As I already stated in my introductory part of this topic, any process will be parted into static and strategic meaning thereby one which is in as it is form and the other requires professional skepticism. Above that, static facts w.r.t. terminologies are also tuned here. Let us sail beyond statutory sections sight u/s 134, 143,177 of Companies Act, 2013 by carving into crux of Inventory & Scrap process.

Draft design depicted as: –

- Radical round

- Strata static sphere

- Material math and mix with money

- Radical Round

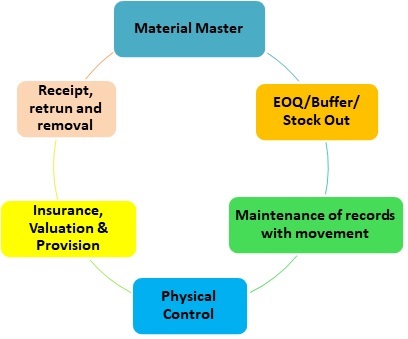

Inventory ink incept at the point when material master is maintained to identify a product as part of inventory. We are taking about the one used primarily in connection with the business. Basically, balance sheet current asset component. Material master then moves towards requirement of minimum, maximum and various in-built threshold for component. Maintaining detail records of each stage including inter transfers, subcontract or job work takes step ahead. Physical controls couped with CARO requirements refined with provisions and valuations are carried till sales visa viz return-receipt match.

- Strata-Static Sphere

Consists of following: –

1. SOP

2. System Strength

3. Re-order review

4. Complete record

5. Physical Controls

6. Insurance & Valuation

7. Receipt, return and removal

1) SOP

SOP of inventory may be broken into two parts one which explains movement it enters at ground level and other its treatment in books. Static aspects related to SOD /DOA to be obtained via matrix. Creation-modification-deletion ought to be defined and in-sink with person in system. Process path to be perceived peacefully. Any industry if we start then there needs to be complete flow in cost sheet as well as work papers which helps in designing controls or identifying any gaps while testing test of design or test of operative effectiveness. Compliance with applicable AS/Ind As , cashflow statement , working capital requirements and other applicable framework at each stage be segregated and cross linked with completeness.

“Static and strategic share of SOP in sync with system sights the show as scheduled”

2) System Strength

System strength stirs the sight of inventory process in substantive audit procedure.

E.g 1) Finished Goods marked as non-moving and raw material ordered for the same! Backward integration at each stage of movement is must. How good my system controls are to restrict/block this raw material order?

2) WIP rejected by quality transferred to reclass like B/C category or moved as scrap sale? How good are my real time track of movements?

“Reclassification risk be redressed on real-time in sync with system, else ends with reconciliation”

3) Re-order level review

Supply chain management mingle at this stage is a surety check. Defining a re-order basically to mitigate risk of non-fulfillment of demand and reviewing it on timely manner marks stock out situation stunted. Procure to pay process also plays pivotal role in evaluating re-order.

“Review at right time redresses re-order level at required rate”

4) Complete Record

Accurate master maintenance is a must. Any system comes with complete bundle but when bucketed for use, some of them still untouched/ unexecuted!

Record keeping and testing its accuracy after inputs of applicable scenarios marks movement track minutely.

E.g. A dummy record to by-pass any stage like quality, quantity order in excess of stock permit, marking of inter transfer instead of job work, etc. In nutshell, any situation where probability of inherent risk is involved with maximum manual intervention is likely to be tested.

Sub-contract & job work junctions are to be evaluated as an integral /non- integral part of process and accordingly in records. Any breaks at this point paves path towards debit/credit notes along with balance confirmations chaos.

Records are lifeline of any process. “Re-drafting records Vs retrieving it in a refined way revamps records”

5) Physical Controls

CARO requirements, perpetual audits and all are of essence. What makes this aspect alive is observation. Visit a unit/store/factory and then only perform a test of design or control effectiveness.

E.g. A 3rd party storage facility visit. At documentation level, contract reading and noting of agreed terms like tolerance for loss units, reporting frequency, surprise checks, etc forms essential part of checklist. It starts with racks system, FIFO/LIFO movement, CCTV, security check, inward and outward movements, insurance, access to facilities, SKU level scans, stickers, packing materials, markings/boards, records, compliance and display boards, IT check to determine activities performed by bots, manual or semi-automated modes from pre-check in to post-check out of inventory.

Physical control check performed by verifying physical audit report Vs books of accounts and treatment of variance is just a post-mortem of a transaction. It is to be done as part of work papers, but difference lies in identifying instances in-person.

E.g. There was mis- management of single item for bulk order packaging; not total miss out but wrong placing of one box instead of correct one. Reason found “lighting & board”. Product supposed to be picked up and the one which was picked when reflects with yellow light placed above it, ought to pick wrong ones. White light and demarcation board eased out repeated mismatches.

“Physical controls curated with checks and concluded with cautious call comply with CARO requirement in real sense.”

6) Insurance, Valuation, and provisions

Insurance already covered in my IFC processes. Generally, 10 -20% buffer or as per industry need its taken more but empirical to ensure no short insurance by analyzing instances invoked and claims settled. Valuation of inventory applying prudence provisions point and if done by 3rd party then any deviation from the report Vs books of accounts be justified by assumptions, rates or any other aspect of applicable framework. Committees if any for inventory related aspect, its recommendations and minutes be minted minutely.

“A prudence procedure backed by valuation & integrated with insurance inclines with Ind AS/AS “

7) Receipt, return and removal

Receipt of goods from job worker/sub-contractor; return of goods with defect/replacement or refund route and removal of goods with respect to scrap or sending as by-product/sub-process. Revenue assurance and leakage at this stage is steadfast.

E.g. Return and refund process for bulk order if not passed by various department on time, ought to be adjusted in next order; which will ultimately fall within the limit of particular debtor being key account. Books to be adjusted with less recovery and inventory movement either in scrap or in spined out.

Thus, internal, and external parties to return, receipt and removal be clearly demarcated to record regular reversal or inter transfer treatment in books.

Talking about removal rides way to scrap sale. Though it might contribute a single digit percent of total sale, sea sight is to be sought. Based on nature of transaction and total components in scrap or wastage it may form a separate process as part of IFC report.

“Re-connecting dots with the help of receipt, return and removal of inventory reveals a realistic review”

- Material math and mix with money module

Can be mingled in following situations: –

1) Material math ought to match in preparation of stock statement based on which fund-based credit requirements are fulfilled. Any variance may impact drawing power.

2) Order management movement manipulation may lead to mismatches in money math.

- E. g. (A)Loss within defined limit -say 5% irrespective of fact that product can be capped within 1% range!

- (B) For consumable products, wastage way (segregated product instead of final consumable) adopted avoiding consumption leading to loss of sale and pocketing.

- © Trading stock trace- It’s tie-up in the system, requirement and inclusion in final product or as non-integral part be perceived properly.

Material math for listed company is colossal core. Monetary aspect involved makes it more prone to risk. In nutshell, robust system controls aligned with insurance ink, in transit traced through cross border and domestic logistic link, supplied safe with storage sink sights surety sale sync in the system.

Author Bio