The New Income-Tax Bill 2025 seeks to modernize and simplify the current tax framework, replacing the Income-Tax Act, 1961, which has undergone over 4000 amendments since its inception. This initiative addresses issues like bulky language, outdated provisions, and extensive cross-references, making the law concise and user-friendly. The Bill reduces its size by half through the removal of over 2100 provisos and explanations and redundant provisions. Clearer drafting styles, simplified references, and extensive use of tables enhance readability and usability. Provisions like “previous year” and “assessment year” have been replaced with straightforward terms, resolving compliance challenges. Stakeholder consultations played a crucial role, with over 20,000 suggestions analyzed and integrated. The exercise also drew insights from global tax law simplifications in the UK and Australia. More than 60,000 man-hours were dedicated to consolidating, vetting, and finalizing the Bill. Notable structural changes include consolidating provisions for non-profit organizations and adopting tabular formats for key sections like TDS provisions. By integrating clarity, ease of interpretation, and tax certainty, the new Bill aligns with evolving economic realities and global best practices.

Also Read:

Govt released Income-Tax Bill, 2025 (Download)

New Income Tax Bill 2025: FAQs on Key Changes

New Income-Tax Bill 2025: Section Mapping & Updates

Income Tax Bill 2025: Executive Summary on Income Tax Act Simplification

FAQs on the New Income Tax Bill 2025

I. Broad scope of new Income-tax Bill

Answers to Frequently Asked Questions

Q I.1 When was the current Income-tax Act passed?

Ans: The current Income-tax Act was enacted in 1961 and came into existence with effect from 01.04.1962. It has been amended nearly 65 times with more than 4000 amendments, year on year through Finance Acts, based on the evolving requirements of modifications in taxation policy.

Q I.2 What concerns have been raised regarding the Income-tax Act 1961?

Ans: Tax administrators, practitioners and taxpayers have acknowledged the contribution of the Income-tax Act, 1961 in overall tax governance and economy. However, over the time concerns have also been expressed over the accumulation of amendments, the intricate language, detailed provisions, redundancies and the heavy structure of the Income-tax Act.

Q I.3 What are the reasons for regular amendments in the Income Tax Act as against other Acts?

Ans: The Income-tax Act is dynamic legislation requiring regular updating and amendments to reflect the nation’s changing economic, social, and political realities. Criminal and other civil laws do not undergo such frequent updating and amendments whereas the Income-tax Act is regularly updated (on annual basis) to reflect the economic changes, fiscal policies, and government priorities. It, therefore, adapts to changes in the economy, business environments, inflation rates, income sources, and global financial trends. The government has introduced tax reforms to encourage specific sectors of the economy while balancing the same with requirements of revenue collection and widening/deepening of the tax base. Given its direct link to taxation and economic conditions, the Act needs to be more adaptable to reflect shifting economic policies, changing incomes, inflation, and emerging industries. The dynamic nature of the Income-tax Act provides it flexibility to accommodate new economic trends.

Examples:

i. To promote exports, specific provisions such as 80HH, 80HHC were brought into the statute. The same having served intended purpose have been since omitted or made inapplicable after sun set date.

ii. To promote infrastructure development, section 80IA was brought into Income-tax Act, 1961.

iii. Sections 80HHE, 10A and 10AA were introduced for facilitating software exports.

iv. Section 80IAC is yet another example of encouraging the start-ups.

Q I.4 Why has the Income-tax Act 1961, become bulky over time?

Ans: The income tax law has become increasingly bulky over time, with its traditional style of drafting and numerous amendments. The complexity of language in the present Act is a product of different factors. To keep pace with certain legal pronouncements, explanations and provisos were often inserted to clarify legislative intent. Changing taxation priorities also led to introduction of additional text to an otherwise simple provision. Further, certain provisions remained in the statute, despite becoming non-operational, in view of pending claims/issues from earlier years.

Q I.5 What simplification efforts have been made in the past?

Ans: Attempts have been made in the past, including those in 2009 and 2019 for simplification of the Income tax Act. The recommendations from these efforts, as regards policy, have been considered in the amendments carried out from time to time.

Q I.6 Has the present simplification exercise considered international experience of other countries who have undertaken similar exercise?

Ans: Simplification of tax laws has received attention globally. Countries have undertaken similar exercises to enhance clarity and compliance in their taxation laws.

