Valuation under Income Approach and its preference during COVID-19 times:

The income approach of business valuation is based on the idea of valuing the present value of future benefits. This approach estimates business value by considering the future income accruing over a period of time. There are two major methods that fall under this category which is capitalisation of earning method and discounted cash flow method.

A valuer should consider the subject company’s cash balance and cash usage rate in assessing the company’s ability to continue operations. This also includes assessing changes the company has made to preserve capital during this time period as well as going forward. Doing so will give the valuer a good idea of how long the company may survive under the current situation.

Why is Income Approach Valuation methodology more appropriate during the COVID-19 pandemic?

The Income approach is emphasized to value business in the new COVID-19 age with the use of multiple projection scenario analyses and probability-weighted outcomes. The key in DCF analysis, one of the methods under Income Approach, is the development of projections that reflect COVID-19-related impacts including a subsequent recovery to a point of stability and maturity over the long term. Forecasting and computation of discount rate under DCF analysis require significant judgement on the part of the valuer in tandem with management perspectives as to the company’s long-term outlook. The cash flow projection rationales must be fully documented and shall include the effect of all relevant economic, industry, and company specific factors, as affected by COVID-19, and as known or knowable as of the valuation date. Also, the DCF method may be more suitable to estimate the limited and short-lived downside period more accurately as compared to other valuation methods.

Also, a H-model or multi-period model may be used with multiple discount rates to factor the expected short-term and long-term risks of the company. A higher discount rate may be applied for the first 3-year period when COVID-19 is expected to impact the earnings of the company comparatively more than the next 2 years for which a lower discount rate may be selected and for the period after which the business activity returns to normal, a terminal discount rate may be used which is in conjunction with the long-term Cost of equity of the company.

With the recent uncertainty created by the COVID-19 pandemic, the use of the Discounted Cash Flow analysis may be more appropriate for the determination of fair market value for many small closely held businesses such as private limited companies or unlisted public companies.

Page Contents

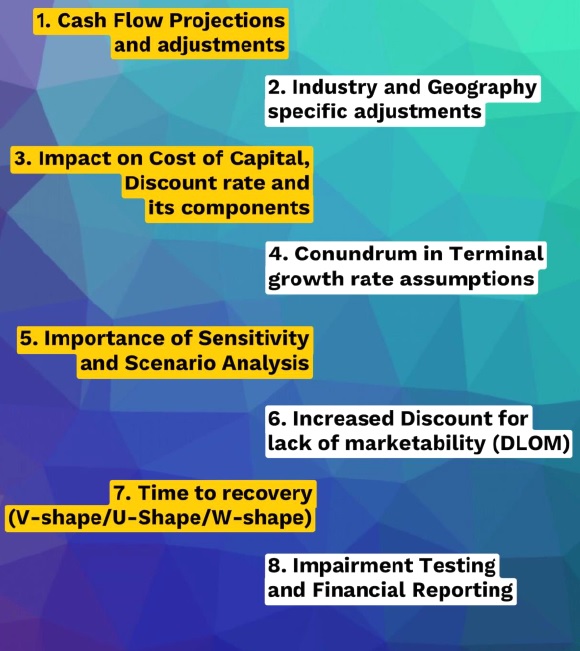

- Aspects to be considered during valuation under Income Approach due to COVID-19:

- 1) Cash Flow projections and adjustments:

- 2. Industry and Geography specific adjustments:

- 3) Impact on Cost of Capital, Discount Rate and its components:

- 4) Conundrum in Terminal Growth rate assumptions:

- 5) Importance of Sensitivity and Scenario Analysis:

- 6) Increase Discount for Lack of Marketability (DLOM):

- 7) Time to Recovery (V-shape/U shape/W shape/K shape):

- 8) Impairment Testing and Financial Reporting:

- Aspects to be considered during valuation under Market Approach due to COVID-19:

- 1) Short Term Market prices or industry multiple not conclusive:

- 2) Fair value is not distressed value/fire value/fear value:

- 3) Preference of Forward-looking Market Multiples:

- 4) The comparability of recent transactions:

- 5) Impact of maintainable revenue/EBITDA assumptions:

- 6) Avoid Double Dip Effect:

- 7) Actively traded vs non-actively traded investments (Volume and frequency):

- 8) Importance of use of ranges:

Aspects to be considered during valuation under Income Approach due to COVID-19:

Source: Self

1) Cash Flow projections and adjustments:

Business valuation involves making cash flow projections and is forward-looking in nature and such cash flow projections reflect what is “known or knowable” to the valuer on the measurement date i.e the valuation date. Due to the rapid, material and sudden change in the economy and the industry around the world, the valuation of a particular entity may be drastically different as on 31st December 2019 as compared to the valuation of the same entity carried out on 31st March, 2020 or on 31st March, 2021. Since there shall be significant fluctuations and variances from historical trends of revenue and expenses across financial years 2020, 2021 and 2022, the requirement of making normalization adjustments to such revenue and expenses becomes of paramount importance during forecasting of financial statements for the purpose of valuation.

The materiality of such cash flow adjustments may vary depending on the specific entity type. Furthermore, there is significant uncertainty about the duration and frequency of pandemic outbreaks, requiring substantial judgement and scepticism on the part of the valuer in development of cash flow projections based on the “known and the knowable” at the time of the valuation.

