Introduction: –

On the recommendations of the GST council, it has been decided that the applications / documents / forms pertaining to refund claims on account of zero rated supplies shall be filed and processed manually till further orders. To give effect to rule 89(1) to rule 97A of CGST rules, 2017, notification no. 55/2017 – Central Tax dt. 15th November, 2017, has been issued. Format for manual application of refund “Form-GST-RFD-01A” has been prescribed in the said notification.

Part I of this article talks about refund claims on account of IGST paid on Zero rated supplies as per section 16 of IGST Act, 2017.

Discussion on the law and procedural aspects: –

Discussion on the law and procedural aspects: –

As per section 54(1) of CGST Act, 2017, any person claiming refund of any tax and interest, if any, paid on such tax or any other amount paid by him, may make an application before the expiry of two years from the relevant date. Explanation 2 under the said section prescribes relevant date in various cases.

In case of zero rated supplies, refund of taxes paid can claimed as follows :

1. Refund of IGST paid on outward supply i.e zero rated supply with payment of tax

2. Refund of unutilised Input Tax Credit where zero rated supplies are made without payment of tax

Let’s have a walk through legislative provisions and procedure prescribed in abovementioned cases.

As per section 16(1) of IGST Act, 2017, zero rated supply includes (a) Export of goods or services or both and (b) supply of goods or services or both to SEZ units or SEZ developers. However, different procedures have been prescribed for different transactions.

Case 1 : Automated process for refund of IGST paid on export of goods i.e export with payment of tax

Prerequisites for sanction of refund of IGST paid are filling of GSTR 3B, table 6A of GSTR – 1 on GSTN portal and shipping bill on customs EDI system by the exporter. The application shall be deemed to have been filed only when export manifest or export report is filled. Upon receipt of the information regarding furnishing of a valid return in FORM GSTR-3 or FORM GSTR-3B, as the case may be, from the common portal, the system designated by the Customs shall process the claim for refund and an amount equal to the integrated tax paid in respect of such export shall be electronically credited to the bank account of the applicant.

In such cases, applicant shall ensure –

a) No discrepancy in the information furnished in table 6A of GSTR – 1 and the shipping bill

b) Invoice no. : Invoice number in GSTR-1 and shipping bill shall match with each other. It is observed that exporters have quoted different invoice numbers for Custom and GST purposes. In such cases, if common series of invoices is maintained, exporters will not face such mismatch problem.

c) Invoice amount, IGST amount paid, shipping bill no. furnished in GSTR – 1 shall match with details furnished in shipping bill.

d) Correct bank account no. mentioned at the time of migration

e) Correct information furnished in “outward taxable supplies (zero rated)” column in GSTR 3B

f) EGM error : avoid EGM error by filling it electronically and not manually

How to rectify errors ?

- In case of delay of refund, exporters may contact jurisdictional customs authorities to check the errors committed in furnishing information in GST return.

- In next tax period, rectification can be done in amendment section in GSTR – 1.

- Complaints can be posted on GST portal under Grievance / Complaints section.

*Note : Above procedure is prescribed only for export of goods and not for export of services

Case 2 : Manual process of refund in other cases

Other cases to be discussed here are :-

(a) Refund of IGST paid on export of services and

(b) Refund of IGST paid on supply of goods or services (both) to SEZ units or SEZ developers with payment of tax

(* Cases other than above will be covered in part II. However, manual procedure to be followed in other cases is similar to procedure mentioned for Zero rated supplies.)

Format of “Form GST RFD 01-A” has been prescribed under notification 55/2017 – Central Tax dt. 15th November, 2017. Applicant needs to create application in the said format on common portal and then print out of the said form shall be submitted with the jurisdictional tax authority to which the taxpayer has been assigned.

Documentary evidences :

| Sr. no. | Refund claim on account of | Documentary evidences required |

| 1 | IGST paid on export of goods | a. A statement containing the number and date of shipping bills or bills of export

b. No. and date of relevant export invoices |

| 2 | IGST paid on export of services | a. A statement containing the number and date of invoices

b. Bank Realization Certificates or Foreign Inward Remittance Certificates |

| 3 | IGST paid on supply of goods to SEZ units or SEZ developers | a. A statement containing the number and date of invoices

b. Evidence that such goods have been admitted in full SEZ for authorised operation as endorsed by specified officer of the zone |

| 4 | IGST paid on supply of services to SEZ units or SEZ developers | a. A statement containing the number and date of invoices

b. Evidence regarding receipt of services for authorised operation as endorsed by specified officer of the zone c. Details of payment, alongwith proof, made by recipient to the supplier |

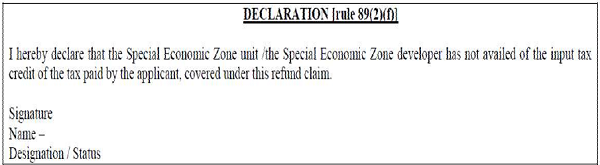

* In 3rd and 4th case above, a declaration to the effect that SEZ unit or SEZ developer has not availed the input tax credit of the tax paid by supplier of goods or services or both is also required as follows :

Refund claims of less than Rs. 2 lakhs :-

As per section 54(4)(b) of CGST Act, 2017, applicant shall furnish documentary evidences to establish that incidence of tax or interest, of which refund is claimed, has not been passed on to any other person.

However, as per proviso to the said section, in case amount of refund claim is less than Rs. 2 lakhs, it shall not be necessary for the applicant to furnish any documentary and other evidences but he may file a declaration, based on the documentary or other evidences available with him, certifying that the incidence of such tax and interest had not been passed on to any other person.

Hello sir,

I have applied for the claim of refund but the adjudicated authority has rejected the claim of refund on the ground that the service provider & the recipient are in the nature of employer employee relationship.Can appeal for the same and claim the refund on the same basis.Will be highly obliged if you do the needful