Summary: A Hindu Undivided Family (HUF) is described as a separate legal and taxable entity under the Income Tax Act that enables legal income splitting and long-term wealth management by treating the family independently from its members. An HUF can own property, earn income, make investments, and claim tax benefits separately, with the Karta managing its affairs and coparceners, including daughters by birth, having equal rights to seek partition, while wives of coparceners are members but not coparceners. Hindu, Buddhist, Sikh, and Jain families with at least two members may form an HUF, including upon marriage. HUFs are taxed using the same slabs as individuals under the Old and New Tax Regimes, irrespective of residential status, although resident senior citizen slab benefits do not apply and rebate is available only to resident individuals, not HUFs. The HUF has a separate basic exemption limit of Rs. 2.5 lakh under the Old Tax Regime and Rs. 4 lakh under the New Tax Regime (FY 2025-26), and may claim deductions under Sections 80C, 80D, 80G, home loan interest deductions, and capital gains exemptions under Sections 54, 54F and 54EC. The content notes that HUF tax planning requires family harmony, long-term vision and professional structuring.

Introduction: A Hindu Undivided Family (HUF) is a powerful and fully legal tax-saving structure under Indian income tax law. It helps in income splitting and long-term wealth management by treating the family as a separate taxable entity.

- HUF is treated as a separate “person” from its members for tax purposes.

- Income can be legally split between individual members and the HUF, reducing overall tax liability.

- HUF can claim deductions under Section 80C, 80D, and capital gains exemptions, just like an individual.

- Enjoys a separate basic exemption limit: – ₹2.5 lakh under the Old Tax Regime – ₹4 lakh under the New Tax Regime

What is an HUF?

HUF stands for Hindu Undivided Family. It is a separate legal entity recognized under the Income Tax Act, created specifically for tax purposes.

An HUF is one of the most effective and fully legal tax-saving structures available to joint families.

An HUF can:

- Own property

- Earn income

- Make investments

- Claim tax benefits independently of its members

This helps families reduce their overall tax liability by legally splitting income between individuals and the HUF. The head of the HUF is called the Karta, and the family members are known as coparceners.

Who Can Form an HUF?

- Hindu, Buddhist, Sikh, and Jain families are all eligible to form an HUF.

- An HUF cannot be created by a single person — a minimum of two members is required.

- There must be a family with lineal ascendants and descendants.

- An HUF can also come into existence upon marriage.

Who Are the Members of an HUF?

An HUF consists of a common ancestor and all lineal descendants, including their wives and unmarried daughters.

Karta

- The head of the HUF, usually the senior-most male or female member.

- Manages the HUF’s financial and legal affairs.

- Has unlimited liability, including for tax obligations.

Coparceners

- All male and female lineal descendants of the common ancestor.

- Daughters are coparceners by birth with equal rights.

- Have the right to demand partition of HUF property.

Other Members

- Wives of coparceners become members after marriage.

- They are not coparceners.

- Have maintenance rights but cannot demand partition.

Important Note:

Only coparceners can seek partition of an HUF, while the Karta bears unlimited liability for HUF dues, including taxes.

HUF Tax Slabs:

- HUF taxation is similar to individual taxation, with minor differences.

- Tax slabs for HUF are the same as for individuals under both: – Old Tax Regime – New Tax Regime

The tax slabs remain the same whether the HUF is Resident or Non-Resident, under both regimes.

Note:

Relaxed slab rates available for resident senior & super senior citizens are not applicable to HUF. Surcharge and cess will be applicable as per prevailing rates.

Rebate – Important Clarification

It is a common misconception that HUFs can claim rebate if taxable income is:

- below ₹7 lakh (New Regime)

- below ₹5 lakh (Old Regime)

- below ₹12 lakh (New Regime for FY 2025-26)

Reality:

Rebate is NOT available to HUFs.

Rebate can be claimed only by Resident Individuals, not HUFs.

HUF Tax Benefits (Still Powerful!)

HUF is treated as a separate taxable person, different from its members.

Hence, separate tax slabs & deduction limits apply.

Income can be legitimately split between members and HUF, helping reduce overall family tax liability.

Basic Exemption Limit:

Old Regime: ₹2.5 lakh

New Regime (FY 2025-26): ₹4 lakh

Key Tax Benefits Available to HUF

Section 80C – Deduction up to ₹1.5 lakh PPF, ELSS, Life Insurance, etc.

Section 80D – Deduction on health insurance premium paid for HUF members

Section 80G – Deduction on eligible donations made by HUF

Home Loan Benefits – Deduction on interest paid on housing loan

Capital Gains Exemptions – Relief under Sections 54, 54F & 54EC on reinvestment of long-term capital gains.

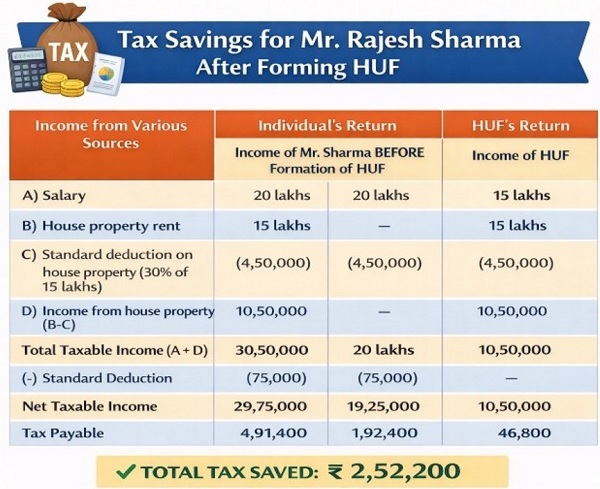

How to Save Taxes by Forming an HUF?

Let’s understand HUF taxation with a simple example

Bottom Line: HUF is powerful for tax planning, But needs family harmony, long-term vision & professional structuring

A Hindu Undivided Family (HUF) is a separate legal and tax entity under Indian income tax laws, consisting of a common ancestor and lineal descendants. An HUF has its own PAN, tax slabs, and deduction limits, enabling legal income splitting and tax optimisation. It can earn income from assets, investments, and capital gains, though salary income cannot be routed through an HUF.

*******

Disclaimer: This information is for general awareness only. Tax treatment may vary based on individual circumstances. Please consult for detailed and personalized advice.