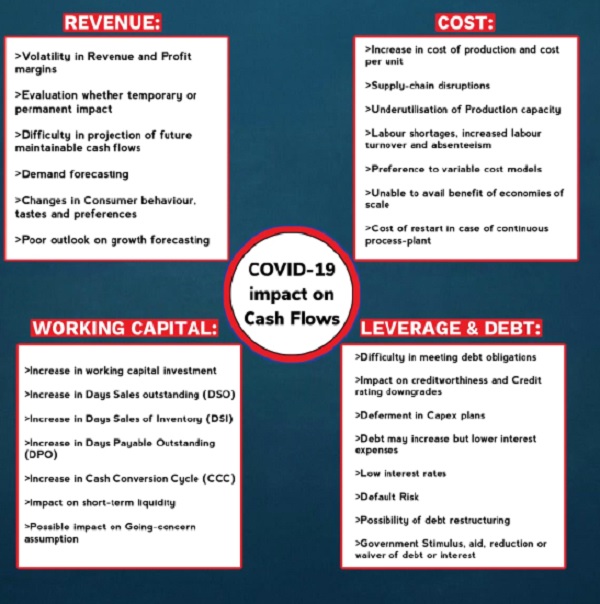

Due to COVID-19, the following considerations are required in cash-flow projections:

Source: Self

A) Revenue Considerations: The valuer shall take into consideration the volatility inherent in projections of revenue and profit margins due to the impact of COVID-19. It is significant to evaluate whether the fluctuations in revenue are temporary or permanent in nature to ensure appropriate forecasting for the next 5 years and also for perpetuity. Due to the difficulty in forecasting revenue for the forecasting period, estimating future maintainable cash flows becomes challenging. The valuer should quantify the impact of demand and growth forecasting with due consideration to the changes in consumer behaviour, taste and preference, if any, due to recurrent lockdowns and the vagaries of pandemic. Also, in compliance to the ethical standards and regulations of The Companies (Registered Valuers and Valuation), Rules 2017, the Valuer has to ascertain the reasonableness and appropriateness of the forecasted numbers and ensure a declaration is provided to that extent in the valuation report and he should not disclaim the responsibility and shift such burden of responsibility to the Management.

B) Cost Considerations: The valuer should evaluate the rationale and the impact of factors contributing to the increase in cost of production and thereby leading to an increase of cost per unit of product. The valuer should take cognisance of such contributory factors leading to an increase in the cost of production, such as due to supply-chain disruptions of preferred vendors and due to experiencing hindrances and disruptions in logistical chain of movement of goods. Other factors impacting adversely are labour shortages leading to increased incidents of labour absenteeism and a higher labour turnover due to restriction on movement of civilians during lockdowns and in containment areas. Due to frequent lockdowns and lack of operational staff and foremen, the production capacity and efficiency of plant and machinery may be underutilized and therefore the benefits of economies of scale on cost may be under-availed. The valuer may ascertain the impact of cost of the management decision to shift to a variable cost model from a fixed cost model such as that of opting for co-working and sharing office spaces rather than incurring a fixed rental cost in the nature of sunk cost or future financial commitments.

C) Working Capital Considerations: The Valuer should evaluate the impact of COVID-19 on the investment in working capital. Mostly, the requirement of investment in working capital should increase due to several factors such as the increase in the Cash Conversion Cycle (CCC) due to the increase in the number of days working capital remains invested in inventory (i.e. DSI) and trade receivables (i.e. DSO) before being realised into cash due to the slowdown in business operations due to lockdowns and other disruptions due to COVID-19. Unless the days of payable outstanding (i.e. DPO) increases too, there shall be a marked increase in the days of working capital investment which may have an adverse impact on the liquidity and the going concern assumption in case the Current Ratio or the Acid Test Ratio is between 0 to 0.99 and in that case the valuer, in a few cases, may have to consider its impact on the selection of the Valuation base, from income approach to liquidation approach.

D) Leverage and Debt Considerations: The Valuer should evaluate whether the Earnings Before Taxes (EBT) becomes negative after reduction of Interest expense from Earnings Before Interest and Taxes (EBIT) and the Free Cash Flows eventually become negative, signifying the poor health of the entity to meet its debt obligations. Also, the Valuer may evaluate the Degree of Financial Leverage (DFL) (i.e. DFL= (EBIT)/(EBT)) to reasonably infer the amount of debt which can be taken and paid since a higher DFL may indicate earnings volatility and an increased inability to assume and repay additional debt and interest whereas a low DFL may indicate a lower level of fluctuation in earnings and the ability to take additional debt. The valuer may also evaluate the impact of COVID-19 on the creditworthiness and the credit rating of the entity to further consider the probability and effect of default risk. Even though plans of Capital expenditure and Capital Budgeting may be deferred during the COVID-19 crisis to preserve capital, there may be tendency to undertake additional debt due to the reduced interest rates, therefore debt may increase but the interest expenses may reduce. The valuer may evaluate the impact of quantification of any Government stimulus provided in the form of a loan or interest waiver or a moratorium period provided in the payment of interest such as the forgiveness of the full loan amount taken under Paycheck Protection Program (PPP) in the United States on the satisfaction of certain conditions or a 6 month moratorium announced by the RBI EMI Moratorium dated 27.3.2020 from March to August 2020 on repayment of loan, at the discretion of the bank.

2. Industry and Geography specific adjustments:

COVID-19 may have been a death knell for businesses in certain sectors i.e. Travel and tourism, hospitality, aviation and consumer discretionary, whereas it was a blessing in disguise for the prosperity and growth of businesses in specific sectors i.e. Digital payment platform, Educational Technology firms, Pharmaceuticals, Food delivery and aggregators platforms. Therefore, the valuer should evaluate the impact of COVID-19 on the specific industry sector the business pertains to and shall also gauge the impact of other specific fundamental parameters such as the industry demand and growth affecting the financial condition and operating outlook of the business and consider the same in his valuation analysis.

