Case Law Details

Soham Techno Cast Vs ITO (ITAT Rajkot)

The appeal before the ITAT Rajkot arose from the order of the Commissioner of Income Tax (Appeals) dated 27.09.2025, which had affirmed the assessment order passed by the Assessing Officer under Section 147 read with Section 144 of the Income-tax Act for Assessment Year 2016-17. The assessee challenged the reopening of the assessment, the validity of approvals and notices issued under Sections 148 and 148A, the addition of Rs. 34,30,995 under Section 69A, the application of Section 115BBE, initiation of penalty proceedings under Section 271AAC(1), and levy of interest under various provisions.

According to the material on record, the assessee had filed a return declaring income of Rs. 26,220. The Assessing Officer noted cash deposits of Rs. 34,30,995, including Rs. 25,30,995 deposited during the demonetisation period, which were considered disproportionate to the returned income. As the assessee did not comply with notices issued under Section 148A(b), the Assessing Officer treated the cash deposits as unexplained. Following the Supreme Court’s judgment in Union of India v. Ashish Agarwal, the earlier notice under Section 148 was treated as a notice under Section 148A(b), material was supplied to the assessee, an order under Section 148A(d) was passed, and a fresh notice under Section 148 was issued. The assessee requested that the earlier return be treated as the return filed in response to the notice under Section 148. Thereafter, notices under Sections 143(2) and 142(1) were issued.

The Assessing Officer specifically called upon the assessee to explain the source of the cash deposits of Rs. 34,30,995. Show cause notices were issued, but the assessee did not comply. The assessment was completed based on the available material, and the entire amount of Rs. 34,30,995 was added as unexplained money under Section 69A and subjected to taxation under Section 115BBE. The Commissioner (Appeals) confirmed the assessment, leading to the present appeal before the Tribunal.

Before the Tribunal, the assessee primarily challenged the validity of the reassessment proceedings. It was submitted that the original notice under Section 148 had been issued on 20.04.2021 and that the notice under Section 148A(b) dated 25.05.2022 itself showed that the alleged escaped income represented by an undisclosed asset was below Rs. 50 lakh. Since the reassessment had been initiated after the expiry of three years from the end of Assessment Year 2017-18, the assessee contended that the reassessment proceedings were liable to be quashed. The Revenue relied on the reasoning adopted by the Assessing Officer.

The Tribunal examined Section 149 of the Income-tax Act governing the time limit for issuance of notices under Section 148. It observed that the relevant assessment year was 2017-18, that the original notice under the unamended law had been issued on 20.04.2021, the notice under Section 148A had been issued on 25.05.2022, and the notice under the amended provisions of Section 148 had been issued on 15.07.2022. The Tribunal noted that where more than three years have elapsed from the end of the relevant assessment year, the extended limitation under Section 149(1)(b) is available only if the income escaping assessment amounts to or is likely to amount to Rs. 50 lakh or more. In the present case, the alleged escaped income was Rs. 34,30,995, which was below the statutory threshold.

The Tribunal relied on the decision in Ganesh Dass Khanna v. ITO [2023] 156 taxmann.com 417 (Delhi), which held that where the alleged escaped income was below Rs. 50 lakh, reassessment notices issued after expiry of the three-year limitation could not be sustained, even after the decision in Union of India v. Ashish Agarwal. Applying that reasoning, the Tribunal held that the notice dated 15.07.2022 could not avail the extended limitation period under Section 149, as the alleged escaped income was only Rs. 34,30,995. It held that the reassessment proceedings were barred by limitation, the initiation of reassessment was wholly without jurisdiction, and accordingly quashed the reassessment proceedings.

Having quashed the reassessment proceedings, the Tribunal held that all other issues relating to the additions on merits had become academic and infructuous. The assessee’s appeal was accordingly allowed.

Cases Discussed:

- Ganesh Dass Khanna v. ITO [2023] 156 taxmann.com 417 (Delhi).

- Union of India v. Ashish Agarwal [2022] 138 taxmann.com 64/286 Taxman 183/444 ITR 1 (SC).

FULL TEXT OF THE ORDER OF ITAT RAJKOT

Captioned appeal filed by the assessee, pertaining to Assessment year 201617, is directed against the order passed by the Learned Commissioner of Income Tax (Appeals) vide order dated 27.09.2025, which in turn arises out of an order passed by the Assessing Officer under Section 147 r.w.s. 144, of the Act, dated 16.05.2023.

