SEBI’s consultation paper proposes a comprehensive overhaul of the investor consent framework and conflicted transaction provisions under the Alternative Investment Funds (AIF) Regulations, 2012. It seeks to standardize consent processes by allowing AIFs to adopt one of three methodologies—deemed consent, present and voting, or express voting—subject to uniform disclosures, documented policies, and consistent application at the scheme level. The paper also proposes a uniform approval threshold of 75% of unitholders by value wherever investor consent is required, enhancing clarity and protecting minority investors. To strengthen governance, AIF managers would be required to ensure transparency, maintain records, and provide equal voting opportunities. On conflicted transactions, SEBI proposes replacing the narrow concept of “associate” with a broader “related party” definition, largely based on the Companies Act, 2013, for conflict-related provisions while retaining “associate” elsewhere. These reforms aim to improve transparency, consistency, operational certainty, and investor protection without unduly restricting legitimate fund operations.

Securities and Exchange Board of India

Consultation paper on rationalizing the requirement of obtaining investor consent and ambit of conflicted transactions requiring investor consent under SEBI (Alternative Investment Funds) Regulations, 2012

SEBI- Jun 30, 2026 | Reports : Reports for Public Comments

Click here to provide your comments

1. Objective

Alternative Investment Funds (AlFs) are investment vehicles meant to channelize the capital of sophisticated investors to companies in need. With an approach to strike a balance between operational and investment flexibility for AlFs, while ensuring that investors are able to make informed decisions, this consultation paper seeks comments and views from the public and stakeholders on the following proposals —

1.1. To standardize the process of obtaining investor consent as per requirements mandated under AIF Regulations, including, for carrying out conflicted transactions;

1.2. To bringing consistency in threshold for unitholder approval prescribed under AIF Regulations and circulars issued thereunder; and,

1.3. To rationalize the ambit of conflicted transactions which would require investor consent, in a manner that aligns with the underlying regulatory intent.

2. Background

2.1. SEBI (Alternative Investment Funds) Regulations, 2012 (AIF Regulations) prescribes that certain material decisions/changes relating to the governance and operations of an AIF, including specified conflicted transactions, shall be carried out only after obtaining requisite investor consent, with varying thresholds for different requirements. The AIF Regulations prescribe different approval thresholds for different matters; however, they do not provide guidance on the manner or methodology for obtaining such consent.

2.2. The AIF Regulations also lay down a framework to address conflicts of interest through fiduciary obligations of the manager and sponsor, coupled with disclosure and investor consent requirements. and transparency requirements. The framework relies primarily on transparency and informed investor participation to manage conflict related issues in view of the nature of the investor base.

2.3. Over time, based on supervisory experience and stakeholder interactions, it has been observed that while the existing framework provides flexibility and operational ease, certain conflict-prone transactions may not be uniformly captured for investor consideration due to the limited scope of entities covered under the current definition of “associate”. This may lead to situations where transactions involving comparable levels of conflict are treated differently, resulting in interpretational uncertainty.

2.4. Further, diverse market practices have emerged with respect to solicitation, voting methodologies, and treatment of non-responses. Additionally, varying approval thresholds prescribed across the regulatory framework, without a clearly articulated rationale, may add to complexity and operational challenges for AIFs and investors alike.

2.5. The proposals in the consultation paper are expected to reduce ambiguity in application of the regulations, and provide AIFs with a clear, predictable and implementable framework for obtaining investor consent and undertaking transactions involving potential conflicts of interest.

3. Standardising the requirement and manner of obtaining investor consent under SEBI (Alternative Investment Funds) Regulations, 2012

Existing regulatory framework for investor consent –

3.1. There are various provisions under AIF Regulations and circulars issued thereunder, wherein requirement of investor consent has been mandated for performing certain material activities / transactions. A list of provisions under AIF Regulations which mandate investor consent is given at Annexure A.

Bringing consistency in threshold for investor consent –

3.2. It may be observed that AIF Regulations mandate different approval thresholds for different activities — mainly consent of 2/3rd or 3/4th (75%) of investors by value of their investment in the fund. As it may be seen, there is no principle based distinction or rationale for requiring different threshold of approval of investors for different activities / transactions under AIF Regulations. Therefore, for the ease of reference, it may be appropriate to have a uniform threshold for investor consent for such activities / transactions.