The severity of COVID-19 impact on the economic health of several sectors is enumerated below:

Source: Self

Therefore, the Valuer should be informed that the industry wise economic impact that COVID-19 has varied across industries and in general the industry wise impact may be categorised as:

1) Minimal — consumer staples, technology and utilities;

2) Moderate — financials, health care, industrials and real estate; and

3) Significant — consumer discretionary, energy, retail and tourism and hospitality.

3) Impact on Cost of Capital, Discount Rate and its components:

The valuer may consider to continue using Capital Asset Pricing Model (CAPM) and other established methods for calculating the cost of capital as they have a well-founded theoretical basis and should be appropriate to calculate the discount rate even in an economic downturn. However, a thorough review of each component of the Cost of Capital is required both individually as well as jointly with other inputs and the possibility of normalizations to such components may not be ruled out in order to evaluate the assessment of the overall result.

The following table enumerates the major aspects to consider in calculation of the Cost of Capital under the Income Approach due to COVID-19:

Source: Self

The various components of cost of equity:

Cost of Equity= Risk-free Rate (Rf) + Equity Risk Premium (ERP)+ Company Specific Risk Premium/Alpha (α)

(A) Reduction in Risk-Free Rate:

To combat the economic downturn and recession due to the onset of COVID-19, the RBI had undertaken several initiatives to infuse liquidity in the economy by reducing the Repo Rate and thereby the base interest rate and coupled with the increasing demand by investors for quality and safe investments in Government Bonds, there has been a decrease in the risk-free rate.

Source: COVID-19- Impact on valuations material dated 8.04.2020 by EBC Learning and Finvox Analytics

A decrease in the risk-free rate may not necessarily mean a reduction in the Cost of Capital since there may be an upward impact on the Cost of Capital by other components due to increase in risk and volatility of returns.

B) Increase in Equity Risk Premium i.e (ERP= Rm-Rf):

There has been an increase in the Equity Risk Premium on the onset of COVID-19 i.e. April 2020, as compared to the pre-COVID era i.e. February 2020, both in the developed economy of USA and in the developing economy of India, due to the increase in expectation of return on the stock on the assumption of a higher risk and volatility on returns by the investor.

United States of America-

Aswath Damodaran increased implied ERP from 5.77% as of March 1, 2020 through 6.52% as of April 1, 2020 (Source: http://pages.stern.nyu.edu/-adamodar/)

Duff & Phelps also increased Recommended US ERP from 5.00% to 6.00% with effect from March 25, 2020 (Source: https://duffandphelps.com/insights/publications/cost-of-capital)

India-

The Equity Risk Premium of India as in January 2020 as per Aswath Damodaran was 7.08% (Source: https://www.youtube.com/watch?v=h8y02tnMY_s)

The Equity Risk Premium of India at the beginning of April 2020 was 7.50% as per Incwert Valuation Chronicles, Series 4, 2020 (Source: https://secureservercdn.net/160.153.137.218/end.241.myftpupload.com/wp-content/uploads/2020/07/Assessment-of-discount-rate_india_June-2020.pdf?time=1594016580)

The valuer should prefer using of Forward-Looking estimate for Market Return over the Historical estimate of Market return since, say, the historical estimate for the market indices such as NSE NIFTY Returns would disregard the impact of the structural changes occurred in the previous year which may be an economic downturn as was in 2007 or may be the favourable effects of Liberalisation, Privatisation and Globalisation model (LPG Model) introduced in year 1991. Whereas, the Forward- looking estimate of market return ensures to capture the implied Equity Risk Premium at the current market value of the equity by equating the present value of expected future cash flows to the total market capitalization of all the constituents of the index. Therefore, the adoption of the latter estimate would ensure that when risk and volatility increase and consequently Market Indices fall, it would lead to an increase in the Equity Risk Premium (ERP).

C) Increase in Company-Specific Risk Premium/Alpha (α):

In order to ensure all factors contributing to risk are considered in the discount rate, the valuer uses his professional judgement to estimate the company specific risk premium which is dependant on the internal factors of the company such as financial performance in previous years, product or service vertical, depth and concentration, competitive strength, risks associated to KMPs, litigation history and current status of pending litigations, small size and illiquidity, amongst other company-specific factors. Also, the uncertainty in cash flow projections may lead to some downside scenarios being missed from the probability weighted average set of projections and the valuer may be inclined to factor a risk premium, namely, Alpha, for the same in the discount rate for appropriate estimate of valuation.

Therefore, Company Specific Risk Premium/Alpha (α), may be captured by taking effect in:

- Future projections/ cash flows of the company or

- Adding additional risk premium to the cost of equity for COVID-19 in addition to the internal factors of the company.

Usually, valuers estimate company specific risk premium or Alpha to be in the following range:

- For higher risk companies in the range of 4-4.5%

- For lower risk companies in the range of 1.5-2%

D) Elimination of Double Dip:

The valuer should be cautious and avoid double count wherein both, normalizations to cash flow projections reflecting the impact of COVID-19 have been made and the element of risk premium due to COVID-19 has also been considered in calculating the company-specific risk premium. Double dip should be avoided since it would lead to understated or conservative valuation of business.

The valuers prefer adjustments for COVID-19 on the cash flow projections over the adjustment made in the cost of capital by adding a risk premium to Alpha since the latter ensures more accurate forecasts and is lesser subjective. However, adjusting for COVID-19 impacts on both cash flows and discount rate may lead to double counting the pandemic effect and an inaccurate and underestimated business valuation.