In the UK, the process was carried out during the period 1994 to 2010 for simplifying the language. Before simplification, the UK Income and Corporation Tax Act, 1988 comprised 960 pages. However, after simplification, it was divided into five separate Acts, with their page counts increased, resulting in a more segmented but overall larger body of tax law.

Similarly, Australia underwent a similar process during 1994 to 1997, where simplification of language also resulted in a longer tax code.

These international experiences emphasize the delicate balance between simplification and the need for clear, unambiguous legal language. Drawing from these lessons, effort has been made to focus not just on linguistic simplification but also on structural rationalization.

Q I.7 What is the scope of exercise undertaken for the new Income-tax Bill?

Ans: The Hon’ble Finance Minister in the budget speech in July 2024 stated that the purpose of the comprehensive review of the Income-tax Act, 1961, is to make the Act “concise, lucid, easy to read and understand”.

Q I.8 What ground rules are set for making the existing provisions concise, lucid, easy to read and understand?

Ans: Following ground rules have been considered for simplifying the existing provisions:

i. The Bill proposes to eliminate redundant provisions, reducing its length by nearly half.

ii The drafting style of the new Bill is straightforward and clear, making the provisions easier to understand by incorporating more than 57 tables compared to 18 tables in the Income-tax Act, 1961. Sub-sections and clauses have been used, instead of relying on provisos and explanations for exceptions and carve-outs. This minimises cross-references and conflict by aggregating all applicable provisions related to a single scenario in one place.

iii. All provisos (about 1200) and explanations (about 900) have been removed.

iv. The 1961 Act contains numerous cross-references to sections, sub-sections, clauses, sub-clauses, items, and sub-items, making the provisions challenging to interpret. The new Bill adopts a simplified reference system, allowing provisions to be cited by simply mentioning the section. For instance, section 133 (1)(b)(ii) in the new bill would indicate sub-clause (ii) of clause (b) of sub-section (1) of section 133 in the existing Act. This change makes the Act’s language easier to understand.

v. A significant aspect of the Bill is the elimination of the concepts of ‘previous year’ and ‘assessment year’. Prior to 1989, the concept of ‘previous year’ and ‘assessment year’ had been brought because the taxpayers could have different twelve-month previous years for each source of income. From 1st April 1989, previous year was aligned to a financial year in all cases. However, ‘assessment year’ continued to be used for various proceedings under the Act. Thus, a taxpayer was required to track two different periods, i.e., the ‘previous year’ as well as the ‘assessment year’. This presented difficulties in complying to the provisions of the Act especially for a new taxpayer who had to keep track of ‘previous year’, ‘assessment year’ as well as ‘financial year’.

Q I.9 Whether any consultations have been done with stakeholders, while drafting new bill?

Ans: A comprehensive consultative process was undertaken for the simplification exercise. A total of 20,976 online suggestions for simplification and removal of redundancies were received, analysed and relevant suggestions were categorized into policy-related, language simplification, removal of redundant or obsolete provisions, etc. Meetings with industry and professional associations were held and field-level brainstorming sessions were held within the Income Tax Department, towards this exercise.

At the international level, consultations were held with some of the taxation authorities that had undertaken similar exercise in the recent past, viz. the Australian Tax Office and Treasury, and the UK’s Office of Tax Simplification.

The documents prepared in 2009 and 2019, were also referred, while undertaking the exercise. International and national guidance material such as ‘Drafting Guide for Simplification of Laws’ issued by Legislative Department, Ministry of Law and Justice, was studied for simplification of legal language.

Q I.10 What processes were followed in conducting the simplification exercise?

Ans: In addition to the stakeholder exercise mentioned in Q I.9, suggestions were sought from taxpayers, industry and professional associations, and field level officers of the Department. A committee of around 150 officers of the Department was actively involved in the entire exercise. The Committee prepared the draft text of various chapters, which was meticulously vetted by the Legislative Department of Ministry of Law and Justice, and consolidated in the form of the final Bill, after necessary approvals.

More than 60,000 man-hours were dedicated by the team for finalising the new Bill. Q I.11 How has the readability improved in the new Bill?

Ans: The readability of tax law has been improved by using simpler language, as against traditional legal language. Where multiple situations are covered, the sections have been made enumerative. Wherever feasible, extensive use of table formats has been made. TDS provisions have been presented in a tabular form. Certain provisions such as section 10, which contained about 150 clauses has been placed in Schedules and presented in the form of tables.

As a result of the comprehensive exercise, the size of the new Bill has reduced by about half on one hand and one the other, the provisions have been consolidated and presented in a user-friendly format.

