Case Law Details

Clarion Agro Products Private Limited Vs ACIT (ITAT Hyderabad)

Hyderabad ITAT: Wrong Section Mentioned (69 Instead of 69A) Doesn’t Invalidate Addition; Section 153D Approval Protected by New Section 292BC

Summary: The Hyderabad ITAT partly allowed the assessee’s appeal for statistical purposes in a search assessment. The Tribunal upheld the addition of ₹67,43,098 relating to excess cash found during the search, holding that mentioning Section 69 instead of Section 69A did not invalidate the addition since the nature of the addition as unexplained cash remained unchanged, and the CIT(A)’s correction of the applicable provision neither enhanced the assessment nor violated principles of natural justice. The Tribunal also rejected the challenge to the validity of approval under Section 153D, observing that, after the retrospective insertion of Section 292BC, technical defects such as absence of DIN, clerical discrepancies or advisory observations in the approval did not invalidate it. On merits, the Tribunal found the assessee’s explanation regarding the source of excess cash unsupported by contemporaneous records and documentary evidence and upheld the addition. However, regarding the addition of ₹5,83,932 on account of alleged stock shortage, the Tribunal restored the matter to the Assessing Officer for fresh examination after considering work-in-process, manufacturing loss, quantitative details and supporting evidence, with an opportunity of hearing to the assessee.

The Hyderabad ITAT partly allowed the assessee’s appeal for statistical purposes in a search assessment involving unexplained cash and stock variation. The Tribunal upheld the addition of ₹67.43 lakh towards excess cash found during search, holding that merely quoting section 69 instead of section 69A is a curable mistake, as the substance of the addition was clearly for unexplained cash. The CIT(A)’s correction of the applicable provision did not amount to enhancement or violate principles of natural justice. The Tribunal also upheld the validity of the approval under section 153D, observing that after the retrospective insertion of section 292BC by the Finance Act, 2026, technical defects such as absence of DIN, clerical errors or alleged insufficiency of reasons do not invalidate such administrative approvals. However, on the addition relating to alleged stock shortage, the Tribunal restored the matter to the Assessing Officer for fresh examination, directing consideration of work-in-process, manufacturing loss and supporting quantitative records before deciding the issue.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal is filed by Clarion Agro Products Private Limited (“the assessee”), feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals)-11, Hyderabad (“Ld. CIT(A)”) dated 03.01.2025 for the A.Y. 201920.

2. At the outset, it was noticed that there was a delay of 24 days in filing the present appeal before the Tribunal. In support of the condonation of delay, the assessee has filed a petition for condonation along with an affidavit explaining the reasons which prevented the assessee from filing the appeal within the prescribed period of limitation.

3. We have considered the contents of the condonation petition and the affidavit filed by the assessee. Having regard to the reasons stated therein, the fact that the delay involved is only 24 days, and there being no serious objection from the Revenue for condonation of such delay, we are satisfied that the assessee was prevented by sufficient cause from filing the appeal within the stipulated period. Accordingly, in the interest of substantial justice, the delay of 24 days in filing the appeal is condoned and the appeal is admitted for adjudication on merits.

4. The assessee has raised the following grounds of appeal:

1) That the Learned Commissioner (Appeals) erred in sustaining the addition of Rs. 67,43,098/- made u/s 69 by Assessing Officer by treating the cash found in the search and seizure operation as Unexplained.

2) That the Learned Commissioner (Appeals) erred in rejecting the explanation of Appellant for source of Cash found in the Search.

3) Without prejudice to above, the Learned Commissioner (Appeals) erred in invoking the provision of Section 69A to sustain the addition made u/s 69 without giving an opportunity of being heard to Appellant before invoking the provision of Section 69A.

4 That the Learned Commissioner (Appeals) erred in confirming the addition of Rs. 5,83,932/- made towards alleged Unaccounted Sales.

5) That without prejudice to above Grounds, the Assessment Order passed u/s 143(3) r/w Section 153A is bad in law as the approval given u/s 153D for passing such Order was not in accordance with law which renders the approval and the Assessment Order Invalid.

That the Appellant craves leave to add, alter or substitute any Grounds of Appeal.

