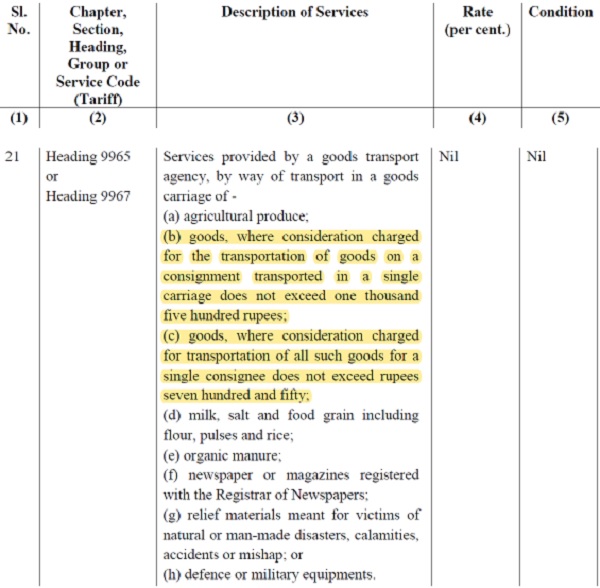

A) Removal of certain Exemptions related to services of transportation of goods by a Goods Transport Agency (GTA):

Notification No. 04/2022- Central Tax (Rate) dated 13.7.2022 amends service exemption Notification 12/2017- Central Tax (Rate) dated 28.6.2017 and removes exemption as provided against Serial No. 21, in column (3), Clauses (b) and (c). The abovementioned Entry is reproduced hereunder:

Source: Extract of Notification 12/2017- Central Tax (Rate) dated 28.6.2017

Interpretation and analysis:

Now, with effect from 18.7.2022, exemption has been withdrawn on the abovementioned highlighted entries, namely, on transportation of goods on road by a Goods Transport Agency (GTA) where, (1) the consideration charged on transportation of goods in a single carriage of GTA does not exceed Rs. 1500, and (2) the consideration charged for transportation of all goods for a single consignee does not exceed Rs. 750. Therefore, from now on, services of transportation of goods by a GTA on road of any amount shall attract GST apart from the specified cases of exemptions as provided in Entry 21, clause nos. (a), (d), (e), (f), (g), (h).

(B) Amendments in Tax rates on transportation services by GTA and option available for GTA to exercise payment of output tax under Forward Charge Mechanism or Reverse Charge Mechanism for every Financial Year:

Notification No. 03/2022- Central tax (Rate) dated 13.7.2022 has made amendments to Notification No. 11/2017- Central Tax (Rate) dated 28.6.2017. The amendments in relation to tax rates applicable on services of transportation of goods by a Goods Transport Agency by road have been discussed hereunder:

Kindly find the relevant extract of the amendments in relation to Goods Transport Agency as per Notification 03/2022- Central Tax (Rate) dated 13.7.2022 as hereunder:

Source: Extract from Notification No. 03/2022- Central tax (Rate) dated 13.7.2022

Interpretation and analysis:

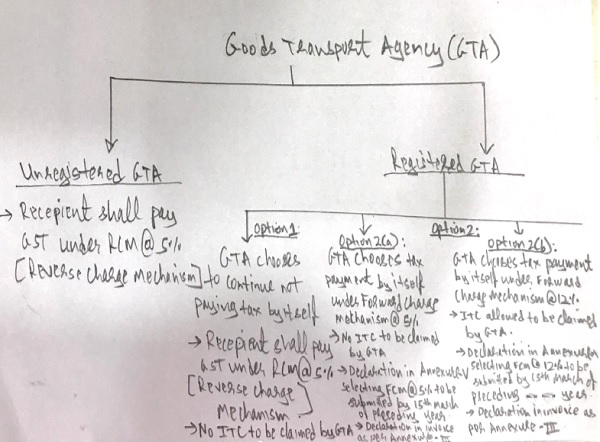

(1) GTA has option to itself pay GST or not (RCM): With effect from 18.7.2022, Goods Transport Agency (GTA) shall be provided with options to pay GST under Forward Charge Mechanism (FCM) with the option that the GTA, (1) (a) may itself pay output tax on transportation services @ 2.5% each under CGST Act and SGST Act with the condition that it does not claim Input Tax Credit (ITC) on the goods and services used in supplying the transport service, or has the option that the GTA, (1)(b) may itself pay output tax on transportation services @ 6% each under CGST Act and SGST Act and may claim ITC on the goods and services used in supplying the transport service.

(2) The GTA may exercise payment of GST on transport services under Forward Charge Mechanism (FCM) i.e. pay the output tax itself, by making a declaration in Annexure-V on or before 15th March of the preceding year. Annexure-V shall be made available on the GST Portal soon. For example: For exercising the option to pay output tax under FCM for F.Y. 2023-24, the GTA has to submit the declaration in Annexure-V stating the same latest by 15.3.2023.

(3) However, a GTA has the option to select FCM method of payment of output tax for Y. 2022-23 by submitting Annexure-V by 16th August, 2022.

(4) It is to be noted that this option once exercised shall not be allowed to be changed within a period of one year from the date of exercising the option and will remain valid till the end of the financial year for which it is exercised.

