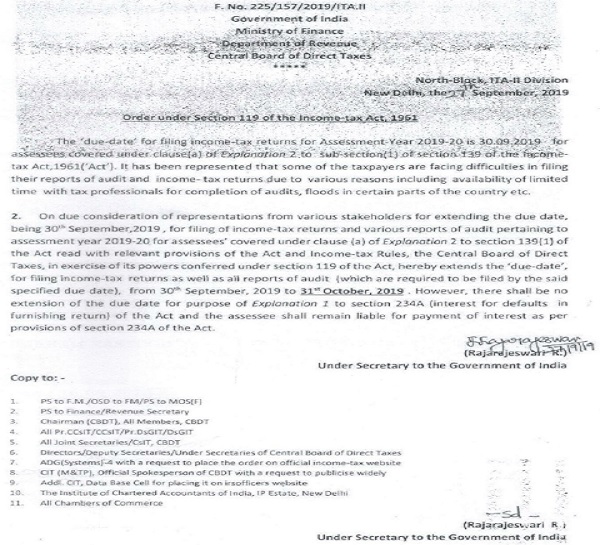

It is prayed that appellant society filed its return of income in ITR-5 on 28-10-2019 which was filed within the extended due date prescribed u/s 139(1) of IT Act. It is prayed that for AY 2019-20 the CBDT extended the due date for filing of returns by issuing Order dated 27th September 2019 u/s 119 of IT Act. Copy of order u/s 119 is at page 03 of the paper book. By way of such order the due date for filing of Returns for assesse covered under clause (a) of explanation 2 to section 139(1) got extended uptill 31st October 2019.

Since the assesse filed its return of income on 28-10-2019 which was well within the extended due date, there was no delay on the part of the assessee in filing of return as the return was filed as per due extended date prescribed u/s 139(1) of IT Act and thus the LD. CIT (A) NFAC has wrongly conceived that ITR for AY 2019-20 was delayed filed and thus adjustment u/s 143(1)(a)(ii) was permissible.

It is therefore prayed that the adjustment made by CPC and further confirmed by CIT(A) NFAC is incorrect as there is no delay in filing of ITR and no adjustment can be made u/s 143(1)(a)(ii) on account of `incorrect claim’ and neither on account of section 80AC of IT Act.

B- Submission on Ground of Appeal No. 1 – .

It is most humbly prayed that Hon’ble Supreme Court vide order dated 23.03.2020 in suo moto Writ Petition No. 3 of 2020 took suo moto cognizance of the difficulties faced by the litigants in filing of appeal due to outbreak of the COVID 19 PANDEMIC directed that the period of limitation under any general or specific law in respect of all judicial or quasi-judicial proceedings, whether condonable or not shall get extended till further orders. Though such order relaxation was provided for period of limitation between 15.03.2020 and 14.03.2021. Thereafter due to second surge in COVID 19 cases through miscellaneous application no. 665 of 2021, the Hon’ble Supreme Court vide order dated 23.09.2021 extended the period of limitation w.e.f. 15.03.2020 till 02.10.2021.

He also drew our attention to the notification of CBDT dated 27/09/2019 whereby the due date of filing return was extended upto 31/10/2019. The aforesaid notification of the CBDT is reproduced below for the ease of reference:

(D.1) The learned A.R. for the assessee, further drew our attention to the order of Hon’ble Supreme Court dated 10/01/2022 in support of his contention that the actual delay was of only 4 days and not of 551 days as erroneously observed by the learned CIT(A). The aforesaid order of Hon’ble Supreme Court is reproduced below for the ease of reference:

IN THE SUPREME COURT OF INDIA

CIVIL ORIGINAL JURISDICTION

MISCELLANEOUS APPLICATION NO. 21 OF 2022

IN

MISCELLANEOUS APPLICATION NO. 665 OF 2021

IN

SUO MOTU WRIT PETITION (C) NO. 3 OF 2020

IN RE: COGNIZANCE FOR EXTENSION OF LIMITATION

WITH

MISCELLANEOUS APPLICATION NO.29 OF 2022

IN

MISCELLANEOUS APPLICATION NO. 665 OF 2021

IN

SUO MOTU WRIT PETITION (C) NO. 3 OF 2020

Order

1. In March, 2020, this Court took Suo Motu cognizance of the difficulties that might be faced by the litigants in filing petitions/ applications/ suits/ appeals/ all other quasi proceedings within the period of limitation prescribed under the general law of limitation or under any special laws (both Central and/or State) due to the outbreak of the COVID-19 pandemic.