Hyderabad

Date: 20.06.2025

Appellant:

Ronak Gupta, Director

5. The brief facts of the case are that the assessee is a company engaged in the business of manufacturing and trading of wheat flour. A search and seizure operation under section 132 of the Income-tax Act, 1961 (“the Act”) was carried out in the case of M/s Jitender Roller Flour Mills Group on 02.05.2018. The premises of the assessee were also covered under the search operation. The assessee filed its return of income for Assessment Year 2019-20 on 24.12.2019 declaring total income of Z1,08,96,640/- under the normal provisions of the Act and book profit of Z1,10,53,717/- under section 115JB of the Act. The case of the assessee was selected for scrutiny and notice under section 143(2) of the Act, dated 24.09.2020 was issued by the Learned Assessing Officer (“Ld. A.0”). During the course of search proceedings, cash of 279,80,500/- was found at the business premises of the assessee. However, the cash balance as per books of account on the date of search was Z12,37,402/-. Accordingly, excess cash of Z67,43,098/- was found over and above the cash balance reflected in the books of account. During the assessment proceedings, the Ld. A.0 called upon the assessee to explain the source of the excess cash. Not being satisfied with the explanation furnished by the assessee, the Ld. AO treated the excess cash of Z67,43,098/-as unexplained income under section 69 of the Act. Further, excess stock valued at 25,83,932/- was also found during the course of search and the same was added by the Ld. AO in the hands of the assessee. Accordingly, the Ld. AO completed the assessment under section 143(3) of the Act vide order dated 26.04.2021 making addition of Z67,43,098/- under section 69 of the Act on account of excess cash and addition of 25,83,932/- on account of excess stock.

6. Aggrieved by the assessment order, the assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT(A) confirmed both the additions made by the Ld. AO and dismissed the appeal of the assessee.

7. Aggrieved by the order of the Ld. CIT(A), the assessee is in further appeal before the Tribunal. At the outset, the Learned Authorized Representative (“Ld. AR”) submitted that under Ground No. 5 of the appeal the assessee has raised a legal issue regarding the validity of approval granted under section 153D of the Act. Inviting our attention to the copy of approval granted under section 153D of the Act placed at page no.140 of the paper book, the Ld. AR raised various objections regarding the validity of the approval. The first objection of the assessee is that no DIN has been mentioned in the approval granted under section 153D of the Act. It was submitted that absence of DIN renders the approval invalid and consequently the assessment order passed on the basis of such approval is liable to be quashed. In support of this contention, reliance was placed on the decision of the Hon’ble Bombay High Court in the case of Sanjay Nathalal Shah Vs. ACIT reported in 182 com 847, the decision of the Amritsar Bench of the Tribunal in the case of Shreeji Bihariji Colonisers Vs. ACIT in ITA Nos. 48 & 49/ASR/2023 for A.Ys. 2018-19 and 2019-20 dated 22.07.2024 and the decision of the Delhi Bench of the Tribunal in the case of Arun Kumar Mittal Vs. ACIT in ITA No. 2970/Del/2022 for AY 2019-20 dated 20.12.2023.

7.1 The Ld. AR further submitted that the approval letter contains factual errors, inasmuch as it refers to additional income as per return filed under section 153A of the Act whereas, in fact, it was the addition proposed in the draft assessment order. It was submitted that such factual inaccuracies demonstrate complete non-application of mind by the approving authority.

7.2 It was further argued that the approving authority has not made any reference to the assessment records examined by him before granting approval and therefore the approval has been granted mechanically without application of mind.

7.3 The Ld. AR also submitted that para no. 3 of the approval letter demonstrates that the approval granted under section 153D of the Act is conditional in nature. In support of the said proposition, reliance was placed on the decision of the Raipur Bench of the Tribunal in the case of Nimesh Patel Vs. DCIT in ITA No. 74/RPR/2019 for A.Y. 2015-16 dated 09.04.2024, the decision of the Delhi Bench of the Tribunal in the case of Mainee Steel Works Pvt. Ltd. Vs. DCIT in ITA Nos. 3371 to 3377/Del/2024 dated 24.01.2025 and the decision of the Delhi Bench of the Tribunal in the case of Rishabh Buildwell Pvt. Ltd. & Others Vs. DCIT in ITA Nos. 2122, 2163, 2123, 2162, 2124 and 2491/Del/2018 dated 04.07.2019. Accordingly, it was submitted that the approval granted under section 153D of the Act is invalid and consequently the assessment order passed pursuant thereto deserves to be quashed.

