Prabhakar K S*

Introduction

Introduction

The provisions relating to tax treatment of cash credit are given in Section 68.

As per said section, any sum found credited in the books of a taxpayer, for which he offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, may be charged to income-tax as the income of the taxpayer of that year.

Conditions

From the reading of section 68, following conditions can be stated to attract the applicability of section 68:

1. Assessee has maintained ‘books’;

2. There has to be credit of amounts in the books maintained by the taxpayer of a sum during the year;

3. The taxpayer offers no explanation about the nature and source of such credit found in the books

4. The explanation offered by the taxpayer in the opinion of the Assessing Officer is not satisfactory.

5. If the taxpayer is a closely held company and the sum so credited consists of share application money, share capital, share premium or any such amount by whatever name called, any explanation offered by such company shall be deemed to be not satisfactory, unless:

- the person, being a resident in whose name such credit is recorded in the books of such company, also offers an explanation about the nature and source of such sum so credited; and

- such explanation in the opinion of the Assessing Officer has been found to be satisfactory.

If all the above conditions exist, sum so credited may be charged to tax as income of the taxpayer of that year.

In addition to section 68, similar provisions are designed under section 69, 69A, 69B, 69C and 69D in respect of certain other items.

The relevant provisions in this regard, in brief, are as follows:

| Section | Relevant Provisions – In Brief |

|

69 |

Unexplained investments – Where the taxpayer has made investments which are

– Not recorded in the books of account, if any, maintained by him for any source of income, – Offers no explanation about the nature and source of the investments or – The explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory – Same may be deemed to be the income of the taxpayer of such year. |

|

69A |

Unexplained money, etc. – Where the taxpayer is found to be the owner of

– Any money, bullion, jewellery or other valuable article, – Such money, bullion, jewellery or valuable article is not recorded in the books of account, and – The taxpayer offers no explanation about the nature and source of the same, or – The explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, – Same may be deemed to be the income of the taxpayer for such year. |

|

69B |

Amount of investments, etc., not fully disclosed in books of account – Where the taxpayer has made investments or found the owner of

– Any bullion, jewellery or other valuable article, and – If it exceeds the amount recorded in the books of account maintained by the taxpayer, – The taxpayer offers no explanation about such excess amount or – The explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, – Same may be deemed to be the income of the taxpayer for such year. |

|

69C |

Unexplained expenditure, etc. – Where in any year the taxpayer has incurred

– Any expenditure and he offers no explanation about the source of such expenditure – Explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, – Same may be deemed to be the income of the taxpayer for such year. Unexplained expenditure shall not be allowed as a deduction under any head of income. |

|

69D |

Amount borrowed or repaid on hundi – Where any amount – Is borrowed on a hundi from, or any amount due thereon – Is repaid to any person otherwise than through an account payee cheque drawn on a bank, – The amount so borrowed or repaid shall be deemed to be the income of the person borrowing or – Repaying such amount. – Same may be treated as income for the year in which it was borrowed or repaid, as the case may be. However, if any amount borrowed on a hundi has been treated as income of any person by virtue of said section, than such person shall not be liable to be assessed again in respect of the same amount on repayment thereof. Amount repaid shall include the amount of interest paid on the amount borrowed. |

–

|

Section |

Provisions @ Present |

Proposed amendment by The Taxation Laws (Second Amendment) Bill, 2016[ w .e. f – 01.04.2017 ] |

|

115BBE |

As per section 115BBE, where the total income of a taxpayer includes

– Any income referred to in section 68/69/69A/69B/69C/ 69D, – The income-tax payable shall be the aggregate of— a. At the rate of 30% (plus surcharge & cess as applicable); and b. The amount of tax payable on other income at the rates applicable to such other income. |