QI.12 What is the treatment of numerous ‘provisos’ and ‘explanations’ and procedural aspects in the existing Act?

Ans: Provisos (more than 1200) and Explanations (more than 900) have been removed, with their simplified content placed as sub-sections or clauses. Wherever feasible, procedural aspects and specific details are proposed to be provided by way of Rules.

QI.13 Have the redundant provisions of the Income-tax Act 1961 been removed in the new Income-tax Bill?

Ans: Yes. Certain provisions became redundant due to numerous amendments and/or policy changes over the years. This resulted in large number of such provisions in the Act. For example, deduction under section 10A, which was a special provision for newly established industrial undertakings in the free trade zones, is no longer available from the Assessment Year 2012-13, onwards. Such obsolete provisions have been removed from the text of the Bill. However, provisions applicable to earlier Assessment Years shall be governed by Repeal and Savings provisions.

QI.14 What other steps have been taken to enhance clarity in the new Bill?

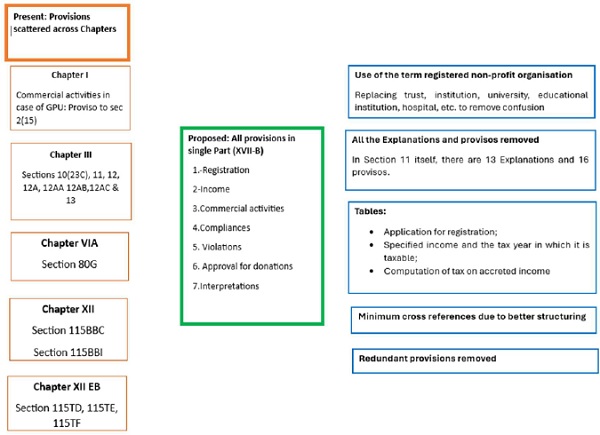

Ans: In addition to removal of ‘provisos’, ‘explanation’ and redundant provisions, formulae, tables, and structures have been used to enhance clarity in the new bill. To the extent possible, provisions involving the same issues, which were present in different chapters in the current Act, have now been consolidated. Redundancy has been removed and definitions at multiple places have been consolidated.

In case of provisions relating to Non-Profit organisations (NPOs), the entire text related to NPOs has been consolidated and structured into 7 sub-parts which contain provisions related to Registration, Income, Commercial activities, Compliances, Violations, Registrations for the purposes of eligibility of donations and Interpretations.

QI.15 How have principles of Tax Certainty followed in drafting of the new Income Tax Bill?

Ans: The new Income-tax Bill is approximately half the length of the existing Income-tax Act 1961, with significant re-organisation of provisions in different sections. While undertaking simplification exercise, a conscious attempt has been made to minimise the scope of litigation and fresh interpretations. For this purpose:

a. Key words/phrases, especially where courts have given rulings, have been retained with minimal modifications.

b. Language has been simplified by use of short sentences to the extent possible.

c. Sections have been translated into row or sub-rows in tables, reducing the number of words and bringing clarity.

d. Provisions have been made clear to minimize scope for multiple interpretations. The provisos and explanations have been removed and simplified content has been placed as sub-sections and clauses.

e. Provisions related to international taxation have been dealt with, broadly, to ensure tax certainty.

f. NGO chapter has been made more comprehensive with use of plain language.

g. Exemption sections, for example section 10 in the present Act, has been made simpler through tables and placing large number of provisions in Schedules.

h. Formulae and tables have been used to enhance clarity, wherever feasible.

i. Provisions involving same issues and definitions, which were present in different chapters in the existing Act have been consolidated, to the extent possible.

QI.16 How does the new Bill compare to the Income-tax Act, 1961 in terms of numbers of Chapters, sections and words?

Ans: There has been a significant reduction in the text of new Bill, in comparison to the existing Income Tax Act, as summarised below.

| Particulars | Income-tax Act, 1961 | The proposed Act |

| Chapters | 47 | 23 |

| Sections | 819* | 536 |

| Words | 5.12 lakhs | 2.60 lakhs |

* Effective Sections

Besides about 1200 Provisos and 900 Explanations have been removed.

QI.17 What is the basis of the statement that the Income tax Act, 1961 consists of 819 sections, while the text of the Act only mentions sections till 298?