3.3. Considering that consent of 75% of investors by value would include more investors in decision making, in comparison to consent of 2/3rd of investors by value, the same might be favourable to minority dissenting stakeholders who may otherwise be dragged along in favor of majority opinion. Thus, it would be appropriate to mandate a threshold of 75% unitholder consent (by value) for all such references where 2/3rd investor consent has been mandated. This consistent approach is expected to provide clarity and facilitate ease of operations for AlFs, without compromising on investor protection.

Need for standardization of consent mechanism –

3.4. AlFs have adopted diverse market practices for obtaining investor consent. As a result, identical approval thresholds may yield different outcomes depending on the voting methodology followed by individual funds. Further, divergent market practices may result in disputes or misinterpretation, particularly in situations involving conflicts of interest.

3.5. SEBI has received representation from AIF industry highlighting the following concerns in relation to the voting mechanism adopted for obtaining investor consent mandated under AIF Regulations —

3.5.1. Lack of response from investors:

AIFs are unable to reach the stated approval/consent thresholds due to non-responsiveness of AIF Investors, especially where the fund has a large investor base.

3.5.2. Selective non-voting:

In certain instances, investors intentionally withhold their responses during consent solicitations as a strategic tactic to leverage concessions from the Alternative Investment Fund, such as reduced fees or favourable co-investment terms, etc.

3.6. It is understood that majority of the AlFs adopt deemed consent model for obtaining investor consent, wherein a failure to respond within a specified time period would be deemed as approval for the given proposal. SEBI has observed various instances where funds have treated non-voting by investors as approval for the said proposal, upon disclosure to investors about the deeming their consent in the absence of an explicit response.

3.7. SEBI has also received feedback from AIF investors regarding the lack of consistency in the process of obtaining investor consent. It is understood that few funds have adopted a practice where the manner of obtaining consent differs from investor to investor. That is, while deemed consent is agreed upon for most investors of the fund, certain investors insist on only explicit approval being considered as consent. As a result, the voting mechanism applied differs among investors within the same scheme. Such differential treatment within a single scheme may give rise to concerns relating to fairness, transparency and governance.

3.8. With a view to provide ease of operations, clarity of interpretation by stakeholders, ease of compliance by funds and ease of supervision by SEBI, standardization of investor consent process is seen by industry stakeholders as a pressing need.

3.9. Prescribing a single methodology/procedure for obtaining investor consent may affect the flexibility of operations for AlFs. Therefore, it appears reasonable and balanced that AlFs may be given an option to choose one of the prescribed methodologies for obtaining investor consent, subject to adherence to minimum safeguards and disclosure requirements applicable to the chosen method. The prevalent methodologies for obtaining and calculating investor consent being considered and currently adopted by AIF industry, are discussed in detail in the following paragraphs.

Proposed Methodologies –

3.10. Method A: Deemed consent –

3.10.1. Under this method, the Al F/manager puts forward a proposal for investor consent and provides a fixed timeline for providing their response (consent/dissent) to the proposal. Investors who do not cast their vote/provide any response within the prescribed timeline are treated as having approved the proposal put forward by the AIF/manager. Thus, unless an investor explicitly votes against the proposal within the specified period, such investor is deemed to have approved the proposal.

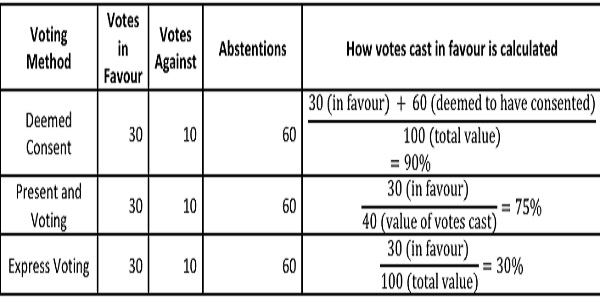

3.10.2. For example, let us consider an AIF with 100 investors, each holding 1% of the fund by value. 30 investors vote in favour of a particular proposal, 10 vote against it and 60 abstain. Under this method, investors who do not cast a vote are deemed to have consented to the proposal, meaning abstentions are treated as votes in favour. The votes in favour are therefore calculated by adding the 30 investors who voted in favour to the 60 who abstained, giving a total of 90 out of 100 investors, or 90% by value.