The risk premium added in cost of equity should be for a specific time period and not for the entire projection period.

In case adjustments are unable to be made to the cash flows, then adjustments may be made to the discount rate and also a H-model or a multi-phase model of discount rates may be used, wherein initially a higher discount rate may be used for a period of 3 years and then discount rate may be brought down corresponding to the pre-covid level for the remaining 2 years out of the 5-year forecast period.

It has been observed that some valuers have followed an approach of adding a discount for distress. Distressed entities generally have higher risk profiles and lower profitability levels compared to their healthier competitors, and a discount for distress, usually at least 20%, is built into the valuation. However, this is not a preferred approach and a better approach is to consider the impact of risk in either the cash flows or the discount rate.

Therefore, the valuer should reasonably expect-

A lower Increase in Cost of Equity

- In case the management considered the effect of COVID-19 and builds the risk in cash flow projections

- A higher Increase in Equity Risk Premium (ERP) is set off by a lower decrease in Risk-Free Rate (Rf)

Higher Increase in cost of Equity

- In case the management considered the effect of COVID-19 and builds the risk in Cost of Capital by adding a COVID-19 specific risk premium.

E) Increased Volatility of Beta:

Estimating betas using weekly returns over the past two years shows that, on average, betas have increased substantially since the COVID-19 pandemic began in March 2020. An increase in beta, all other factors being unchanged, implies an increase in discount rate and a corresponding reduction in valuation. The increase in betas varies broadly across industries. The COVID-19 pandemic has also resulted in an additional element of uncertainty for the valuer in regard to the most appropriate way to calculate beta. It is well established that the estimation period may impact betas. Since, the COVID-19 pandemic unfolded drastically, betas calculated using short-term lookback windows are more likely to be affected than betas calculated from longer-term data. Again, this is a valuer’s professional judgement to evaluate and consider the sector to which the company belongs to determine whether the long-term price movements should be given higher weightage in Beta estimations or short term. It is to be kept in mind that for the sectors, which have had moderate to low impact beta may be estimated using long term price movements, and sectors which have had high impact with lingering after effects, would require higher weightage to short term price movements for beta estimations.

The valuer should apply increased scrutiny to previously assessed betas which shall be appropriate to ensure that expected sector volatility is appropriately incorporated within the discount rate. Due to the extreme volatility experienced due to the spread of the COVID period there can be a disproportionately large impact from the data in certain months on the beta calculations, in some cases causing betas to double or halve from previous levels. The valuer may decide to appropriately exclude the data of these particularly volatile months in certain circumstances to ensure the beta isn’t disproportionately weighted towards data from this highly volatile period.

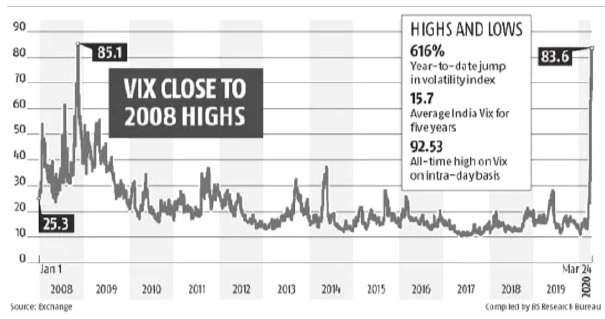

F) Levels of Volatility Index (VIX):

India VIX, which is also called the fear index, touched 86.63 on 24th March, 2020, higher than its historic closing peak of 85.13 it reached during the global financial crisis in November 2008. The VIX Index is an apt indicator to gauge the investor sentiments and whether the market value is a true indicator of Fair Value or is indeed Fear Value. The VIX Index which usually trades at the level of 20, when trades at a level of 40 or above represents investor’s anxiety and fear and such high levels of implied volatility indicate are acutely bearish.

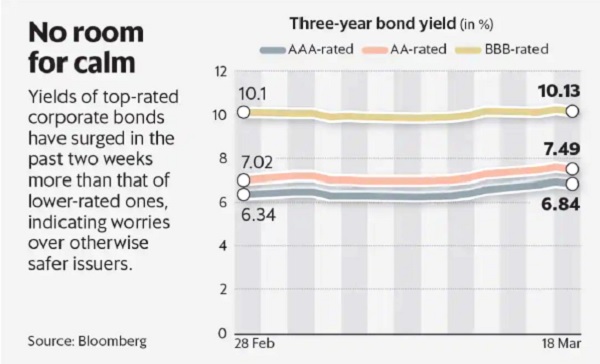

G) Degree of spike in Credit Spread:

During the months of March and April 2020, India’s corporate bond market had been pricing in greater risk due to the Covid-19 outbreak threatening economic activity and the corporate bond spreads continued to widen even for AAA-rated paper. In fact, the yield on AAA-rated corporate bond had jumped more than that on the lowest investment grade rating of BBB, as the below chart indicates. For raising three-year money, AAA-rated companies had to shell out at least 6.8% then against a modest 6.3% a mere two weeks earlier. Those with AA rating have had to shell out at least 25 basis points more. Even the strongest balance sheets were having to shell out more to entice investors now.

Therefore, the valuer takes into consideration the increase in the Credit spread due to the impact of COVID-19, in determining the cost of debt since a credit spread is the risk premium add-on to the base interest rate used when pricing corporate debt issues and reflects the credit rating or risk rating of the company, the maturity of the issue, current market spread rates, as well as other components such as security and liquidity.

