Manish Goel

Major Amendments made in Income Tax post 8th Nov 2016 and Pradhan Mantri Garib Kalyan Yojana Rules, 2016–

1. Income-tax (30th Amendment) Rules, 2016:

a. Entry number 10 has been revised in table of Rule 114B and now requires every person to quote his PAN in all documents pertaining to transaction‑

Cash deposits with Bank/ Cooperative Bank/ Post Office‑

i. exceeding fifty thousand rupees (Rs. 50,000) during any one day; or

ii. aggregating to more than two lakh fifty thousand rupees (rs. 2,50,000) during the period 09th November 2016 to 30th December 2016.

b. New entry (Number 12) has been added in Rule 114E which requires Bank/ Cooperative Bank/ Post Master General, to furnish statement of financial transaction (on or before the 31st day of January 2017) for‑Cash deposits during the period 09th November 2016 to 30th December 2016 aggregating to‑

i. twelve lakh fifty thousand rupees (Rs. 12,50,000) or more, in one or more current account of a person; or

ii. two lakh fifty thousand rupees (Rs. 2,50,000)or more, in one or more accounts (other than a current account) of a person.

NOTE: Public is advised in self-interest to adhere to the above conditions and limits to avoid inconvenience and chances of an issue of notice from income tax department.

2. The CBDT notified the Income-tax (6th Amendment) Rules, 2016 which came into force on the 1st day of April 2016 had inserted new Income Tax Rule 8AA relating to “Method of determination of the period of holding of capital assets in certain cases”. A new sub-rule 3 has been inserted by Income-tax (34th Amendment) Rules, 2016 which says that in the case of a capital asset, declared under the Income Declaration Scheme 2016, being an immovable property (like land and building), the period for which such property is held shall be reckoned from‑

i. the date on which such property is acquired if the date of acquisition is evidenced by a deed registered with any authority of a State Government;

ii. in any other case, the period for which such asset is held shall be reckoned from the 1st day of June 2016.

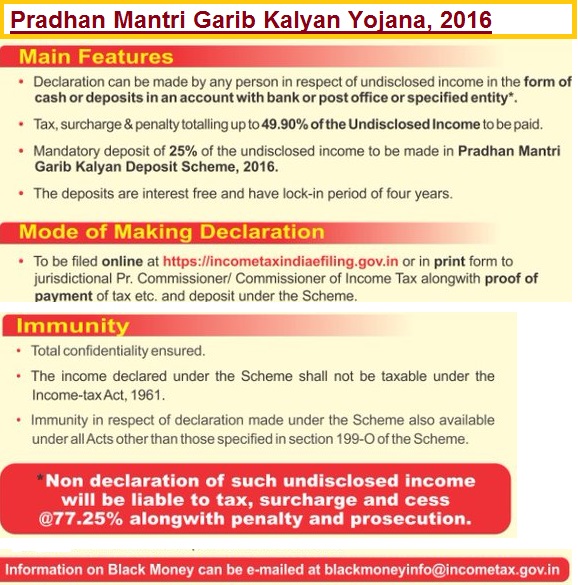

3. Scheme of Taxation and Investment Regime for Pradhan Mantri Garib Kalyan Yojana Rules, 2016‑

i. It shall come into force on the 17th day of December 2016 and shall be valid till 31st day of March 2017.

ii. The deposit under this Scheme shall be made by any person who intends to declare undisclosed income under section 199C(1) of the Taxation and Investment Regime for Pradhan Mantri Garib Kalyan Yojana, 2016.

iii. The deposits shall be accepted at all the authorised banks notified by Government of India in multiples of rupees one hundred.

iv. The deposits shall be held to the credit of the declarant in Bonds Ledger Account maintained with Reserve Bank of India.

v. Section 199F(1) requires declarants to deposit at least 25% of the amount of their Undisclosed Cash Deposits in the Pradhan Mantri Garib Kalyan Deposit Scheme, 2016 wherefrom no withdrawals shall be permitted for 4 years and whereon no interest shall be paid.

vi. The entire deposit to be made under section 199F(1) under this Scheme shall be made, in a single payment, before filing the declaration under section 199C(1).

vii. The deposit shall be made in the form of cash or draft or cheque or by electronic transfer and shall be drawn in favour of the authorised bank accepting such deposit.

viii. An application for the deposit under this Scheme shall be made in Form II clearly indicating the amount, full name, Permanent Account Number, Bank Account details (for receiving redemption proceeds), and address of the

ix. If the declarant does not hold a PAN, he shall apply for a PAN and provide the details of such PAN application along with acknowledgement number.

x. The declaration shall be furnished to the Commissioner, notified under section 199G(1),‑

a. electronically under digital signature; or

b. through transmission of data electronically under electronic verification code; or

c. in print form.

xi. If any person, having furnished a declaration, discovers any omission or any wrong statement therein, he may furnish a revised declaration.

Illustration‑

A declaration of Undisclosed Cash Deposit of Rs. 5,00,000/- shall be treated in the following manner:

| S. No. | Particulars | Amount (Rs.) |

| (a) | Undisclosed Cash Deposit | 5,00,000

|

| (b) | Deposit in Deposit Scheme – In terms of section 199F[(a) * 25%] [Lock-in period of 4 years without interest thereon] | 1,25,000 |

| (c) | Balance available for payment of Penal Tax and for use [(a) – (b)] | 3,75,000 |

| (d) | Tax on (a) @ 30% – In terms of section 199D(1) [(a) * 30%] | 1,50,000

|

| (e) | Pradhan Mantri Kalyan Cess (i.e. surcharge) on (a) @ 33% of tax – In terms of section 199D(2) [(d) * 33%] | 50,000

|

| (f) | Penalty on (a) @ 10% – In terms of section 199E [(a) * 10%] | 50,000 |

| (g) | Penal Tax [(d) + (e) + (f)] | 2,50,000 |

| (h) | Balance available for immediate use [(c) – (g)] | 1,25,000 |

Therefore, we could say after paying 50% penal tax on undisclosed cash deposit and 25% being put in the deposit scheme for a period of four years without any interest, only 25% of the undisclosed cash deposit shall be available to the declarants for immediate use. However, since no interest is being received on 25% deposited with bank, effective cost to the money would be around 58% instead of 50% of penal interest only.