2. On 23.03.2020, this Court directed extension of the period of limitation in all proceedings before Courts/Tribunals including this Court w.e.f. 15.03.2020 till further orders. On 08.03.2021, the order dated 23.03.2020 was brought to an end, permitting the relaxation of period of limitation between 15.03.2020 and 14.03.2021. While doing so, it was made clear that the period of limitation would start from 15.03.2021.

3. Thereafter, due to a second surge in COVID-19 cases, the Supreme Court Advocates on Record Association (SCAORA) intervened in the Suo Motu proceedings by filing Miscellaneous Application No. 665 of 2021 seeking restoration of the order dated 23.03.2020 relaxing limitation. The aforesaid Miscellaneous Application No.665 of 2021 was disposed of by this Court vide Order dated 23.09.2021, wherein this Court extended the period of limitation in all proceedings before the Courts/Tribunals including this Court w.e.f 15.03.2020 till 02.10.2021.

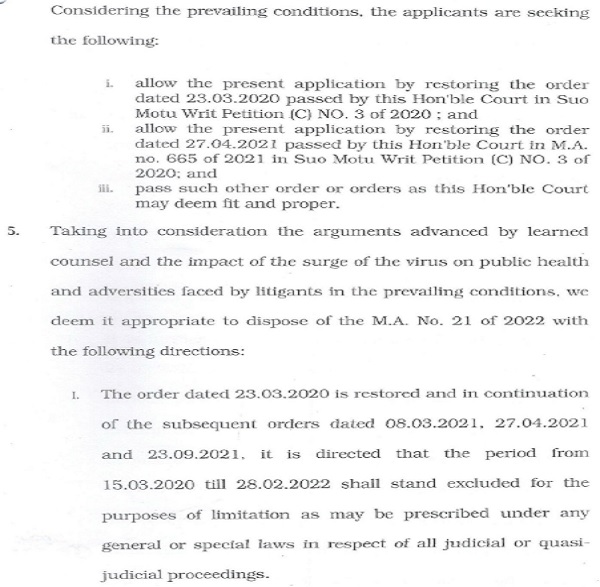

4. The present Miscellaneous Application has been filed by the Supreme Court Advocates-on-Record Association in the context of the spread of the new variant of the COVID-19 and the drastic surge in the number of COVID cases across the country. Considering the prevailing conditions, the applicants are seeking the following:

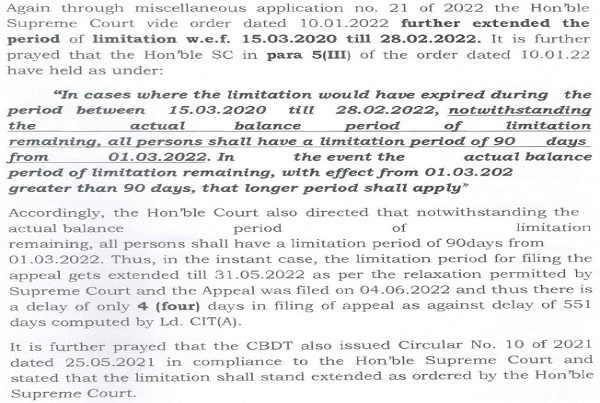

II. Consequently, the balance period of limitation remaining as on 03.10.2021, if any, shall become available with effect from 01.03.2022.