H) Increase in cost of Debt (Kd):

The valuer may need to evaluate the revision in the cost of debt to take into account industry, geographic or company specific risks arising out of current market conditions. Therefore, valuers must consider on a case-by-case basis whether the actual and current debt margins should be applied or not in order to estimate an appropriate cost of debt by giving weightage to the following factors:

- Whether a company is funded short-term or long-term,

- The requirement of future re-financing,

- Promised vs. expected yield,

- Assumption whether observed credit spreads persist indefinitely,

- Creditworthiness and credit rating of the entity

- Decrease in base interest rates

- Ability to meet debt obligations and possible debt restructuring

- Requirement of additional debt to meet Capex plans

- Conversion of debt into equity share capital

- Government stimulus on waiver or relaxation of debt or interest

The same principle holds for the appropriate target debt/equity ratio which, in general, might be expected to be lower relative to equivalent historical ratios in certain sectors due to the constraints on debt financing packages during covid

I) Other notable considerations such as capital restructuring, decline in stock markets, changes in business and consumer confidence, change in Systemic Risk, rising unemployment levels and precedence of historical financial crisis have significant impact on the cost of capital or the discount rate which the valuer takes in consideration while valuing the business. The valuer should evaluate the impact of the capital restructuring exercise on the cost of capital in situations of buy back of shares, loan or interest restructuring by bank due to loan becoming NPA, loan refinancing at a higher interest rate due to credit downgrade or such impacts in case of conversion of debt into equity. The decline in stock market due to COVID-19 instils fear in the minds of the investors towards equity investments and a higher market return may be expected due to higher volatility. COVID-19 has disrupted the lifestyle and livelihood of the public which may lead to a change in business and consumer confidence or a change in taste and preference and may lead to an increase in the required rate of return from the business for the investors.

As per the research paper titled “Change in Systemic Risk in Indian Financial Market due to COVID-19 Pandemic” by Chandramani Jha and Dr. Utkarsh Goel, (IIIT), Allahabad, Department of Management Studies, the marginal expected shortfall of financial firms of NIFTY 50 for pre-COVID year 2019-20 and COVID year2020-21 were measured and found that the undercapitalization of Indian financial firm has increased 3 fold during COVID-19 Pandemic ensuing systemic risk had been increased during COVID-19 year to pre-COVID year. The result is also supported by daily stock return correlations of financial firms which is a simple and robust indicator of systemic risk. It has been found that the correlations of financial firm stock returns among themselves and market index as well is increased during COVID-19 pandemic that led to rise in systemic risk.

Source: Research paper titled “Change in Systemic Risk in Indian Financial Market due to COVID-19 Pandemic” by Chandramani Jha and Dr. Utkarsh Goel, (IIIT), Allahabad, Department of Management Studies

As per the above table, HDFC Bank has highest average capital shortfall and contributes maximum to the systemic risk during covid-19. Whereas SBI Life has contributed lowest to systemic risk in both pre-covid and covid year.

4) Conundrum in Terminal Growth rate assumptions:

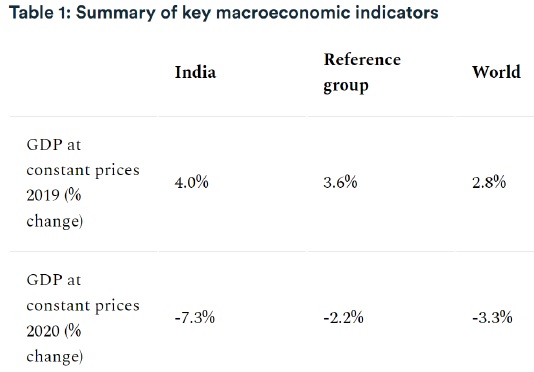

The valuer, usually, considers the growth rate of Gross Domestic Product of the country it is situated in as the terminal growth rate for the business. While economies worldwide had been hit hard, India had suffered one of the largest contractions. During the F.Y. 2020-21, the rates of decline in GDP for the world were 3.3% and 2.2% for emerging market and developing economies. The table hereunder summarises growth of GDP pre-covid i.e. F.Y. 2019 and post-covid for India i.e. FY 2020, along with a reference group of comparable countries and the world. The fact that India’s growth rate in 2019 was among the highest, makes the drop due to Covid-19 even more noticeable. The valuer may assume the terminal growth rate in the range of 3.5%-4% which is a close approximation of the long-term growth rate for India’s GDP at constant prices in 2019 i.e. pre-covid period.

Source: World Economic Outlook Database April 2021, International Monetary Fund

Additionally, the valuer should acknowledge that the long-term growth rate assumptions should reflect market participants’ long-term estimates for inflation and real economic growth, adjusted to reflect the outlook for the sector that a company is operating in as well as company specific factors. Typically, the effects of new industries and technologies and the impact of competition within industries may limit the company’s specific long term growth rates to a lower level than for the economy as a whole to at least some degree. However, the long-term sector and company specific outlook may well have changed as a result of Covid-19, with some sectors demonstrating stronger growth such as online educational platforms i.e Byju’s and Unacademy, online connectivity platforms i.e Zoom Meetings, digital payments platforms i.e. Phonepe, Bharatpe, Paytm etc., and more resilience and others being relatively weaker than previously expected. The overall drop-in risk-free rates, and indeed discount rates more broadly, is also arguably consistent with a reduction in long term economy wide nominal growth expectations to at least some degree, due to changing expectations of inflation and/or real economic growth. It is therefore important that the discount rate and long- term growth rate assumptions used within a valuation are internally consistent, otherwise the capitalization rates/multiples implied within terminal values may not be realistic or reconcilable with market data.