As per section 115BBE, where the total income of a taxpayer includes

– Any income referred to in section 68/69/69A/69B/69C/ 69D, & reflected in in the return of income furnished U/s. 139 OR – Determined by the Assessing Officer includes any income referred to section 68/69/69A/69B/69C/69D, if such income is not covered under the above clause – – The income-tax payable shall be the aggregate of— a. At the rate of 60% (plus surcharge & cess as applicable); [ Approx. 75% ] and b. The amount of tax payable on other income at the rates applicable to such other income. |

|

Besides, Section 115BBE(2) starts with a non-obstante clause stating that notwithstanding anything contained in the Act, NO DEDUCTION IN RESPECT OF ANY EXPENDITURE OR ALLOWANCE SHALL BE ALLOWED to the Assessee. |

||

Our comments:

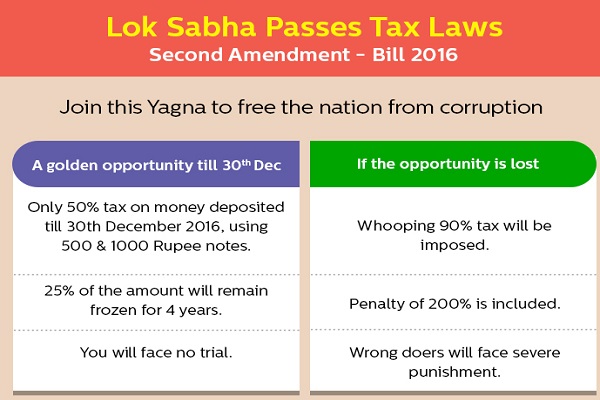

An Assessee can deposit his unaccounted cash into the bank and declared it as a current year’s income in next year’s tax return i.e. next Assessment year 2017-18. So the Assessee can pay the requisite tax at the rate of 30 percent plus surcharge plus cess under Section 115BBE and escape the penalty.

To set right this anomaly, the proposed amendment, increases the tax rate under Section 115BBE to 65 percent plus applicable surcharge & cess [Approx. 75 percent].

Besides, the Department can levy penalty under Section 271AAC at 10 percent on the tax, taking the outgo up to about 85 percent.

It is also proposed to bring a new Income Declaration Scheme called ‘Taxation and Investment Regime for Pradhan Mantri Garib Kalyan Yojana, 2016. Under this scheme, a declarant shall be required to pay 30 % tax of the undisclosed income, and penalty at 10% of the undisclosed Income.

Further, a surcharge called “Pradhan Mantri Garib Kalyan Cess at the rate of 33% of tax is also proposed to be levied. In addition to tax, surcharge and penalty (totaling to approx. 50%), the declarant shall have to deposit 25% of the undisclosed income in a Deposit Scheme to be notified by the RBI under the “Pradhan Mantri Garib Kalyan Deposit Scheme, 2016”. An assessee, who declares his undisclosed income under the said scheme, will get immunity from Direct Tax Laws & many other laws except Money Laundering, Corruption and Benami Property Transactions Acts

Conclusion:

The Government has reduced the taxes to incentivize the people to declare their undisclosed income as it also leads many advantages for government as well, such as reduction in additional manpower, resources and less litigation.

Since “The Taxation Laws (Second Amendment) Bill, 2016’ presented as a Money Bill in Lok Sabha, approval of Rajya Sabha does not arise. Once, period of 14 days – as prescribed by our Constitution – lapsed from the date of its receipt in Rajya Sabha, inevitably, the Bill will be sent to the President for His assent and same will be notified. In this case, the 14 days, will be 14th December, 2016.

Reference:

- The Taxations Laws (Second Amendment) Bill, 2016 – Bill No 299 of 2016

- Taxmann’s Income Tax Act, as amended by Finance Act, 2016, 60th Edition

- A N Aiyar’s Indian Tax Laws – 2016, as amended by Finance Act, 2016, 53rd Edition

- Direct Taxes – Laws & Practice by Dr. Girish Ahuja & Dr. Ravi Gupta, as amended by Finance Act, 2016, 7th Edition

- Kanga & Palkhivala’s – The Law and Practice of Income Tax – Volume II, Tenth Edition

* The Author is a budding tax law professional and may be reached at shreetaxchambers @ bsnl.in