2. The grounds of appeal raised by the assessee are as follows:

“1. That, the Ld. AO has wrongly re-opened the assessment u/s 147 of the I.T Act, 1961, a) The approval granted by Ld. PCIT u/s 151 of the Act is mechanical in nature, b) The reopening is initiated without complying with the provisions of section 149(1)(a) of the Act c)The Ld. AO has reopened the assessment without quantifying the escapement of income, d) Assessment is reopened based on borrowed satisfaction and without application of mind, e) The Ld. AO has failed to obtain separate approval for issuing notice u/s 148A(b) of the Act, f) The notice u/s 148 of the Act is issued without Document Identification Number.

2. That, the notice issued u/s 143(2) of the Act dated 01/05/2023 is in violation of CBDT instruction F. No. 225/157/2017/ITA-II dated 23.06.2017.

3. That, the Ld. AO has wrongly made addition of Rs.34,30,995/- on account of unexplained money u/s 69A of the I.T. Act, 1961.

4. That, the Ld. AO has wrongly applied the provision of section 115BBE of the I.T. Act, 1961.

5. That, the Ld. AO has wrongly initiated penalty proceedings u/s 271AAC(1) of the I.T. Act, 1961

6. That, the Ld. AO has wrongly charged the interest u/s 234A, 234B, 234C, 234D and 244A of the I.T. Act, 1961.

7. That, the findings of the Ld. Assessing Officer are not 7 justified and are bad-in-law.

8. The appellant craves to add, amend, alter and DLEETE any of the above ground of appeals.”

3. The relevant material facts, as culled out from the material on record, are as follows. The assessee has filed his return of income for assessment year (A.Y.) 2017-18, on 04.11.2017, declaring income of Rs.26,220/-. The huge amount of transaction, that is, cash deposited of Rs. 34,30,995/- (including Rs.25,30,995/-deposited during demonetization period) do not commensurate with returned income filed by the assessee for the year under consideration. The assessee has not complied with the notices issued u/s 148A(b) of the Act. In absence of any submission in compliance to notices, the source of credits appearing in the bank accounts either by way of cash deposit and/or other credit remains undisclosed and unexplained. Therefore, it is clear that the following financial transactions remained unexplained:

| Bank Name | Account No. | Mode of deposit | Amount (in Rs.) |

| Dena Bank | 3013024021 | Cash | Rs.34,30,995/- |

| Total | Rs.34,30,995/- |

Subsequently, the Hon’ble Supreme Court vide judgment dated 04.05.2022 (2022 SCC Online SC 543), in the case of Union of India vs Ashish Agarwal has adjudicated on the validity of the issue of reassessment notices issued by the Assessing Officers during the period beginning on 1st April, 2021 and ending with 30th June 2021, within the time extended by the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020. The Hon’ble Supreme Court has held that these notices issued under the old law shall be deemed to be the show cause notices issued under clause (b) of section 148A of the new law and has directed the Assessing Officers to follow the procedure with respect to such notices. Accordingly, in view of the order dated 04.05.2022 of the Hon’ble Supreme Court, the above mentioned notice issued u/s 148 of the Income Tax Act, 1961 in the case of assessee, is deemed to be Show Cause Notice u/s 148A (b) of the Income Tax Act, 1961, for the said Assessment Year and the information and material in possession of assessing officer was provided to the assessee, on dated 30.05.2022, on the basis of which assessment / reassessment proceedings were initiated u/s 147 of the Income Tax Act, 1961 and consequently the above mentioned notice u/s 148 of the Income Tax Act, 1961, was issued to the assessee. As per the mandate given in the Judgment of the Hon’ble Supreme Court in the case cited as above, the assessee was given 2 weeks’ time to explain the transactions corresponding to the abovementioned information and material along with supporting documentary evidence and to explain that these do not represent income that has escaped assessment, for the above mentioned assessment year, under the new provisions of section 147 of the Income Tax Act. On the basis of information order u/s 148A (d) was passed on 14.07.2022 in the case of assessee and notice u/s 148 was issued. In response to the notice under section 148 referred to above, the assessee had sent a communication to the assessing officer dated 20.01.2023, saying that the return filed on 21.05.2021, for the Assessment Year 2017-18 may be treated as return filed in response to notice under section 148 of the Act. Therefore, the same is treated as filed in compliance of notice u/s 148 referred to above. Accordingly, notices u/s 143(2)/ 142(1) of I.T. Act, 1961 were issued to the assessee.