5) Importance of Sensitivity and Scenario Analysis:

Fair value is based on what is known and knowable at the time of valuation and it requires informed judgement on the part of the Valuer. Thus, while valuing companies for the year 2020 and onwards, revenue and expenses may show a significant fluctuation and deviation from the Last Twelve Months data (LTM) and historical trends and may not reflect a normal level of operations for the basis of forecasting entity’s operation. Thus, while computing the fair value, sensitivity and scenario analysis might be worth considering wherein probability weighted average in multiple scenarios for the forecasts may be preferred over a single set of projections.

Different cash flow scenarios could be a useful way of understanding the range of potential outcomes for a business and its attached risks. For example, the following multiple scenarios may be considered in the Sensitivity Analysis:

- Base Case: In this scenario the revenues and operations may be impacted for 1-2 years and will return to normal level of operations after that period. This may be considered as scenario with short to medium term disruption and the severity of impact of COVID-19 is moderate.

- Bear Case: In this scenario the revenues and operations may be impacted for the next 3-5 years and shall take time to recover. In such cases, longer term projections would be required (say 10 years). This may be considered as a scenario with a broader and longer economic downturn and the severity of impact of COVID-19 is significant.

- Bull Case: In this scenario the revenues and operations would return to normal level of operations within the same / next year. This may be considered as a business-as usual scenario and the severity of impact of COVID-19 is nil to negligible.

The valuer may determine whether Going Concern Value may be arrived at using scenario analysis. While Scenario analysis is not new and is often used in valuation given the uncertainty around future, this is more relevant during these times of COVID-19 crisis and disruption in business.

In case, the valuer chooses to value the company using scenarios, value of going concern may be:

Going Concern Value = (Value base case x Probability base case) + (Value bear case x Probability bear case) + (Value bull case x Probability bull case.

6) Increase Discount for Lack of Marketability (DLOM):

The valuer shall evaluate whether there is a significant impact of COVID-19 on the aspect of illiquidity or non-marketability of investment in the concerned company or whether there is a decrease in the ability on the part of the investors to access the Capital or Secondary Market to liquidate the investment in the company, thereby demanding a COVID-19 marketability discount.

The logic to develop a COVID-19 marketability discount can be applied to directly adjusting the multiplier, discount, or capitalization rate or applied as a separate discount for marketability. As with any discount, care must be exercised by the valuer to avoid Double Dip i.e. to not apply a discount for a risk that has already been fully accounted for.

When applying a COVID-19 marketability discount, Valuers must value the subject company similar to how they would have done prior to COVID-19-related issues becoming prevalent. Valuers may adjust future cash flows to what is most likely. Since February 2020, in general, marketability discounts have increased as a result of the factors below – even though it has been partially offset by a lower risk-free rate of interest:

- Decreased access and opportunities to financing for the underlying business and the purchase of the minority position itself.

- Decreased Mergers and Acquisition activity and a reduced pool of willing buyers.

- Increased supply side of secondary investments as institutions seek to divest to rebalance and/or meet regulatory requirements.

- Reduced expected profitability, cash flow and longer realization timelines.

- Increased perceived risk and higher required rate of return

The following tables show the trends for change in Deals in both, Private Equity and Mergers and Acquisitions in the last 5 years including the impact of COVID-19:

Therefore, a higher discount for lack of marketability (DLOM) shall be required in the present COVID-19 environment since the transactions of businesses have decreased significantly and there is a drastic decrease in market activity and of the pool of interested, willing buyers, thereby leading to an increase in illiquidity and the DLOM.

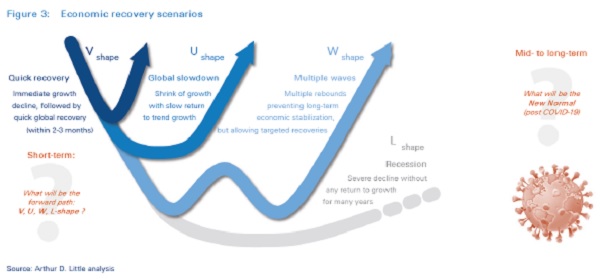

7) Time to Recovery (V-shape/U shape/W shape/K shape):

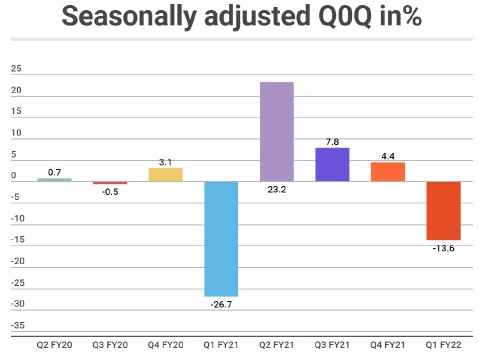

India’s Gross Domestic Product (GDP) contracted by 7.3% in F.Y. 2020-21.

A V-shaped recovery is the best-case scenario, where the economy bounces back immediately after a sharp decline to go back to its pre-recession level in less than a year.

In a U-shaped recovery, the economy experiences stagnation for a significant period of time after declining. It then rises gradually to its previous peak. This means the recession lasts longer, causing job losses and erosion of savings.

Also called the “double-dip recession”, a W-shaped recovery sees an economy staging a brief comeback only to fall a second time. This scenario breaks consumer confidence and enters the full recovery period that can take up to 2 years. The economy will witness two recessionary periods.

In respect to the Indian economy, if one looks at quarter-on-quarter growth, the recovery seems to be W-shaped if the coming quarters see growth. However, when seen quarter-on-quarter, GDP generally contracts in Q1 because the size of the economy is higher in Q4.

