Introduction: In recent years, the e-commerce industry has witnessed significant growth, transforming the way businesses operate and consumers shop. As this sector continues to thrive, e-commerce operators need to stay ahead of their financial responsibilities, including tax obligations. Section 194-O of the Income Tax Act, introduced in the Finance Act 2020, pertains specifically to the taxation of e-commerce operators. This article aims to provide a comprehensive understanding of the Tax Deducted at Source (TDS) requirements for e-commerce operators under Section 194-O.

E-commerce Operator:

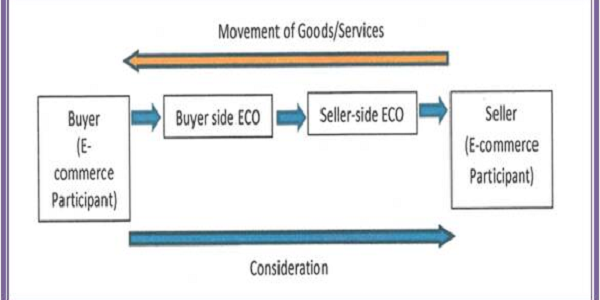

Definition: An e-commerce operator is a person or entity that owns, operates, or manages a digital or electronic facility or platform for electronic commerce. Sellers or service providers to offer goods or services to customers can use this platform.

E-commerce Participant (or Seller):

Definition: An e-commerce participant, also referred to as a seller, is an individual or business entity that sells goods or services through the e-commerce platform facilitated by the e-commerce operator.

Purpose of Section 194-O:

- The primary objective of Section 194-O of the Income Tax Act, 1961, is to ensure tax compliance in the e-commerce sector. It mandates that e-commerce operators deduct Tax Deducted at Source (TDS) on payments made to e-commerce participants or sellers. By deducting TDS at the source, the government aims to streamline the taxation process, prevent tax evasion, and ensure that taxes are collected efficiently from transactions conducted in the digital marketplace.

- This provision simplifies the tax compliance process by shifting the responsibility of deducting and depositing TDS from the individual sellers to the e-commerce operators. It helps in ensuring that the appropriate amount of tax is deducted when payments are made to sellers, and this amount is then remitted to the government.

- By requiring TDS on e-commerce transactions, the tax authorities aim to curb tax evasion in the growing digital economy. It provides a mechanism to track and collect taxes on income generated through e-commerce platforms, making the taxation system more robust and effective.

Key Provisions of Section 194-O:

Applicability:

- Section 194-O applies to e-commerce operators, who operate digital or electronic platforms facilitating the sale of goods and services.

- The provisions apply to payments made to e-commerce participants, which include sellers, service providers, or any other person making sales through the operator’s platform.

Threshold Limit:

- The TDS provisions under Section 194-O are triggered when the annual gross receipts of the e-commerce participant exceed Rs. 5,00,000 during the financial year where the e-commerce participant is an individual and HUF and holds PAN and Aadhar card otherwise tds@5%.

- TDS if where e-commerce participant is nonresident.

Rate of TDS:

- The e-commerce operator is required to deduct TDS at the rate of 1% of the gross amount of sales or services facilitated through its platform.

Example

Assuming an e-commerce operator facilitates the sale of goods worth Rs. 1,00,000 through its platform. According to the given information, the TDS rate is 1% of the gross amount of sales.

TDS = Gross amount of sales * TDS rate TDS = Rs. 1,00,000 * 1% = Rs. 1,000

So, in this example, the e-commerce operator would be required to deduct TDS at the rate of 1%, which amounts to Rs. 1,000 from the gross amount of sales. The remaining Rs. 99,000 would be paid to the seller, and the deducted TDS of Rs. 1,000 would be remitted to the government as per the TDS regulations.

Time of Deduction:

- TDS under Section 194-O is required to be deducted at the time of credit of the amount to the account of the e-commerce participant or at the time of payment, whichever is earlier.

Payment to Government:

- The e-commerce operator is obligated to deposit the deducted TDS to the government within a specified time frame.

TDS Return Filing:

- E-commerce operators are required to file TDS returns in Form 26QC, providing details of the TDS deducted, every quarter.

Non-Applicability to Individuals and HUF:

- Section 194-O does not apply to individuals or Hindu Undivided Families (HUFs) carrying out e-commerce activities for personal purposes.

- E-commerce participants should be residents of India.

Conclusion: In conclusion, e-commerce operators must be diligent in understanding and adhering to the TDS provisions under Section 194-O. Compliance with these regulations not only ensures adherence to legal requirements but also contributes to the overall integrity and transparency of the e-commerce ecosystem. By adopting best practices and integrating efficient TDS mechanisms, e-commerce operators can navigate the complexities of Section 194-O and contribute to the growth of a robust and compliant digital marketplace.

*****

About the Author: The author is Ruchika Bhagat, FCA helping foreign companies in setting up and closing businesses in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants is a well-established Chartered Accountancy firm founded in the year 1997 with its head office in New Delhi.

About the Author: The author is Ruchika Bhagat, FCA helping foreign companies in setting up and closing businesses in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants is a well-established Chartered Accountancy firm founded in the year 1997 with its head office in New Delhi.