4. On the basis of information, the order u/s 148A(d) of the Act was passed in the case of assessee and notice u/s 148 was issued 14.07.2023. Accordingly, notices u/s 142(1) of I.T. Act, 1961 were issued to the assessee. In compliance to the notice under section 142(1) of the I.T. Act, the assessee has filed reply dated 20.01.2023. The assessee was specifically required to furnish explanation on the issue of cash deposited of Rs. 34,30,995/- (including Rs.25,30,995/- deposited during demonetization period). Show cause notice was also issued on 08.05.2023 to the assessee to furnish explanation regarding to explain source of cash deposit to the tune of Rs. 34,30,995/- (including Rs.25,30,995/- deposited during demonetization period). Again show cause notice was also issued on 08.05.2023 to the assessee to furnish explanation regarding to explain source of cash deposit to the tune of Rs. 34,30,995/- (including Rs.25,30,995/- deposited during demonetization period). However, the assessee failed to comply the show cause notice dated 08.05.2023. Therefore, the assessment was completed on the basis of facts of the case and material available on record. The assessing officer noted that assessee failed to submit source of cash deposit. Therefore, considering the facts of the case and information available, Rs. 34,30,995/- was treated as unexplained and unaccounted income of assessee. Accordingly, Rs. 34,30,995/- was added to the income of assessee u/s 69A of I.T. Act, 1961 as unexplained money read with section 115BBE of the Act.

5. Aggrieved by the order of the Assessing Officer, the assessee carried the matter in appeal before the Ld. CITA, who has confirmed the action of the Assessing Officer, therefore assessee is in further appeal before this Tribunal.

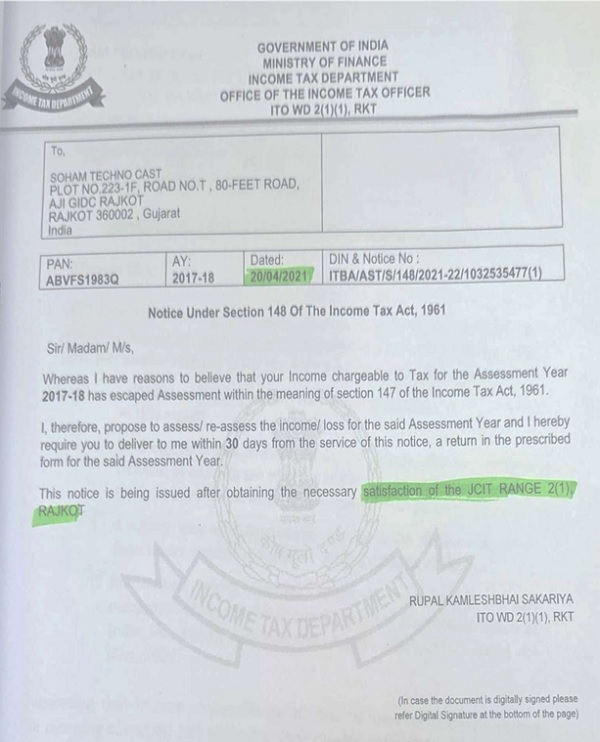

6. Learned Counsel for the assessee challenged the reopening of assessment under section 147 of the Act stating that original notice under section 148 of the Act was issued on 20.04.2021, which is reproduced below:

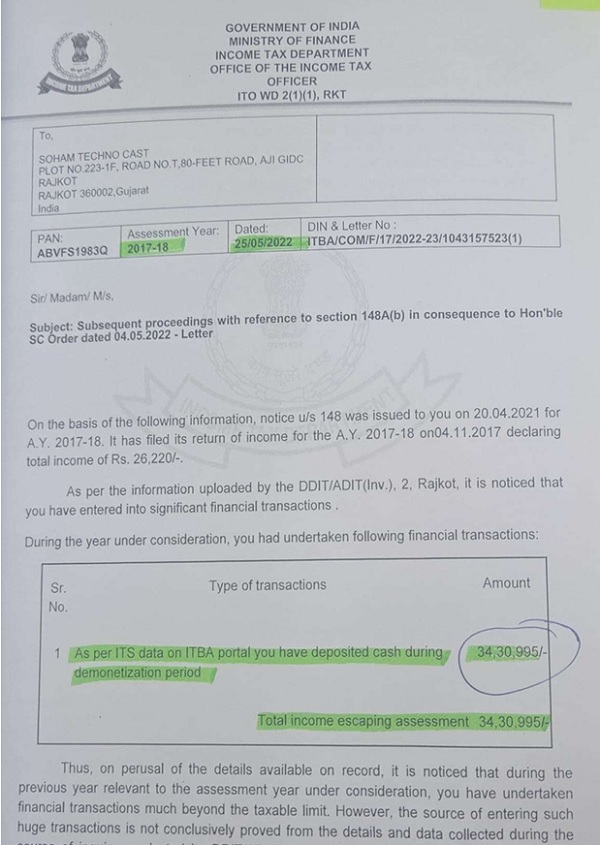

7. The learned Counsel for the assessee submitted that notice under section 148A (b) of the Act was issued on 25.05.2022, which is reproduced below:

–

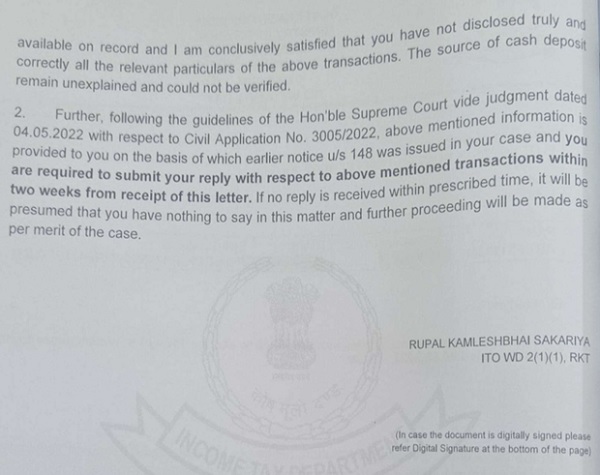

The ld. Counsel submitted that on perusal of the notice u/s 148A(b) of the Act dated 25/05/2022, it can be stated that income escapement represented by undisclosed asset is below Rs. 50 lacs and reopening is carried out after the end of three years from the end of assessment year (AY) 2017-18. Therefore, reassessment proceedings may be quashed.

8. On the other hand, the Ld. DR for the Revenue has primarily reiterated the stand taken by the Assessing Officer, which we have already noted in our earlier para and is not being repeated for the sake of brevity.

9. I have heard both the parties and carefully gone through the submission put forth on behalf of the assessee along with the documents furnished and the case laws relied upon, and perused the fact of the case including the findings of the ld 7 CIT(A) and other materials brought on record. I note that reopening of assessment under section 147 of the Act is initiated without complying with the provisions of section 149(1)(a)(b) of the Act. In the assessee’s case the relevant assessment year (AY) under consideration is A.Y. 2017-18. The notice u/s 148 of the Act has been issued under unamended Act on 20/04/2021. The copy of notice is enclosed at page no. 38 of the paper book and the same is reproduced above. The notice u/s 148A of the Act has been issued on 25/05/2022, and the same is reproduced above. The notice u/s 148 of the Act dated 15/07/2022 has been issued under the amended Act, the copy of notice is enclosed at page no. 39 of paper book. I find that in order to reopen the assessment under section 147 of the Act, after a period of three years, the income escaped from assessment should be more than Rs.50,00,000/-, however, in the assessee’s case, the income escaped from assessment is only Rs.34,30,995/- therefore, jurisdiction exercised by the assessing officer to reopen the assessment of the assessee is not valid, as the income escaped from assessment is only Rs. Rs.34,30,995/-, which is below Rs. 50,00,000/- hence, reassessment proceedings initiated against the assessee under section 147 of the Act should be quashed. In this regard, it is appropriate to examine the provision of section 149 of the Act with respect to time limit for issuance of notice u/s 148 of the Act, which is reproduced below:

“Time limit for notice

149. (1) No notice under section 148 shall be issued for the relevant assessment year, –

(a) if three years have elapsed from the end of the relevant assessment year, unless the case falls under clause (b);

(b) if three years, but not more than ten years, have elapsed from the end of the relevant assessment year unless the Assessing Officer has in his possession books of account or other documents or evidence which reveal that the income chargeable to tax, represented in the form of-

(i) an asset

(ii) expenditure in respect of a transaction or in relation to an event or occasion; or

(iii) an entry or entries in the books of account,

which has escaped assessment amounts to or is likely to amount to fifty lakh rupees or more.