8. Per contra, the Learned Departmental Representative (“Ld. DR”) strongly supported the orders of the lower authorities. The Ld. DR submitted that after insertion of section 292BC by the Finance Act, 2026 with retrospective effect from 1.4.2021, technical defects in approvals granted by income-tax authorities stand cured and such approvals cannot be invalidated merely on account of technical infirmities. It was submitted that approvals granted under section 153D of the Act are administrative and supervisory in nature. Therefore, non-mentioning of DIN, factual mistakes in the approval note or absence of detailed discussion cannot invalidate the approval in view of the specific provisions contained in section 292BC of the Act. As regards the contention of the assessee regarding conditional approval, the Ld. DR submitted that para no. 3 of the approval letter merely contains advisory observations. The approving authority has not stated that the approval is being granted subject to fulfilment of any condition. It was submitted that the use of the word “may” clearly indicates that the observations are recommendatory in nature and not mandatory. Accordingly, it was argued that the approval granted under section 153D of the Act is a valid approval and the legal ground raised by the assessee deserves to be rejected.

9. We have heard the rival submissions and perused the material available on record including the case laws relied upon. The assessee, vide Ground No. 5, has challenged the validity of approval granted under section 153D of the Act. The first objection of the assessee is that the approval granted under section 153D of the Act does not contain any DIN and therefore the approval itself is invalid. We have carefully gone through the judicial precedents relied upon by the assessee. We find that all the decisions relied upon by the assessee were rendered prior to the insertion of section 292BC of the Act by the Finance Act, 2026 w.e.f. 1.4.2021. In this regard, we have gone through the provisions of section 292BC of the Act, which is to the following effect:

“Circumstances in which approvals by income-tax authority not to be invalid.

292BC. Notwithstanding anything contained in this Act or in any judgment, order or decree of any Court, for the removal of doubts, it is hereby clarified that any approval given by an income-tax authority in relation to any assessment, reassessment or re-computation proceedings under this Act shall be deemed to be administrative and supervisory in nature and shall not be invalid or shall not be deemed to be invalid by reason of any insufficiency of the reasons recorded or by reason of any defect in the form or manner of its authentication or communication including whether digital signature have been appended to such approval or not, where such approval is granted electronically.”

9.1 On perusal of the provisions of section 292BC of the Act, we find that the legislature has clarified that any approval, sanction or consent granted by an income-tax authority in relation to any assessment, reassessment or re-computation proceeding under the Act shall be deemed to be administrative and supervisory in nature and shall not be regarded as invalid merely by reason of any insufficiency of reasons recorded or by reason of any defect in the form, manner of authentication or communication thereof. Thus, the legislature has specifically provided that technical defects in the form, authentication or communication of an approval granted by an income-tax authority shall not invalidate such approval. Therefore, in view of the retrospective amendment brought by insertion of section 292BC of the Act w.e.f. 1.4.2021, we are unable to accept the contention of the assessee that mere non-mentioning of DIN in the approval granted under section 153D of the Act would render such approval invalid.

9.2 The assessee has also pointed out certain factual discrepancies in the approval letter, namely, reference to additional income as per return filed under section 153A of the Act instead of addition proposed in the draft assessment order and absence of specific reference to assessment records. In our considered opinion, these objections also relate to the form and manner in which the approval has been recorded and communicated. In view of the specific provisions of section 292BC of the Act, such technical or clerical defects cannot invalidate the approval granted under section 153D of the Act.

9.3 The assessee has further contended that the approval granted under section 153D of the Act is conditional in nature. In this regard, we have gone through para no. 3 of the approval letter placed at page no. 140 of the paper book, which is to the following effect:

3. Asst. record in 1 volumes returned herewith. Applicability of tax rates u/s 115BBE, penalty proceedings u/s 270A and 271AAC may please be checked before passing order.