Ans: During the course of numerous amendments to the Income tax Act, 1961, several policy decisions were incorporated as separate provisions. Many a times such provisions were connected to already existing sections and accordingly the new sections were numbered in continuation to the existing sections. For example, several provisions relating to tax on special cases were inserted as sections starting with 115 series viz 115 AC,115AD, 115JB, 115VP etc. As a result of such insertions, effective sections existing in the Income tax Act, 1961 are 819.

Q I.18 Why does the new Bill still contain 536 sections and 2.6 lakh words?

Ans: While the existing Income-tax Act contains 298 numbered sections, effective sections in the current Act are 819. This is because other than numeric section numbers there are large number of sections with alpha-numeric codes such as 115A to 115WM (117 sections) and so on. The Income-tax Act not only deals with levy of tax but it is a comprehensive document, which encompasses all aspects of tax administration. It also includes other aspects such as:

(a) laying down the administrative framework, assigning roles and responsibilities for assessing officers, taxpayers, tax deductors, and professionals etc;

(b) setting out the framework for income determination, timelines, appellate procedures, enforcement, assessments, and penalties; and

(c) taking into account the impact of interpretations on economic policy, affecting both domestic and international investments.

The new Bill proposes 536 sections to meet the above-mentioned requirements. Further, several sections in the new Bill exist primarily to honour the commitments under the existing tax regime, including provisions relating to Minimum Alternate Tax (MAT), various deductions and exemptions, etc. These provisions will remain in force until their respective sunset clauses take effect. Therefore, these are required to be part of new Bill to ensure a smooth transition, while maintaining legal and policy continuity.

QI.19 Whether the simplification exercise has led to no ‘material’ change? Ans: The simplification exercise, inter-alia, encompasses following aspects:

i. Redundant provisions of the Income tax Act have been removed;

ii. Sub-sections and clauses have been used, instead of relying on provisos and explanations for exceptions and carve-outs;

iii. Simplified system for cross referencing of sections, sub-sections, clauses etc has been used;

iv. Extensive use of tables, formulae for enhanced clarity;

v. Consolidation of provisions scattered across various sections/ Chapters relating to a single issue; etc

Since there have been regular amendments to the Income Tax Act, 1961 including amendments proposed in Finance Bill, 2025, the Act stands updated from policy perspective. All amendments proposed upto Finance Bill 2025 have been duly incorporated in the new Income tax bill 2025. Therefore, while no major policy related changes have been made in the Bill, the above aspects have led to proposed ‘material’ changes in the existing law.

QI.20 Whether any mapping of old and new sections will be available?

Ans: Section-wise mapping will be made available on the official website of the Income Tax Department.

QI.21 How has ‘previous year’ and ‘assessment year’ been dealt with in the new bill?

Ans: The concept of ‘tax year’ has been introduced replacing ‘previous year’ and ‘assessment year’. The timelines and computation in the Bill are now with reference to the financial year for which the income is liable to be taxed. It is expected that the use of ‘tax year’ will make the new Bill easier to comprehend. Further, many of the comparable tax jurisdictions in the world are using one single term, for purpose of denoting the unit period of taxation. ‘Tax year’ is commonly used in many countries.

With the introduction of ‘tax year’, broadly the following principles have been adopted:

i. ‘Tax Year’: Unit period of taxation. This term shall be referred in respect of all transactions and income for that period.

ii. ‘Financial Year’: For purposes of timelines for compliance and for procedural issues.

QI.22 How have the provisions of TDS and TCS been simplified in the new bill?

Ans: TDS and TCS provisions have been made easier to comprehend by providing tables. There are separate tables for payment to residents and non-residents, and where no deduction at source is required. For example, the proposed provisions relating to TDS on rent are shown below:

| 2. | Rent | ||

| S. No. | Nature of Income or sum | Payer | Rate |

| Threshold limit | |||

| (i) | Income by way of rent | Person other than specified person | Rate: 2% |

| Threshold limit:

Rs. 50,000 for a month or part of a month |

|||

(Reference can be made to Table in proposed section 393 of the Bill)

QI.23 What has been done to simplify the provisions related to Non-Profit Organizations?

Ans: The provisions related to Non-Profit Organizations were present at different places in the existing Act, in section 11, section 12, section 12A, section 12AA, section 12AB, section 13, section 115BBC, section 115BBI, section 115TD, section 115TE, section 115TF. The provisions related to approval are under the first and second proviso to section 80G (5). These have been simplified and consolidated into one chapter. All the provisions related to registered Non-Profit Organisations have now been arranged in Part B of Chapter XVII titled “B.–– Special Provisions for Registered Non-Profit Organisation” in the new Bill.