III. In cases where the limitation would have expired during the period between 15.03.2020 till 28.02.2022, notwithstanding the actual balance period of limitation remaining, all persons shall have a limitation period of 90 days from 01.03.2022. In the event the actual balance period of limitation remaining, with effect from 01.03.2022 is greater than 90 days, that longer period shall apply.

IV. It is further clarified that the period from 15.03.2020 till 28.02.2022 shall also stand excluded in computing the periods prescribed under Sections 23 (4) and 29A of the Arbitration and Conciliation Act, 1996, Section 12A of the Commercial Courts Act, 2015 and provisos (b) and (c) of Section 138 of the Negotiable Instruments Act, 1881 and any other laws, which prescribe period(s) of limitation for instituting proceedings, outer limits (within which the court or tribunal can condone delay) and termination of proceedings.

(D.2) On merits, the learned A.R. for the assessee submitted that the issue was also covered in favour of the assessee by the order dated 24/10/2024 of ITAT, Lucknow Bench in the case of Co-op Cane Development Union Gola vs. Income Tax Officer in I.T.A. No.185/Lkw/2024. The relevant portion of the order is reproduced below:

2. In this appeal, the assessee has raised the following grounds: –

“(1). That the Ld. C.I.T. (A), NFAC, erred on facts and in law in not allowing deduction u/s 80P of Chapter VI-A of I. T. Act of Rs. 11,07,25,716/- by incorrectly stating that the Return was filed beyond the time limit specified u/s 139(1) of I. T. Act and thereby invoking the provisions of section 80AC of I. T. Act , upheld the disallowance of deduction as incorrect claim by way of adjustment u/s 143(1)(a) of I. T. Act.

(2) That Ld. C.I.T. (A) NFAC erred on facts and in law in not considering that the Return was filed within the due date extended by the CBDT vide order dated 27.09.2019 u/s 119 of the I. T. Act i.e. 31.10.2019.

(3) That the present disallowance is highly excessive, contrary to the facts, law and principle of natural justice and without providing sufficient time and opportunity to have its say on the reasons relied upon by him.”

3. In this case, the assessee’s return showing nil income was processed by Centralized Processing Center (CPC) of Income Tax Department, u/s 143(1) of the Act, and intimation was issued by CPC to the assessee, u/s 143(1) of the Act, wherein the assessee’s claim for deduction u/s 80P of the Act was disallowed. The assessee filed appeal in the office of the Ld. CIT(A). Vide impugned appellate order dated 07/02/2024, the Ld. CIT(A) dismissed assessee’s appeal on the ground that the assessee failed to filed the return of income within the due date satisfied u/s 139(1) of the Act. The Ld. CIT(A) has also observed in his impugned appellate order that First Appellate Authority was not invested with powers of condoning the delay of filing of return of income. The relevant portion of the impugned appellate order dated 07/02/2024 of the Ld. CIT(A) is reproduced as under: –

“4.1 Ground Nos. 1 to 5:

The appellant has raised five grounds of appeal. However, the main issue raised by the appellant is the disallowance of deduction u/s 80P by the AO, – CPC, Bengaluru which has been challenged by the appellant on the following grounds.

(i) The Return of Income was not filed within the due date.

(ii) The disallowance u/s 80(P) was outside the scope and ambit of section 143(1)(a)(iv) for A.Y. 2019-20.

It is seen from intimation order that the due date of filing of original return of income for the AY 2019-20 was 30/09/2019, however the appellant has filed its return of income on 27/10/2019. Thus, the return of income has not been filed within the due date as prescribed in section 139(1) of the Act. Accordingly, as per the provisions of section 80AC of the Act, the claim of “deduction u/s 80P has been rejected by CPC.

As per the provisions of section 80AC(ii), no deduction under any provisions of Chapter VIA under the head “C-deduction in respect of certain incomes’ will be allowed w.e.f. 01/04/2018 unless an assessee filed the return of his income on or before the due date specified under sub section (1) of section 139. Since the said provision was effective from 01/04/2018, the assessment year. involved in the present case falls within the purview of amended section 80AC of the Act as the return of income was filed beyond the due date. Thus, since the return has: been filed beyond the due date u/s 139(1) of the Act, the appellant is not eligible to claim deduction u/s 80P rws 80AC, ‘the only remedy available lies in the machinery provisions of the Act rather seeking legal remedy. Such provisions are found in section 119(2)(b) which ‘enables an assessee to approach the Board for seeking relief in such cases. The provisions of section 119%2)(b) are reproduced below:

Section 119:

“Instructions to subordinate authorities.