9.4 On perusal of the above, we find that the approving authority has stated that applicability of tax rate under section 115BBE of the Act and initiation of penalty proceedings under sections 270A and 271 AAC of the Act “may please be checked before passing the order”. In our considered opinion, the aforesaid observation does not make the approval conditional. The approving authority has nowhere stated that the approval is being granted subject to fulfilment of the aforesaid observations. Further, the use of the expression “may please be checked” clearly indicates that the observations are advisory in nature and not mandatory. The approving authority has neither directed reconsideration of the additions proposed in the draft assessment order nor withheld the grant of approval pending verification of any issue. The observations merely relate to consequential matters concerning applicability of tax rate and penalty proceedings. It is not the case of the assessee that after the approval under section 153D of the Act, there is any change in the final assessment order passed by the Ld. AO as compared to the draft assessment order which require fresh approval under section 153D of the Act. Therefore, the same cannot be construed as conditions precedent for grant of approval under section 153D of the Act. We have also gone through the decisions relied upon by the assessee in the cases of Nimesh Patel Vs. DCIT (supra), Mainee Steel Works Pvt. Ltd. Vs. DCIT (supra) and Rishabh Buildwell Pvt. Ltd. & Others Vs. DCIT (supra). On perusal of the said decisions, we find that those decisions were rendered in the backdrop of facts where the directions issued by the approving authority were found to be conditional in nature and the approval itself was held to be dependent upon fulfilment of such conditions. However, in the present case, we do not find that the approval granted by the approving authority is based upon any condition. As discussed hereinabove, the observations contained in para no. 3 of the approval letter are merely advisory in nature and do not affect the grant of approval itself. Therefore, the reliance placed by the assessee upon the aforesaid decisions is misplaced and the ratio laid down therein does not apply to the facts of the present case. Accordingly, we hold that the approval granted under section 153D of the Act cannot be regarded as conditional merely because of the aforesaid observations contained in para no. 3 of the approval letter. In view of the foregoing discussion, we do not find any merit in the legal objections raised by the assessee regarding the validity of approval granted under section 153D of the Act. Accordingly, Ground No. 5 raised by the assessee is dismissed.

10. The Ld. AR submitted that Ground No. 3 of the appeal is a legal ground challenging the action of the Ld. CIT(A) in changing the section under which the addition of Z67,43,098/- was sustained. The Ld. AR submitted that the Ld. AO had made addition of 267,43,098/- on account of excess cash found during the course of search under section 69 of the Act. However, the Ld. CIT(A), without providing any opportunity of being heard to the assessee, treated the said addition as falling under section 69A of the Act. It was submitted that the addition made by the Ld. AO under section 69 of the Act is not sustainable in law, as excess cash, if at all taxable, could only be brought to tax under section 69A of the Act. It was further submitted that the Ld. CIT(A) could not have changed the section without providing an opportunity of hearing to the assessee. Accordingly, it was contended that the addition of Z67,43,098/- is liable to be deleted.

11. Per contra, the Ld. DR relied upon the orders of the lower authorities and submitted that the Ld. AO has clearly recorded that the addition pertains to unexplained cash found during the course of search. Merely because the Ld. AO has mentioned section 69 instead of section 69A, the addition cannot be deleted when the nature of the addition is otherwise clearly identifiable from the assessment order.

12. We have heard the rival submissions and perused the material available on record. The grievance of the assessee is that the Ld. AO has made addition of Z67,43,098/- under section 69 of the Act whereas the Ld. CIT(A) has treated the same as an addition falling under section 69A of the Act. In this regard, we have carefully gone through para nos. 3 to 3.6 of the assessment order, which is to the following effect:

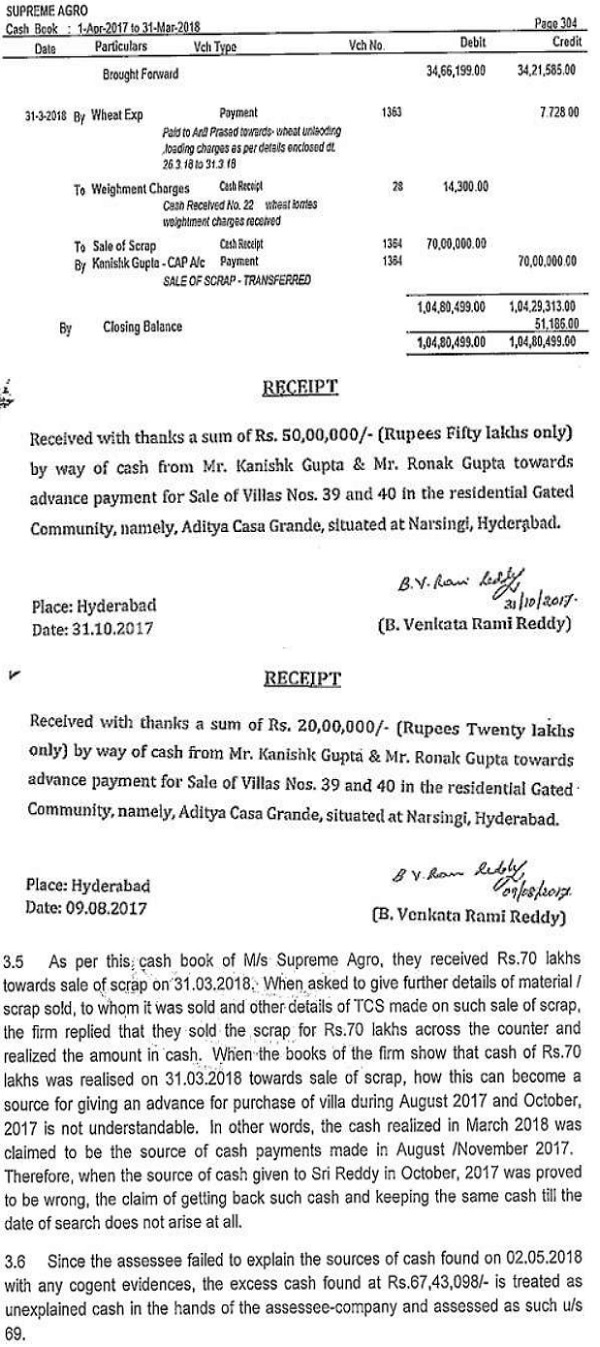

3.2 The issue was put before the assessee during the course of hearings. In response, the assesses submitted that the Directors of the assessee company are also partners in a firm Ws Supreme Agro, running from 14-220, S.No.842/1, Patancheru, Medak and cash of Rs.70 lakhs was realised towards scrap sale in the firm; the above cash was paid by them to Sri B. Venkat Rami Reddy of Sri Aditya Constructions towards advance against purchase of two villas; Sri Reddy returned the cash in view of new provisions of Income Tax Act placing restrictions on receiving cash and that the returned cash was found during the course of search on 02.05.2018.

3.3 Before going into the submissions of the assessee, it is in place to refer to the time frame of the above happenings, which were conveniently not brought out by the assessee. If the dates are added to the above submissions, it can be seen that the Directors of the assessee-company, as partners of a firm, Ws Supreme Agro sold scrap and realised Rs.70.00 lakhs on 31.03.2018, paid Rs.70.00 lakhs on two different dates, i.e., 09.08.2017(Rs.20 lakhs) and 31.10.2017(Rs.50.00 lakhs) to Sri Reddy towards advance of villa, got the cash back during November, 2017 and kept the money with them till the date of search.

3.4 Though the above lines do not give a clear understanding of the submissions of the assessee, to make it clear, relevant page of the cash book of M/s Supreme Agra and the cash advance receipts are scanned hereunder:

13. On perusal of the above, we find that the Ld. AO has categorically recorded that during the course of search, excess cash amounting to 267,43,098/- was found at the business premises of the assessee over and above the cash balance reflected in the books of account. Thus, the nature of the addition made by the Ld. AO is clearly that of unexplained money found in possession of the assessee. No doubt, the Ld. AO has referred to section 69 of the Act while making the addition. However, it is evident from the discussion contained in the assessment order that the addition pertains to unexplained cash found during the course of search, which is otherwise covered by the provisions of section 69A of the Act. Therefore, the mistake committed by the Ld. AO is only with regard to quoting of the section and not with regard to the nature of the addition itself. It is a settled proposition of law that mere quoting of a wrong provision does not invalidate an action if the authority otherwise possesses the jurisdiction and the action is otherwise sustainable in law. The Hon’ble Supreme Court, in various decisions, has recognized the principle that substance must prevail over form and that mere technical mistakes should not defeat substantive justice. Applying the aforesaid principle to the facts of the present case, we are unable to accept the contention of the assessee that the addition is liable to be deleted merely because the Ld. AO has mentioned section 69 instead of section 69A of the Act.

13.1 As regards the contention of the assessee that the Ld. CIT(A) changed the section from section 69 to section 69A without granting an opportunity of hearing, we do not find any merit in the same. The Ld. CIT(A) has merely corrected the provision applicable to the facts already recorded by the Ld. AO. The nature of the addition, quantum of addition and basis of addition remained unchanged. No new source of income has been introduced by the Ld. CIT(A), nor has the addition been enhanced. Therefore, we do not find that any prejudice has been caused to the assessee on account of such correction. In our considered opinion, correction of the applicable section by the Ld. CIT(A) in the peculiar facts of the present case does not amount to enhancement of assessment nor does it result in violation of the principles of natural justice. Therefore, we reject the contentions advanced by the assessee. Accordingly, the Ground No. 3 raised by the assessee is dismissed.