Source: Business Standard publication dated 7.10.2021

When growth is seen in the context of seasonally adjusted quarter-on-quarter, it seems to be W-shaped if it comes in the next quarters. This is the most appropriate measure in the current times.

Source: Business Standard publication dated 7.10.2021

Therefore, the recovery pattern of Indian economy is W shaped and the Valuer may take due consideration of the same while forecasting and valuation of the business.

The following table explains the various types of economic recovery patterns in pictorial representation:

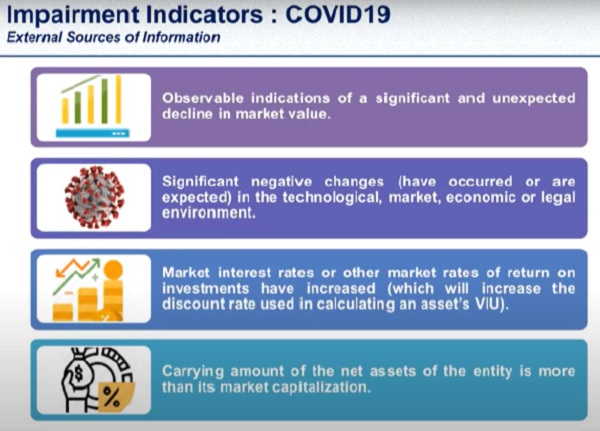

8) Impairment Testing and Financial Reporting:

Since, the financial and capital market environment across the globe has got affected by the rapid spread of COVID-19, there may be significant volatility or indications of significant decline in market prices of financial instruments. The valuer should evaluate whether the management has carried out the annual impairment testing of assets or cash generating units in compliance to the IND-AS 36, Impairment of Assets. The following external factors are indicative of requirement of impairment testing and the estimation of the recoverable amount of the asset, including non-financial assets, (i.e. Recoverable value is the higher of Fair value less cost of selling and Value in Use.) As per IND-AS 36, Weighted Average Cost of Capital (WACC) derived from Capital Asset Pricing Model (CAPM) can be used as a discount rate after adjustments for COVID-specific risks, to derive the Value in Use of the asset.

Source: Material of Impact of COVID-19 on valuation of securities and financial assets by Finvox dated 23.6.2020

COVID-19 global pandemic has caused substantial contraction in the entity’s business since March 2020 and this depressed scenario is expected to continue over the next few quarters and onwards. Since entities are experiencing significant cancellation of business orders and bookings by its customers and the observable market value of the business as a whole has declined coupled with significant adverse changes occurring or are expected to occur in the technological, market and economy, are reasons enough for undertaking the impairment exercise and recognising impairment loss in case of long term or a permanent decline in the value of the assets.

The valuer acknowledges that cash flows may not be affected by impairment directly as the same is a non-cash transaction in nature. However, it directly affects the income statement and balance sheet in reducing the value of the assets to the recoverable amount in case of recognition of impairment loss.

Valuation under Market Approach:

Market-based valuations determine the value of a company by comparing it to similar business transactions. The valuer while applying the Market Method may be faced with the challenge of insufficient access to market data on insufficiently comparable competitors. Additionally, the valuer is posed with another distinct challenge of deciding to use pre- COVID-19 transactions in post-COVID-19 valuations. Expert valuation analysis and normalisation adjustments shall be required in order to produce useful financial metrics. During such unprecedented times of COVID-19, merely selecting a group of transactions from the past two years and calculating an average multiple shall not suffice.

Aspects to be considered during valuation under Market Approach due to COVID-19:

1) Short Term Market prices or industry multiple not conclusive:

The valuer should take a long-term view of the market multiples rather than a distressed multiple as on a specific date which may disproportionately reduce the value of the company.

The valuer should evaluate whether the market price of comparable companies on the valuation date represents fair value or not.

Valuer, usually, uses Last Twelve Months (LTM) EBITDA multiple while applying Market Approach, and such a singular use of LTM multiple may not be appropriate and may require a combination of LTM and NTM i.e. Next Twelve months, multiples.

The valuer should note that the unlisted companies or the private limited companies should be valued using inputs consistent with the perspectives of the market participants, that emphasizes on the use of general market conditions over and above market conditions for a particular date.

Therefore, Industry multiple calculated based on the prevailing market prices as on 31.3.2020 may not be an appropriately adjusted Industry Multiple for unlisted companies especially because of a high volatility factor. Therefore, it is pertinent for the valuer to use the multiple based on the market prices over a period of time rather than on a specific date.

The valuer takes cognisance of the fact that the unlisted and private limited companies are less volatile since private investments lag the public markets and change value less quickly as compared to the actively traded public limited companies and should not be discounted as much as the public limited companies. The private investments lag the public markets since the public markets have a more active market and there are frequent and quick sale and purchase of equity shares as compared to that for a closely held private limited company, hence the volatility is lower in the latter company.

Source: COVID-19- Impact on valuations material dated 8.04.2020 by EBC Learning and Finvox Analytics

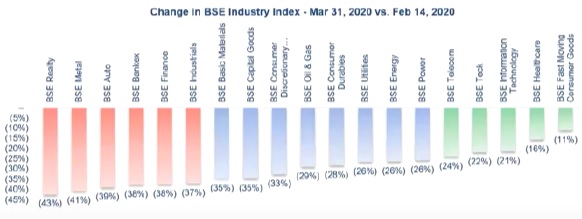

The valuer should not assume that the corresponding industry multiple of Realty has also declined by 43% just as there is a similar decline in the Realty Index, while conducting business valuation.