1. The Board may from time to time…

2. Without prejudice to the generality of the foregoing power,

(b) the Board may, if it considers it desirable 6F expedient so to do for avoiding. genuine hardship in any case or class, by general or special order, authorize (any income tax authority, not being a Commissioner (Appeals) to admit an application or claim for any exemption, deduction, refund, or any other relief under this Act after expiry of the period specified by or under this Act for making such application or claim and deal with the some on merits in accordance with law.”

From the above, it is clear that the first appellate authorities have not been entrusted with powers of condoning delay in such cases. The intention of legislature with respect to such cases is very clear that the remedy in such situation lies in the section 119 of the Act.

4.2 At this stage, it will be relevant to reproduce the relevant provisions of section 143(1) of the Act which is as under:

| (a) | The total income or loss shall be computed after making the following adjustment, namely- | |

| (i) | Any arithmetical error in the return: | |

| (ii) | An incorrect claim, if such incorrect claim is apparent from any information in the return | |

| (iii) | Disallowance of loss claimed, if return of the previous year for which set off of loss is claimed was furnished beyond the due date specified under sub-section (1) of section 139; | |

| (iv) | Disallowance of expenditure indicated in the audit report but not taken into account in computing the total income in the return; | |

| (v) | Disallowance of deduction claimed under section 10AA, 80-IA, 80IAB, 80-IB, 80IC, 80ID or section 80-IE if the return is furnished beyond the due date-specified under sub-section(1) of section 139; or | |

| (vi) | Addition of income appearing in Form 26AS or form 16A or Form 16 which has not been included in computing the total income in the return; |

“143. (1) Where a return has been made under section 139, or in response to a notice under sub-section (1) of section 142, such return shall be processed in the following manner, namely:

Provided that no such adjustments shall be made unless an intimation is given to the assessee of such adjustments either in writing or in electronic mode, Provided further that the response received from the assessee, any, shall be considered before making any adjustment, and in a case where no ‘response is received within thirty days of the issue of such intimation, such adjustments shall be made-]

Explanation.— For the purposes of this sub-section, (a) “an incorrect claim apparent from any information in the return” shall mean a claim, on the basis of an entry, in the return,-

| (i) | Of an item, which is inconsistent with another entry of the same or some other item in such return; | |

| (ii) | In respect of which the information required to be furnished under this Act to substantiate such entry has not been so furnished; or | |

| (v) | In respect of a deduction, where such deduction exceeds specified statutory limit which may have been expressed as monetary amount or percentage or ratio or fraction, |

A perusal of clause (iv) to section 143(1)(a) of the Act would show that it ‘provides for disallowance of expenditure indicated in the audit report, but not taken into account in computing the total income in the return.

4.3 On perusal of the above section it is seen that section an incorrect claim ‘can be disallowed as per the provisions of section 143(1)(ii) of the Act. Therefore the AO, CPC, Bengaluru had rightly disallowed the deduction u/s 80P by following the provisions of section 80AC of the Act.

4.4 The Hon’ble Madras High Court in the case of Veerappampalayam Primary Agricultural Co-op Society Ltd. Vs DCIT [138 taxmann.com 571] dealt the similar issue in WP No. 7038 of 2020 and has decided the matter in favour of the revenue. The Hon’ble Court has held as under:

“Section 80AC of the Income Tax Act, 1961DeductionNot to be allowed unless return furnished (Belated Return)Assessment Year 2018-19Whether provisions of section 80AC(ii) make it clear that any deduction that is claimed under Part C of Chapter VIA would be admissible only if return of income in that case were filed within prescribed due date Held, yes, whether thus, no – Claim under any provisions of Part C of Chapter VIA would be admissible in case of a belated return Held, Yes.