10. From the above, it is vivid that Section 149(1) of the Act mandates that no notice u/s 148 would be issued for the relevant assessment year if three (03) years have elapsed from the end of the said assessment year. The AO can take recourse to the extended limitation period if the conditions precedent prescribed in clause (b) of sub-section (1) of section 149 are fulfilled. Therefore, where three (03) years from the end of the relevant assessment year have elapsed, the AO can issue a notice u/s 148 provided the conditions prescribed in clause (b) of section 149(1) of the amended 1961 Act are fulfilled. As per clause (b) of section 149 one of the conditions for triggering the extended period of 10 years in cases where 3 years has lapsed is that income chargeable to tax which has escaped assessment amounts to, or is likely to amount to Rs. 50 lakhs or more for the assessment year in consideration, where in the assessee case under consideration, the amount has escaped from assessment is Rs.34,30,995/- only, therefore, reassessment proceedings, should be quashed, for this reliance is placed on decision in the case of Ganesh Dass Khanna v. ITO [2023] 156 taxmann.com 417 (Delhi), wherein it was held as follows:

“Section 149, read with sections 148 and 148A, of the Income-tax Act, 1961 and section 3 of the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 and Article 142 of the Constitution of India, 1950- Income escaping assessment – Time limit for issuance of notice – Assessment years 2016-17 and 2017-18 – A notice dated 28-6-2021 under unamended section 148 was issued upon assessee in respect of relevant assessment year 2017-18-Similarly, a notice dated 30-6-2021 under unamended section 148 was issued upon assessee in respect of relevant assessment year 2016-17-Pursuant to judgment of Supreme Court in case of Union of India v. Ashish Agarwal [2022] 138 taxmann.com 64/286 Taxman 183/444 ITR 1 (SC), revenue issued another notice under section 148A(b) dated 20-5-2022 for assessment year 2017-18-Assessee contended that reassessment proceedings triggered against it were time-barred as limitation period of three years qua relevant assessment years had expired – Whether reassessment notice issued on or after 1-4-2021 under unamended section 148 would be deemed to have been issued under substituted section 148A(b) and revenue could not have issued another notice under section 148A(b) for assessment year 2017-18 Held, yes Whether, further, since concededly, in instant case, alleged escaped income was less than Rs. 50 lakhs, impugned notices issued between 1-4-2021 and 30-6-2021, by which time limitation of three years under-section 149(1)(a) had already expired, these notices were barred by limitation Held, yes Whether, consequently, orders passed under section 148A(d) and consequent notices issued under section 148 concerning both assessment years could not be sustained Held, yes [Paras 54] [In favour of assessee]”

11. Accordingly, the impugned notice, u/s 148 of the Act is dated 15/07/2022. Further, the said notice is for alleged escaped income of Rs.34,30,995/-, which is less than Rs. 50,00,000/- and thus, the said notice cannot take the benefit of extended period of limitation which is beyond three years till ten years. Thus, the impugned notice dated 15.07.2022, issued under Section 148, is barred by the limitation period prescribed under Section 149 of the Act therefore, the proceedings are wholly without jurisdiction, in as much as, notice under Section 148 of the I.T Act, 1961 is normally three years from the end of the relevant assessment year and extendable beyond 3 years till 10 years provided the income which has escaped assessment is Rs. 50,00,000/- or more and the permission of the concerned authority is taken and in the instant case it is evident from the notice, which clearly indicates that the alleged income, which has escaped assessment, is only Rs. 34,30,995/-, therefore, it is quite evident that the alleged income, which has escaped assessment, is only Rs. 34,30,995/-, thus, I do not have hesitation in holding that the very initiation of reassessment proceeding is wholly without jurisdiction, therefore, I quash the reassessment proceedings.

12. In view of the reasons set out above, as also bearing in mind entirety of the case, I am of the considered view that the reasons recorded by the Assessing Officer, as set out earlier, were not sufficient reasons for reopening the assessment proceedings. Therefore, I have quashed the reassessment proceedings. As the reassessment itself is quashed, all other issues on merits of the additions, in the impugned assessment proceedings, are rendered academic and infructuous.

13. In the result, appeal of the assessee, is allowed in above terms.

Order is pronounced in the open court on 22/06/2026.

Author Bio