14. The Ld. AR submitted that Ground Nos. 1 and 2 of the appeal relate submission of the assessee on merits with regard to the addition of Z67,43,098/- made on account of excess cash found during the course of search. The Ld. AR submitted that the excess cash found from the premises of the assessee-company did not belong to the assessee but belonged to Shri Kanishk Gupta, Managing Director of the assessee company. In this regard, our attention was invited to para no. 3.4 of the assessment order wherein the Ld. AO has reproduced the cash book of M/s Supreme Agro for 31.03.2018 and the receipts issued by Shri B. Venkata Rami Reddy. It was submitted that Shri Kanishk Gupta was also a partner in M/s Supreme Agro. During the relevant period, M/s Supreme Agro had received cash of 270,00,000/- on sale of scrap. Out of the said amount, Shri Kanishk Gupta had withdrawn 270,00,000/- in cash from M/s Supreme Agro. Thereafter, Shri Kanishk Gupta advanced 250,00,000/- on 31.10.2017 and 220,00,000/- on 09.08.2017 to Shri B. Venkata Rami Reddy as advance for purchase of Villas Nos. 39 and 40 situated at Aditya Casa Grande, Narsingi, Hyderabad. It was further submitted that the proposed purchase transaction did not materialize and consequently Shri B. Venkata Rami Reddy refunded the advance amount of 270,00,000/- to Shri Kanishk Gupta. Accordingly, it was contended that the excess cash found during the course of search represented the amount refunded by Shri B. Venkata Rami Reddy to Shri Kanishk Gupta and therefore the same could not be treated as unexplained cash belonging to the assessee-company. Accordingly, the Ld. AR submitted that the entire source of cash stood explained and therefore the addition of Z67,43,098/- deserves to be deleted.

15. Per contra, the Ld. DR strongly relied upon the orders of the lower authorities. The Ld. DR first submitted that if the cash actually belonged to Shri Kanishk Gupta in his individual capacity, there was no explanation as to why the same was found from the business premises of the assessee-company. The Ld. DR invited our attention to para no. 3.4 of the assessment order reproduced herein above, wherein the Ld. AO has reproduced the cash book of M/s Supreme Agro for 31.03.2018. It was pointed out that M/s Supreme Agro had recorded receipt from sale of scrap and withdrawal of 270,00,000/- by Shri Kanishk Gupta on 31.03.2018. However, the advances allegedly given to Shri B. Venkata Rami Reddy were stated to have been made on 09.08.2017 and 31.10.2017, i.e., much prior to the date on which the cash withdrawal was recorded in the books of M/s Supreme Agro. It was therefore submitted that if the entries recorded in the books of M/s Supreme Agro are accepted as correct, Shri Kanishk Gupta did not have the cash in hand on the dates on which advances were allegedly made to Shri B. Venkata Rami Reddy. Thus, the entire explanation furnished by the assessee becomes factually impossible. The Ld. DR further submitted that if the assessee’s contention is accepted that the sale of scrap and withdrawal of cash had actually taken place earlier but were recorded in the books only on 31.03.2018, the same would be equally unbelievable because M/s Supreme Agro was maintaining a closing cash balance of only 251,186/- and it is difficult to accept that cash transactions aggregating to 270,00,000/- were omitted from the books for several months and recorded only at the year end.

15.1 The Ld. DR further submitted that no documentary evidence whatsoever has been produced by the assessee to establish that Shri B. Venkata Rami Reddy had actually refunded the alleged advance amount of 270,00,000/- to Shri Kanishk Gupta. It was submitted that mere production of receipts evidencing payment of advance cannot establish receipt back of the said amount.

15.2 The Ld. DR also pointed out that out of the excess cash of Z67,43,098/-, cash of Z17,43,098/- was found with the cashier of the assessee-company. Therefore, even on facts, it is difficult to accept that the personal cash of Shri Kanishk Gupta was lying with the cashier of the company.

15.3 Lastly, the Ld. DR invited our attention to Question No. 9 of the statement of Shri Kanishk Gupta recorded on 03.05.2018 during the course of search placed at page no. 51 of the paper book. It was submitted that in the statement recorded immediately after the search, Shri Kanishk Gupta had accepted the excess cash as undisclosed income of the assessee-company. Therefore, the subsequent explanation furnished by the assessee is only an afterthought devised to explain the excess cash found during the course of search.

