Certain advantages for conversion of loan into equity share capital of the Company:

- No cash exchange occurs in the debt-to-equity swap.

- Increasing cash flow by decreasing liabilities.

- Avoidance to paucity of financial resources.

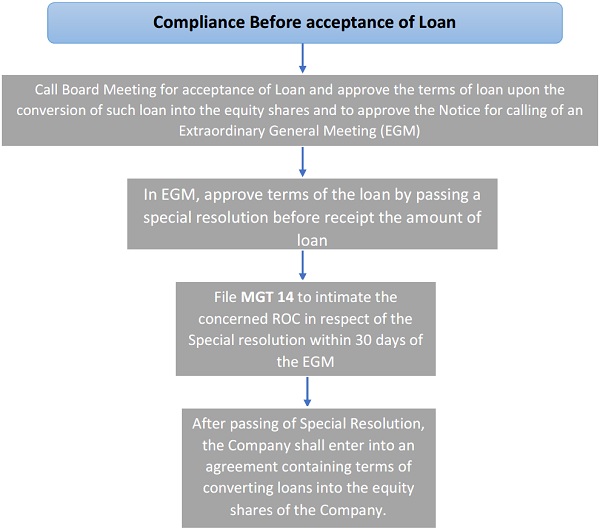

Process chart for Conversion of Loan into Equity shares

Section 62 (3) of Companies Act, 2013

Phase 1:

Important Note: It is mandatory to pass the special resolution at the time of acceptance of Loan with the term of conversion into equity share capital in future.

Phase 2:

Implications for non-filling of e-form MGT 14 within 300 days from the date of passing of Special Resolution:

What can be the amount of Penalty which MCA can levy?

The amount of maximum twenty-five lakh rupees can be levied on the Company. The penalty of maximum Five Lakh rupees can be levied on each director and other officers of the Company.

About the Author

Author is Divya Goel, ACS working as Assistant Manager- Company Secretary with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. Author can be reached at info@neerajbhagat.com.