As I already stated in my introductory part of this topic, any process will be parted into static and strategic meaning thereby one which is in as it is form and the other requires professional skepticism. Above that, static facts w.r.t. terminologies are also tuned here. Let us sail beyond statutory sections sight u/s 134, 143,177 of Companies Act, 2013 by carving into crux of Property, plant & equipment process.

Also Read-

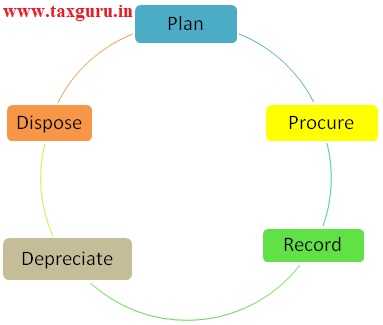

Draft design depicted as:-

- Radical round

- Statutory Stall

- Strata-static sphere

- Disposal desk

# Radical Round

Procurement and planning phase pertains to already perceived path in P2P.Recording requires “ready to use” reference (AS/Ind AS).Depreciation deals with dual requirement under Companies Act, 2013 and Income Tax Act, 1961.Disposal digs deep till divergent dignitaries desk (For licenses in case of any hazardous waste).

# Statutory Stall

Break the chain! I am talking about my own structure to set these series, which stands smashed by starting with” statutory stall”. What it is and why a starting stroke? As name suggests, its synopsis of statutory areas this process incorporates. Because here we are talking about listed companies, a single sight aside surely sinks us; hence it should be starting point.

Simple step of opening balance builds our basic bond. How? From latest published annual report. It is only by reading between the lines, one leads to light lamp of “the applicable framework”. List may include:-

1. Indian Accounting Standards (Ind AS)—Based on Phase Company falls.

| Ref No | Particulars |

| 7 | Statement of cash flows |

| 16 | Property ,plant and equipment |

| 17 | Leases |

| 20 | Accounting for Govt grant & disclosure of Govt Assistance |

| 21 | Effect of change in foreign exchange rates |

| 23 | Borrowing costs |

| 36 | Impairment of assets |

| 38 | Intangible Assets |

| 40 | Investment property |

2. Companies Act 2013 sections

Sec 123 read with Schedule II

3. CARO 2016 as CARO 2020 w.e.f. 01/04/2021

# Strata- Static Sphere

- Sync with strata-static sphere

Sailing through statutory sections with strata static sphere:

Cash flow statement

Investing activities and loss/gain gaze gives gist of data to create control activities and draft RACMs.

Jumble Jar of Ind-AS

Let’s take one example to cover crux of other IndAS , obviously by remembering radium as Ind AS 16.

E.g. Asset is imported with terms of trial or return basis within 2 months. Flow of transaction task:-

Duty payment on entering India

⇓

Factory gate inward in Units FAR, yet to be entered in BOA

⇓

Installation certificate, commercial production, put to use at the end of 2 months.

⇓

Recognition in BOA after dissecting capitalization and allied aspects.

⇓

Application to bank for borrowing and inclusion of asset in FAR, Insurance inclined.

⇓

Impairment study, forex gain/loss, depreciation drive at financial year closure.

Just imagine immense involvement of all departments from above example; it’s insistent.

Apart from above, any asset which already qualified for subsidy and no more subsidy is receivable at time one conducts IFC, we can’t take risk to remove that aspect under shelter of not applicable or not received during financial year, but do take cognition of deferment demeanor. Jumble jar of Ind AS to be justified judiciously.

Company’s Act sections

Depreciation dealings, useful life and learning’s. Notes to accounts and balance sheet blocks builds base to comply with this section.

CARO 2016,Upcoming 2020

Physical verification of assets stands as paramount part. This signifies sync between factory gates to books date (recognition in BOA). Variance way would also be viewed w.r.t. physical verification vs. fixed asset register (FAR).

- SOP

This document is something that sets the static-strategic pace of any process persisting. Sequenced sail may begin by:-

Budget, agreements, on-boarding vendor, logistic, tagging of asset, recognition in BOA, disposal , DOA , SOD and it finally ends by sign-off as per approval matrix with validity date.

- Capital work in progress

Transfer and monitor of CWIP to respective category in FAR or in WIP code can be carried out.

- Intangibles, Merger & Acquisitions & Valuations

There are standard ways well defined in Ind-AS to deal with aforesaid aspects which are of intrinsic value to worth it.

- Financial year cut

Depreciation being dual demanding drives dominating along with disposal, capitalization and allied areas which acquires assent approach at year end.

- System sensitivity

Static strokes already discussed in P2P like creation, alteration and deletion. Apart from that view vision is also a variety. 1st point is “Sequence square” w.r.t. tagging/barcoding of assets seeks substantiality. FAR being focal point of PPE process finds its way from system, hence even minute aspect assigns attention. It means sample for sequential aspect ought to be substantively sorted out. 2nd point is “Linkages” with FAR i.e. FA balance in FAR reconciles with general ledger .This linkage liaisons with ANY processes is indispensible.

# Disposal desk

Density of this process might be more towards tangible assets. These parameters are even part of one of the potential areas pinching PBT.Disposal desk be drafted as,

“Cognizability curve from put to use till discard through books via business boosts” (Knowledge of client business)

Author Bio