Accordingly, the Ld. DR submitted that the addition made by the Ld. AO deserves to be sustained.

16. We have heard the rival submissions and perused the material available on record. The issue involved in Ground Nos. 1 and 2 relates to the addition of Z67,43,098/- made on account of excess cash found during the course of search. The primary contention of the assessee is that the excess cash belonged to Shri Kanishk Gupta and represented the amount refunded by Shri B. Venkata Rami Reddy against advances earlier given for purchase of villas. In this regard, we have carefully gone through para no. 3.4 of the assessment order, which is reproduced herein above, wherein the Ld. AO has reproduced the cash book of M/s Supreme Agro for 31.03.2018 and the receipts relied upon by the assessee. On perusal of the same, we find that the advances of 250,00,000/- and 220,00,000/- were stated to have been given by Shri Kanishk Gupta to Shri B. Venkata Rami Reddy on 31.10.2017 and 09.08.2017 respectively. However, the cash withdrawal of 270,00,000/- by Shri Kanishk Gupta from M/s Supreme Agro has been recorded in the books only on 31.03.2018. Thus, the advances are stated to have been made much prior to the date on which the cash withdrawal has been recorded in the books of M/s Supreme Agro. Therefore, the contention of the assessee that Shri Kanishk Gupta withdrew cash from M/s Supreme Agro and thereafter advanced the same to Shri B. Venkata Rami Reddy is not supported by the contemporaneous records and cannot be accepted. We also find considerable force in the contention of the Revenue that if the entries recorded in the books of M/s Supreme Agro are accepted as correct, Shri Kanishk Gupta did not possess the cash on the dates on which advances were allegedly made. On the other hand, if it is assumed that the withdrawal and sale of scrap had actually taken place earlier and were recorded only on 31.03.2018, such explanation is equally difficult to accept. M/s Supreme Agro was maintaining a closing cash balance of merely Z51,186/ – and it is improbable that cash transactions aggregating to 270,00,000/- would remain unrecorded for several months and be accounted for only at the end of the financial year. The circumstances clearly indicate that the entries relied upon by the assessee are only after-thought entries brought on record to explain the excess cash found during the course of search.

16.1 We further find that though the assessee has produced evidence regarding payment of advances to Shri B. Venkata Rami Reddy, no evidence whatsoever has been produced to establish that the said advances were subsequently refunded by Shri B. Venkata Rami Reddy to Shri Kanishk Gupta. No receipt, confirmation, bank record or any other documentary evidence evidencing return of cash has been placed on record. Therefore, the very foundation of the explanation advanced by the assessee remains unsupported by any credible evidence.

16.2 We also find merit in the contention of the Revenue that if the cash was the personal cash of Shri Kanishk Gupta, there is no satisfactory explanation as to why such cash was found from the business premises of the assessee-company. More importantly, cash amounting to Z17,43,098/- was found with the cashier of the assessee-company. This fact further weakens the explanation that sought to be advanced by the assessee.

16.3 We have also gone through the reply given by Shri Kanishk Gupta to the Q. No. 9 in his statement recorded on 03.05.2018 during the course of search, which is to the following effect:

“Q.9. 1 am showing you the page number 1 in the folder containing loose sheets seized vide Annexure A/ CAPPL/ OFF/ 01 containing cash balance statement as on 2 May, 2018 of Rs. 12,37,402/ -. However, we have found the cash of Rs.79,80,500/ -.Please explain the sources of cash of Rs.50,00,04/ -found in the locker kept in your chamber and Rs.29,30,500/ – found in the almirah of your cashier Sti Dasarath, Also Explain the excess cash found in your office premises.

Ans. I accept that the amount of Rs. 50,00,000/ -found in the locker kept in my chamber is an old undisclosed business income. I also accept that the amount of Rs.17,43,098/ -kept in the almirah of Sri Dasarath is an old undisclosed business income.”

16.4 On perusal of the above, we find that Shri Kanishk Gupta accepted the excess cash found during the course of search and offered the same as undisclosed income of the assessee-company. It is a settled proposition that a statement made at the first available opportunity carries substantial evidentiary value, as at that stage there is little scope for manipulation or fabrication of facts. The explanation subsequently advanced by the assessee is not supported by any independent evidence and appears to be an afterthought.