(5) lThe GTA is allowed to issue tax invoices and make tax payments @ 5% or 12% under Forward Charge Mechanism (FCM) on the goods transportation service for the period from 18th July, 2022 to 16th August, 2022 before exercising the option to opt for such payment of tax under FCM for the financial year 2022-2023 but in such a case the supplier GTA shall have to exercise such an option to pay GST on its supplies on or before the 16th August, 2022.

(6) Kindly note that in case the GTA wishes to continue not paying output tax itself on the transportation services provided, he may continue to remain as such and the recipient of service shall pay such output tax under Reverse Charge Mechanism @ 2.5% each under CGST Act and SGST Act. Here, the GTA shall not be allowed to claim the ITC on the goods and services used to provide such transportation services. However, in case the recipient of transportation of service of goods by a Goods Transport Agency (GTA) has paid tax of such a service under Reverse Charge Mechanism (RCM), such recipient of supply is eligible to claim Input Tax Credit on such tax paid.

(7) The following flowchart explains the various options available in the hands of a Goods transport agency in payment of tax, tax rates applicable and conditions applicable therewith:

Source: Self

(8) The format of Annexure–V as abovementioned is provided hereunder:

“Annexure V

FORM

Form for exercising the option by a Goods Transport Agency (GTA) for payment of GST on the GTA services supplied by him under forward charge before the commencement of any financial year to be submitted before the jurisdictional GST Authority.

Reference No.-

Date: –

I/We_________________________ (name of Person), authorised representative of M/s…………. have taken registration/have applied for registration and do hereby undertake to pay GST on the GTA services in relation to transportation of goods supplied by us during the financial year under forward charge in accordance with section 9(1) of the CGST Act, 2017 and to comply with all the provisions of the CGST Act, 2017 as they apply to a person liable for paying the tax in relation to supply of any goods or services or both;

I understand that this option once exercised shall not be allowed to be changed within a period of one year from the date of exercising the option and will remain valid till the end of the financial year for which it is exercised.

Legal Name: –

GSTIN: –

PAN No.

Signature of Authorised representative:

Name of Authorised Signatory:

(9) Full Address of GTA:

Source: Extract of Notification No. 03/2022– Central Tax (Rate) dated 13.7.2022

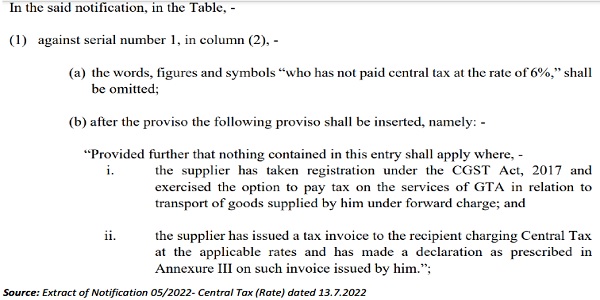

(C) Changes in invoicing for services of transportation of goods by Goods Transport Agency (GTA):

Notification 05/2022- Central Tax (Rate) dated 13.7.2022 has amended Entry No.1 of Notification No. 13/2017 – Central Tax (Rate) dated 28.6.2017 and has eliminated “[who has not paid Union territory tax at the rate of 6%]” and replaced it with the following entries (i) and(ii). Kindly find the relevant extract of the amendments related to GTA in Notification 05/2022- Central Tax (Rate) dated 13.7.2022 as hereunder:

Interpretation and analysis:

(1) Any registered GTA opting for payment of output tax under Forward Charge Mechanism i.e. payment of tax by itself, shall comply with the following conditions:

(a) Should be registered under GST as a Goods Transport Agency,

(b) Should have submitted a declaration mentioning opting for payment of tax under FCM in Annexure-V on or before 15th March of the preceding year.

(c) Should issue a tax invoice with either 5% or 12% GST rate to the recipient of the service and make a declaration as prescribed in Annexure-III in every such tax invoice. Kindly find the format of declaration hereunder:

Source: Extract of Notification 05/2022- Central Tax (Rate) dated 13.7.2022

(d) The recipient of transportation of service may claim Input Tax Credit on the basis of the tax invoice issued by the GTA, under Forward Charge Mechanism, which may be either 5% or 12% tax rate.

(e) All the relevant amendments as above mentioned vide Notification No. 03/2022- Central Tax (Rate) dated 13.7.2022, Notification No. 04/2022- Central Tax (Rate) dated 13.7.2022, Notification 05/2022- Central Tax (Rate) dated 13.7.2022 shall come into effect from 18.7.2022.

Attachments with highlighted portions are provided for your kind reference as mentioned hereunder:

(1) Notification No. 04/2022- Central Tax (Rate) dated 13.7.2022

(2) Notification 12/2017- Central Tax (Rate) dated 28.6.2017

(3) Notification No. 03/2022- Central tax (Rate) dated 13.7.2022

(4) Notification No. 11/2017- Central Tax (Rate) dated 28.6.2017

(5) Notification 05/2022- Central Tax (Rate) dated 13.7.2022

(6) Notification No. 13/2017 – Central Tax (Rate) dated 28.6.2017

DISCLAIMER: The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon.

Author Bio