Quarterly Return and Monthly Payment Scheme (w.e.f. 01.01.2021)

The scheme is GSTIN wise. It means that having different GSTIN under Same PAN may opt for the scheme in some GSTIN and not in other. Once opted the scheme has to applied unless the taxpayer revise the said option.

Manner of opting the scheme Rule 61A

One may avail the scheme for any quarter from first day of second month of preceding quarter to last day of first month of the quarter.

However, the facility to avail the scheme is available throughout the year.

Example: Time limit to opt QRMP for Quarter April to June 2021 shall be From 1st of Feb 21 to 30th of April 21.

How to avail QRMP From 01.01.2021

| Auto migration by portal (for 1st Qtr of the scheme) | ||

| Turnover | GSTR 1 opted | Deemed option |

| Upto 1.5 Cr | Quarterly | Quarterly |

| Upto 1.5 Crore | Monthly | Monthly |

| >1.5 cr upto 5 cr | Monthly | Quarterly |

Registered person are free to change their option to QRMP scheme from 5th of December 2020 to 31st of January 2021.

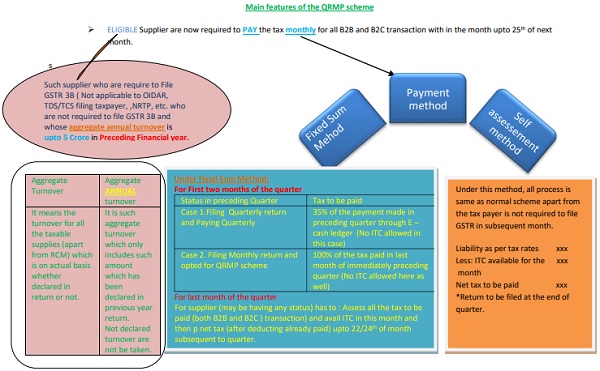

Reason behind the Scheme

There was a scheme of Quarterly Return and Quarterly payment earlier to introduction of QRMP scheme which has following drawbacks:

- Supplier (eligible to opt If have aggregate turnover upto 1.5 Crore) in this scheme has to pay quarterly as well as file return quarterly which blocks the payment to Government as well as recipient of such supplier though have paid their tax were unable to take Input Tax Credit (ITC) of same. This has been solved by introduction of QRMP scheme.

–

–

–

–

Author Bio

Everything described in superior manner. Very useful post and thank you Mr. CA krishnakant sah for your help.

Thank you very much. I take your best wishes for my upcoming results of CA.