Section 143 of the Income Tax Act, 1961AssessmentGeneral (Intimation under section 143(1)(a))Assessment Year 2018-19, Whether scope of an intimation under section 143(1)(a), extends only to making adjustments based upon errors apparent from return of income and patent from record Held, yes (in favour of revenue).”

The Hon’ble Court has noted that the provisions of section 80AC are very clear in the sense that the any deduction claimed under Part C of Chapter VIA would be admissible only if return of income is filed within prescribed due – date. As the date of filing of return of income is apparent from the return itself, the AO CPC, could easily draw an inference whether the claim of deduction is admissible in accordance with the provisions of section 80AC of the Act which is a basically a mechanical exercise and falls within purview of section 143(1)(a) of the Act.

Further, in a latest decision in the case of Janki Vaishali Co-op Housing Society Ltd. Vs CIT(A), NAFAC, the Hon’ble ITAT Mumbai Bench in ITA No. 944/Mum/2022( AY 2018-19) has also laid the similar position of law and upheld the decision of the Ld.CIT(A) wherein the disallowance u/s 80P of the Act was upheld for the reason that the return of income was filed beyond the due date as specified in section 139(1) of the Act.

4.5 Further, at this juncture, it would not be irrelevant to discuss the decision of the Hon’ble Apex Court in the case of CC v. Dilip Kumar & Company [2018] 95 taxmann.com 327/69 GST 239, wherein the Hon’ble Court has laid down following principles:

(a) Exemption notification/provisions should be interpreted strictly, the burden of proving applicability would be on the assessee to show that his case comes within the parameters of exemption clause or exemption notification.

(c) In case of ambiguity in a charging provision, the benefit must necessarily go in favour of subject/assessee but the same is not true for an exemption notification wherein the benefit of ambiguity must be strictly interpreted in favor of the revenue/state

‘From the principle laid down by the Hon’ble Apex Court in the above case, it is _amply clear that the provisions of exemption as well as deduction provided in the Statute are to be interpreted strictly and onus always lies with the claimer to Substantiate that there is no violation of governing provisions while claiming exemption/deduction as per the law. By following the ratio laid down by the Hon’ble ‘Apex Court in the case of Dilip Kumar, it is clear that the onus was on the appellant to Substantiate that the claim of deduction was admissible in accordance with the Governing provisions of the Act. However, it is clear that in the instant case, there is Clear violation of provisions of section 80AC(ii), therefore, the claim of deduction is also not admissible in the light of the provision of section 80AC(ii) and in view of the decision of Apex Court in the case of Dilip Kumar( Supra).

4.6 Further, the Hon’ble Apex court in the case of Principal Commissioner of Income Tax-lll, Bangalore and another Vs. M/s Wipro Limited (Judgment ‘dated 11.07.2022 in the Civil Appeal No. 1449 OF 2022) has applied strict construction to reverse the findings of the Hon’ble High Court (“HC”) of Karnataka which had earlier allowed carry forward of such losses. The Hon’ble SC held that the requirement of filing a declaration within a timeline is “mandatory” in nature as per the language of the provision. It reiterated the age-old principle that a taxing statute should be read as it is and held that the exemption/ deduction provisions should be “strictly” and “literally” complied with and, therefore, a strict interpretation should be adopted.

4.7 The appellant has relied on the following case laws

(i) Order of the NFAC in Appeal no. NFAC/2018-19/10140506, dated 29/10/2020 in the case of Hardoi District Cane Growers Co-operative Society – Ltd for A.Y. 2019-20.

(ii) Order of NFAC in Appeal no. NFAC/2018-19/10098136, dated 11/08/2023 in the case of Sahkari Ganna Vikas Samiti Ltd for A.Y.2019-20.

(iii) Order of NFAC in Appeal no. NFAC/2018-19/10014459, dated 12/04/2022 in the case of Sahkari Ganna Vikas Samiti Ltd, Puranpur for A.Y. 2018-19.

