RECENT AMENDMENTS TO SEBI (LODR) REGULATIONS: KEY HIGHLIGHTS FROM CIRCULAR NO. SEBI/HO/CFD-POD-2/CIR/P/2024/185 DATED 31ST DECEMBER 2024

On the recommendation of the Expert Committee, SEBI, through its circular dated 31st December 2024, introduced measures to enhance and simplify compliance requirements for listed entities. The circular implements integrated filing for governance and financial disclosures with revised timelines, aimed at facilitating ease of doing business.

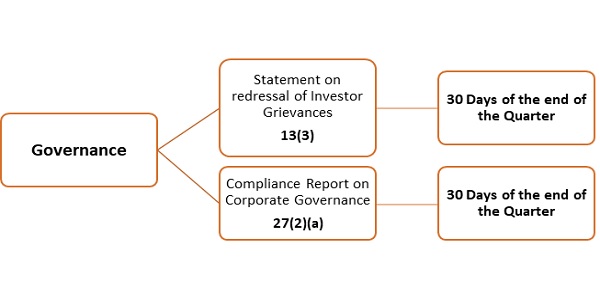

Governance Filings:

- Investor Grievance Statements (Regulation 13(3)) and Corporate Governance Compliance Reports (Regulation 27(2)(a)) must now be submitted within 30 days post-quarter-end.

- Additional disclosures include updates on changes in share acquisition, minor penalties, and tax litigation matters.

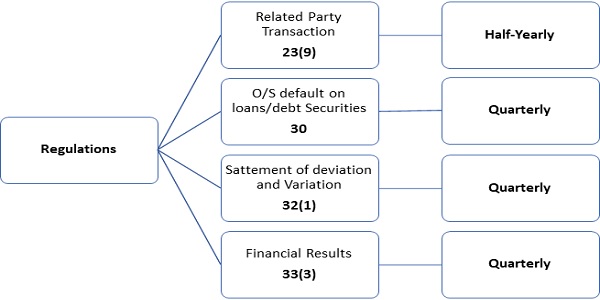

Financial Filings:

- Key financial disclosures include:

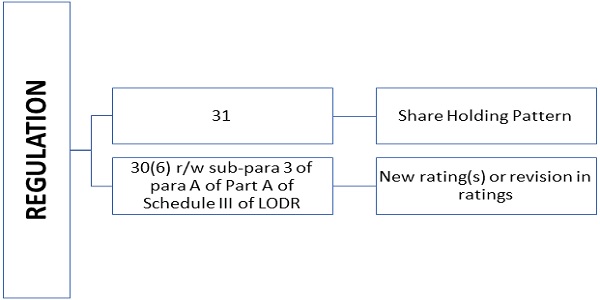

- Related Party Transactions (Regulation 23(9)),

- Loan Defaults (Regulation 30),

- Deviation Statements (Regulation 32(1)),

- Financial Results (Regulation 33(3)).

NOTE:

An extension has been granted for filing the first quarterly integrated report comprising Governance and Financials for the quarter ended December 31, 2024. Entities may now submit the integrated filings within an extended timeline of 45 days from the end of the quarter, i.e., by February 14, 2025. This relaxation aims to provide entities with additional time to ensure accurate and comprehensive compliance.

The circular further redefines the role and responsibilities of secretarial auditors. It mandates shareholder approval for their appointment and introduces new eligibility criteria, including disqualifications.

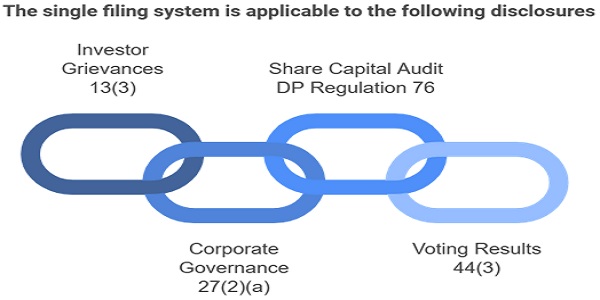

THE FOLLOWING DISCLOSURES ARE NOW UNIFIED UNDER GOVERNANCE FILINGS

In addition, the following information must be disclosed on a quarterly basis as part of the Integrated Governance Filing:

THE FOLLOWING FILINGS HAVE BEEN CONSOLIDATED UNDER FINANCIALS:

SINGLE FILING SYSTEM

The single filing system applies to entities listed on both stock exchanges, namely BSE and NSE. With effect from October 18, 2024, listed entities are no longer required to submit the same disclosure separately on both exchanges. Instead, they have the option to file disclosures and any revisions exclusively on either exchange, ensuring a more efficient compliance process.

SYSTEM DRIVEN DISCLOSURE

The manual filing of the following disclosure is not necessary. Instead, the disclosure will be automatically generated by the stock exchange.

CHANGES IN DISCLOSURE FORMATS

| Sl.No | Regulation | Changes in format |

| 1 | 27(2)(a)- Corporate Governance | Quarterly

1. Composition of Board of Directors 2. Composition of Committee 3. Meeting of Board of Directors 4. Meeting of Board of Directors 5. Meeting of Committees 6. Affirmations 7. Investor Grievances Redressal Report 8. Disclosure of Acquisition of Share or Voting Rights in Unlisted Companies 9. Disclosure of Imposition of Fine or Penalty 10. Disclosure of updates to ongoing Tax Litigations or Disputes |

| Half-Yearly

1. All the above disclosures 2. Disclosures of Loans/Guarantees 3. Affirmations on Compliance Requirements for AGM |

||

| Annual

1. All Quarterly disclosures 2. Disclosures of Loans/Guarantees 3. Website Affirmations 4. Affirmations w.r.t Compliance with Corporate Governance Provisions |

||

| 2 | 33(3) – Financial Results | Quarterly

1. Quarterly Financial Results 2. Statement of deviation or variation 3. Disclosure of outstanding default on loans and Debt Securities 4. Disclosure of Related Party Transaction |

| Half-yearly

1. Half-yearly financial Results 2. Statement of deviation or variation 3. Disclosure of outstanding default on loans and Debt Securities 4. Disclosure of Related Party Transaction |

||

| 3 | Annually

1. Annual Audited financial 2. Statement of deviation or variation 3. Disclosure of outstanding default on loans and Debt Securities 4. Disclosure of Related Party Transaction 5. Statement on Impact of Audit Qualifications |

DISQUALIFICATIONS ADDED REGARDING THE APPOINTMENT OR CONTINUATION OF A SECRETARIAL AUDITOR IN THE LISTED ENTITY

SERVICES THAT SHOULD NOT BE RENDERED BY THE SECRETARIAL AUDITOR.

Author Bio