2) Fair value is not distressed value/fire value/fear value:

As per IND-AS 113, Fair Value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Significant elements of Fair Value:

1) Orderly Transaction

2) Measurement Date

3) Market Participants assumptions wherein there shall be a willing buyer and a willing seller and there shall be focus on future maintainable income or revenue

Fair value is not the same as Distressed sale Price/Forced sale price.

Fair Value means the amount which would be received in an orderly transaction given an appropriate marketing period. In case of distressed sale or a forced sale during the adverse impact of COVID-19, then an appropriate marketing period may not have been available to ensure an orderly transaction and such consequent distressed sale price should not be considered as Fair Value.

Comparable transactions pertaining from February 15th to March 31st 2020 should not be considered since such value is not fair value and is a forced/fire sale price.

It is important to assess whether current market prices are reflecting long term fair value. The valuer should consider preference of unaffected metrics over affected market prices and in case of use of actual or normalized market multiples, it is important to document the nature of the selected multiples.

The valuer may consider the VIX Index, which is an apt indicator to gauge the investor sentiments and whether the market value is a true indicator of Fair Value or is indeed Fear Value. The VIX Index which usually trades at the level of 20, when trades at a level of 40 or above represents investor’s anxiety and fear and such high levels of implied volatility indicate are acutely bearish.

3) Preference of Forward-looking Market Multiples:

The valuer should prefer the use of Forward-looking public company market multiples. In the guideline public company method (GPCM), a variation of the market approach, forward-looking multiples are now stressed to indicate business value. This is because, these multiples reflect COVID-19-related market pricing and earnings impacts. The recent financial history of a company (its past revenue, earnings, cash flow, etc.) are now viewed as less reliable parameters used to indicate value, since they do not fully reflect the subject company’s post-COVID-19 financial conditions and earning power outlook.

4) The comparability of recent transactions:

The Guideline Public Method and Comparable Transaction Method is a comparable analysis method that seeks to value similar companies using the same financial metrics applied in recent comparable transactions. Market approach requires use of different multiples like Book Value Multiple, EBIT multiple etc. The valuer should be mindful that a multiple reported even a month ago might materially misrepresent the risk associated with a comparable transaction as on date.

The valuer may prefer to use the Transaction Multiples method but special attention and caution is required to be provided on such comparable transactions occurred during the COVID-19 crisis period which may require downward adjustments to prevent overstatement of business valuation. The valuer may use his professional judgement to evaluate the degree of this adjustment which may need to be assessed on a case-to-case basis depending upon the industry and the level of stress.

Thus, the valuation professional needs to carefully use the multiples associated with the transactions that occurred during this crisis.

In usual practice, the comparable transactions pertaining to a time period of previous 2-3 financial years are considered and a longer duration is not preferred due to drastic changes in economy, industry and technology and other macro-economic factors.

5) Impact of maintainable revenue/EBITDA assumptions:

The valuer shall evaluate maintainable revenue and earnings, keeping in view the market participants’ perspective.

The valuer shall analyse comprehensively the impact on the financial metrics of the target company such as PAT, EBITDA, EPS, EBIT, Revenue etc.

The valuer shall gain insight by industry benchmarking to comprehend short-term and long-term impacts on the financial metrics.

6) Avoid Double Dip Effect:

In case, the valuer having calculated the target multiple based upon the current market price using the LTM multiple basis for comparable companies, that already includes the impact of COVID-19, shall not consider making adjustments to the performance or financial matrix of the target company, in order to ensure that the business value is not underestimated or conservative.

7) Actively traded vs non-actively traded investments (Volume and frequency):

The valuer should take cognisance of the fact that infrequently traded or non-traded investments are usually less volatile than actively traded investments. During times of drastic public market value changes, private investments tend to lag the public markets and tend to change value less steeply than the actively traded investments.

The private investments lag the public markets since the public markets have a more active market and there are frequent and quick sale and purchase of equity shares as compared to that for a closely held private limited company, hence the volatility is lower in the latter company.

8) Importance of use of ranges:

Due to high volatility and the possibility of subjective valuation using scenario analysis or due to the shortcomings of selection of market multiples methods during COVID times, the valuation ranges may need to be wider than normal, and these ranges may well be subject to volatility as valuations are updated over time.

In terms of financial reporting valuations, disclosures in the valuation report may require to be more comprehensive and mention that valuations could change quickly over a relatively short time frame, particularly if the businesses are highly leveraged.

Conclusion:

The valuer is expected to apply his professional judgement on case-to-case basis since there is no set thumb rule to approach and account for market uncertainties and volatility in the valuation exercise and no standard normalization adjustments to cash flows or discount rates are made available to make the valuation assignment any less subjective. The market environment is so unpredictable and volatile that if a particular business were to be valued on 31st December 2019, it may reflect a drastically different picture as against being valued on 31st March 2020 or on 31st March 2021. The engagement with management becomes of paramount importance to discuss and assess any short-term or long-term effects in financial performance or metrics.

The valuer may consider using traditional approaches to business valuation paralleled with conducting a more meticulous due diligence on the quality, accuracy and completeness of financial forecasts provided to them and in deciding the nature and extent of normalisation adjustments, if any, to be made to revenue, multiples, discount rates and other financial or performance matrix. Thus, implication and challenges to the valuation would be unique and negotiating the valuation to close a deal would remain a challenge.

The use of range of values has become significant in every engagement along with a disclaimer that valuations may change significantly and frequently given the changes in such dynamic circumstances.

Author Bio