However in view of the express provisions contained in section 119(2)(b) and the decision of the Hon. Madras High Court quoted above the decision relied upon by the appellant is not acceptable,

In view of the above, I am of the considered opinion that the AO CPC has rightly disallowed the claim of deduction u/s 80P as the return of income was filed beyond the due date. Also for the fact that first appellate authorities have not been given the power to condone and relying upon the provisions of section 80AC and the judicial pronouncements referred above, these grounds of appeal are dismissed.

5. In the result, appeal of the appellant is Dismissed.”

4. Aggrieved, the assessee filed this present appeal in Income Tax Appellate Tribunal (ITAT) against the aforesaid impugned appellate order dated 07/02/2024 of the Ld. CIT(A). At the time of hearing before us, the Assessee was represented by Shri Shubham Rastogi, Authorized Representative for the Assessee and Revenue was represented by Shri Manu Chaurasia, Ld. CIT-DR. The Ld. Authorized Representative (“AR”) for the Assessee submitted that the due date for filing of the return was extended by the Central Board of Direct Taxes (CBDT) from 30/09/2019 to 31/10/2019. In this regard, he drew our attention to page no. 1 of u/s 143(1) of the Act, wherein categorically, it is mentioned that the extended due date of filing original return was 31/10/2019. Thus, he contended that the return of income filed by assessee on 27/10/2019 was well within the time as extended by CBDT. He submitted that the addition made u/s 143(1) of the Act be deleted and that the Assessing Officer be directed to allow the deduction under section 80P of the Act as claimed by the assessee.

4.A. The Ld. CIT-DR for Revenue left the matter to the discretion of the Bench.

5. It is not in dispute that the due date for filing of original return was extended by CBDT from 30/09/2019 to 31/10/2019; which is also acknowledged in the intimation u/s 143(1) of the Act. The relevant portion at page no. 1 of the intimation issued by CPC to the assessee u/s 143(1) of the Act is reproduced as under: –

6. Since the assessee has filed return of income on 27/10/2019, which is well within the time having regard to extended due date for filing of original return (31/10/2019) u/s 139(1) of the Act, the assessee is not hit by the provisions of Section 80AC(ii) of the Act. The CPC as well as the Ld. CIT(A) have clearly erred in disallowing assessee’s claim u/s 80P of the Act on the ground that the assessee’s return of income was filed belatedly. Therefore, we set aside the impugned appellate order dated 07/02/2024 of the Ld. CIT(A), and we direct the Assessing Officer to allow the deduction u/s 80P of the Act to the assessee in accordance with law. The grounds of appeal are treated as disposed of in accordance with aforesaid direction.

(D.3) Learned Sr. D.R. for Revenue relied on the aforesaid impugned appellate order of the learned CIT(A).

(E) After perusal of the records and hearing the representatives of both the sides, it is found that undisputedly there was delay of 4 days in filing of the appeal by the appellant assessee in the office of the learned CIT(A). However, the learned CIT(A) has erroneously observed that the delay was of 551 days. In view of the foregoing, the impugned appellate order dated 11/03/2024 of the learned CIT(A) is set aside and he is directed to pass fresh order in accordance with law on the issue of assessee’s request for condonation of delay. For this purpose the learned CIT(A) is directed to respectfully follow the aforesaid order dated 10/01/2022 of Hon’ble Supreme Court. Further if the learned CIT(A) deems it proper to condone the delay on the part of the assessee in filing of the appeal in the office of the learned CIT(A), then the CIT(A) is further directed to decide the assessee’s appeal on merits. While deciding the appeal of the assessee on merits, if such a situation arises, the learned CIT(A) is further directed to give due consideration to decided precedents in the case of Income Tax Appellate Tribunal, which, as contended by the assessee, squarely covers the issue in dispute on merit in favour of the assessee.

(F) In the result, the appeal is partly allowed for statistical purposes.

(Order pronounced in the open court on 02/01/2025)