QI.24 What simplification has been carried out for salaried employees in the new bill?

Ans: All the provisions pertaining to salary have been consolidated at one place for ease of understanding so that the taxpayer does not have to refer to separate chapters for filing his return of income. The deductions which were earlier allowed under section 10 of the Income Tax Act,1961, like gratuity, leave encashment, commutation of pension, compensation on VRS and retrenchment compensation, are now part of the salary chapter itself. Some of the allowances like HRA are now provided in Schedule II of the new Bill that finds reference in the provisions relating to salary. The objective was to improve readability by way of providing tables and formulas.

While the chargeability of all the perquisites has been retained in the Act, their valuation, conditions and exceptions have been shifted to Rules as they do not affect every taxpayer. Similarly, redundant and repetitive provisions have also been removed for better readability.

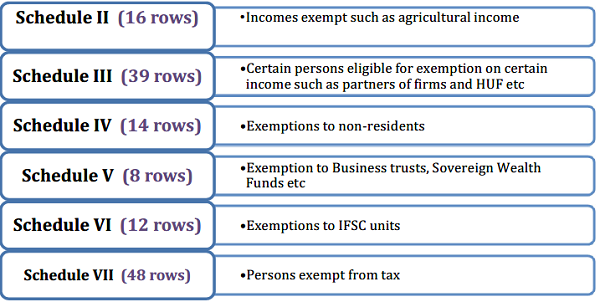

QI.25 What changes are being made to exemptions for specific incomes and persons?

Ans: Provisions relating to exemptions for specific incomes and persons are being moved to separate schedules for easier reference and simpler compliance as follows:

example of the Schedules is given

An example of the Schedules is given below:

| Sl. No. | Eligible persons | Conditions |

| A | B | C |

| 1. | Any regimental Fund or non-public Fund established by the armed forces of the Union | Such Fund is for the welfare of the past and present members of the armed forces or their dependants. |

(References to Schedules has been made in section 11 of the Bill)

QI.26 What are the next steps after the new Bill is introduced?

Ans: Stage 1: Bill is passed by the Parliament and becomes an Act

Stage 2: Operational and delegated legislation framework

i. Notification of new Rules and Forms.

ii. Simultaneous exercise of software development to set up the systems and processes for various administrative and quasi-judicial functions.

QI.27 How will the old and new provisions co-exist?

Ans: Various facets of compliance for the respective years have been mentioned in the Repeals and Savings clause in the Bill, which will safeguard all rights and liabilities accrued under the old law.

QI.28 What are the changes on rates and other policy in the new bill?

Ans: There are no changes related to rates. Since there have been regular amendments to the Income Tax Act, 1961 including amendments proposed in Finance Bill, 2025, the Act stands updated from policy perspective. All amendments proposed upto Finance Bill 2025 have been duly incorporated in the new Income tax bill 2025. Therefore, while no major policy related changes have been made in the Bill, the above aspects have led to proposed ‘material’ changes in the existing law.

QI.29 Why is it that on comparison of new Income Tax Bill and earlier provisions, it is found that in some cases viz ‘virtual digital assets’, etc there are certain changes?

Ans: The Income Tax Bill 2025 also contains all amendments proposed in Finance Bill 2025. Therefore, the users are advised to compare the provisions of the Income Tax Act, 1961, as updated with proposed amendments in Finance bill 2025, while reading the Income Tax Bill, 2025. There is, therefore, no change in the scope of ‘virtual digital asset’ under the Income Tax Bill, 2025. The definition under the Bill incorporates the amendment already proposed under the Finance Bill, 2025.

QI.30 Which Chapters of the Income tax Act, 1961 have seen large reduction of words, as a result of the simplification exercise?

Ans: As noted above, the total words in the new Income Tax Bill, 2025 are around 2.6 lakhs, as against 5.12 lakh words in the Income Tax Act, 1961. Some of the Chapters where substantial reduction of words have been achieved are as given below:

| Income Tax Act, 1961 | Income Tax Bill, 2025 | Reduction of words | ||

| Topic | Words | Topic | Words | |

| Exemption related provision | 30000 | Exemption related provisions | 13500 | 16500 |

| TDS/TCS | 27453 | TDS/TCS | 14606 | 12847 |

| Non-profit Organization | 12800 | Non-profit Organization | 7600 | 5200 |