16.5 Considering the entirety of facts and circumstances of the case, the contemporaneous statement of Shri Kanishk Gupta, the absence of any evidence regarding refund of cash by Shri B. Venkata Rami Reddy, the inconsistencies in the cash flow explanation and the location from which the cash was found, we are unable to accept the explanation furnished by the assessee as genuine and credible. Therefore, we uphold the addition of Z67,43,098/- made by the Ld. AO and sustained by the Ld. CIT(A). Accordingly, Ground Nos. 1 and 2 raised by the assessee are dismissed.

17. Ground No. 4 of the assessee relates to the addition of 25,83,932/- made on account of alleged shortage of stock. The Ld. AR submitted that during the course of search proceedings, certain shortage in physical stock as compared to the stock as per books of account was noticed by the Revenue Authorities in respect of wheat and bran. However, excess stock was found in respect of Rawa, Atta and Maida. The Ld. AO adjusted the excess quantity against the shortage quantity and arrived at a net shortage of 31.77 metric tons. Thereafter, the Ld. AO valued the said shortage at the rate of Z18.38 per kilogram and made an addition of 25,83,932/- in the hands of the assessee. The Ld. AR submitted that the assessee is engaged in the business of manufacturing Rawa, Atta and Maida from wheat and, therefore, it is a common phenomenon in such line of business that a portion of stock remains at different stages of the manufacturing process. It was further submitted that while conducting stock verification, the Revenue Authorities failed to consider the quantity of stock lying in the manufacturing process. The Ld. AR further submitted that the shortage of 31.77 metric tons constitutes only about 0.044% of the total production of the assessee and such variation is attributable to normal process loss and wastage occurring during the manufacturing activity. It was contended that considering the nature of the assessee’s business, the impugned shortage is insignificant and represents a normal business occurrence. Accordingly, it was prayed that the addition made by the Ld. AO and sustained by the Ld. CIT(A) be deleted.

18. Per contra, the Ld. DR, supported the orders of the lower authorities. It was submitted that the assessee failed to substantiate its claim with any documentary evidence, quantitative records or scientific working regarding the alleged process loss, wastage or stock lying in the manufacturing process. It was contended that mere oral submissions without supporting evidence cannot be accepted. Accordingly, the Ld. DR prayed that the addition made by the Ld. AO be sustained.

19. We have heard the rival submissions and perused the material available on record. The undisputed facts are that during the course of search proceedings, the Revenue Authorities found shortage in the physical stock of wheat and bran as compared to the stock reflected in the books of account. Simultaneously, excess stock was found in respect of Rawa, Atta and Maida. The Ld. AO adjusted the excess quantity against the shortage quantity and determined a net shortage of 31.77 metric tons. The said shortage was valued at Z18.38 per kilogram and an addition of 25,83,932/- was made in the hands of the assessee. We find merit in the submissions of the Ld. AR that in a manufacturing concern engaged in the production of Rawa, Atta and Maida, some quantity of stock normally remains in the manufacturing process and certain wastage is also common and inevitable during the course of production. Therefore, while examining any variation in stock, the effect of work-in-process as well as normal manufacturing loss is required to be considered. The contention of the assessee that the impugned shortage constitutes only about 0.044% of the total production also deserves examination. At the same time, we find that the assessee has not placed on record any documentary evidence, quantitative reconciliation, stock records or working demonstrating the extent of process loss, manufacturing wastage and stock lying in the manufacturing process. In the absence of such supporting material, the claim of the assessee cannot be accepted merely on the basis of oral submissions. Considering the totality of the facts and circumstances of the case, we are of the view that the issue requires fresh examination at the end of the Ld. AO. Accordingly, we set aside the orders of the lower authorities on this issue and restore the matter to the file of the Ld. AO with a direction to re-adjudicate the addition of 25,83,932/- after providing adequate opportunity of being heard to the assessee. The assessee shall substantiate its claim regarding process loss, manufacturing wastage and stock lying in the manufacturing process by furnishing necessary documentary evidence, quantitative details and supporting workings. The Ld. AO shall examine the same and decide the issue afresh in accordance with law. Accordingly, Ground No. 4 of the assessee is allowed for statistical purposes.

20. In the result, the appeal of the assessee is partly allowed for statistical purposes.

Order pronounced in the Open Court on 8th July, 2026.

Author Bio