3.10.3. This method is widely accepted in the industry considering the fact that investors in AIFs are typically institutional investors or high net-worth individuals who are presumed to be sophisticated and capable of evaluating whether participation in the approval process is necessary. In certain cases, it has been submitted by the industry that such investors may consciously choose not to vote. Further, requiring affirmative approval from all or a significant majority of investors may lead to delays in decision-making, particularly in funds with a large investor base as per the feedback received by SEBI. By treating the absence of dissent as approval, this method enables the AIF to act efficiently in the interests of investors who actively participate in the decision-making process.

3.10.4. However, this method also raises concerns from an investor-protection and governance perspective. Treating inaction as approval may result in material or conflicted decisions being implemented without demonstrable and informed investor support. For instance, even if 20% of the investors (by value) express dissent for a proposal and none of the other investors express explicit consent, the proposal would be taken as approved due to deemed consent provision. There is also a risk that investors may overlook communications or fail to respond within the stipulated timeframe, leading to approvals being deemed without their active participation. In the absence of a specific norm/written down agreement, the timeframe is at the discretion of the manager and at times, may be insufficient for the investor to take an informed decision.

3.11. Method B: Present and voting –

3.11.1. Under this approach, only votes actively cast by investors (consent/in favour, dissent/against) are taken into account for determining whether the requisite investor approval threshold has been met. Investors who do not participate in the voting process are treated as having abstained, and such abstentions do not have any bearing on the outcome.

3.11.2. This methodology is consistent with voting practices followed under various other SEBI-regulated investment vehicles, including mutual funds, listed companies, Real Estate Investment Trusts (“REITs”), and Infrastructure Investment Trusts (“InvITs”).

3.11.3. For example, let us consider an AIF with 100 investors, each holding 1% of the fund by value. 30 investors vote in favour of a particular proposal, 10 vote against it and 60 abstain. Under this method, only votes that are actually cast count, and abstentions are excluded. The votes in favour are calculated by dividing the 30 investors who voted in favour by the 40 investors who actually participated in the vote, giving 75% by value of the participating voters.

3.11.4. This method encourages participation of investors in voting process and is adopted widely accepted practices in other SEBI-regulated vehicles. The investors who choose to abstain implicitly defer to the decision of active participants.

3.11.5. It may be argued that matters requiring approval under the AIF Regulations often relate to fundamental aspects of fund governance, conflicted transactions, or material changes to fund operations. In cases where participation levels are low, decisions affecting core attributes of the fund may be approved by a limited subset of investors, potentially giving rise to conflicts of interest or outcomes that may not adequately reflect the interests of non-participating investors.

3.12. Method C: Express voting for approval –

3.12.1. Under this method, a proposal is considered approved only when the value of votes explicitly cast in favour of the proposal, through any mode (digital or physical) facilitated by the AIF manager, meets or exceeds the applicable approval threshold calculated with reference to the total investor value of the fund, irrespective of the level of investor participation. Investors who do not cast a vote within the prescribed timeframe are treated as having neither consented nor dissented. Such non-responding investors reduce the likelihood of the proposal being approved unless a sufficient level of investor participation is achieved.

3.12.2. For example, let us consider an AIF with 100 investors, each holding 1% of the fund by value. 30 investors vote in favour of a particular proposal, 10 vote against it and 60 abstain. Under this method, only explicit votes in favour count, and abstentions do not contribute to approval. The votes in favour are calculated by dividing the 30 investors who voted in favour by all 100 investors in the fund, giving 30% by total value.

3.12.3. This method ensures that approvals for material decisions reflect deliberate and affirmative investor intent. By requiring the approval threshold to be met with reference to the total investor value, this method provides a higher degree of investor protection and reduces the risk of material decisions being implemented without broad-based investor support.

3.12.4. However, practical challenges exist as highlighted by the industry participants, especially in scenarios where investor participation is low or where investor base is large, dispersed or unresponsive. Some important decisions may fail to receive approval even when supported by the majority of participating investors, potentially leading to an inability to implement necessary actions in a timely manner.

3.13. To summarize, the following table captures how votes cast in favour of a proposal is calculated as per the methodologies detailed above.

3.14. All of the aforesaid methodologies for obtaining investor consent have their own set of pros and cons. Considering that AlFs are meant for sophisticated investors, it may be prudent to provide flexibility regarding the methodology for obtaining investor consent, as long as there is adequate disclosure, written down policy and consistent adaption to ensure fairness and transparency to the investors. Thus, the AIF/manager may be provided flexibility to adopt one of these methodologies which best suits their investor base and facilitates operational ease, subject to certain prescribed conditions for each methodology.

3.15. Further, allowing AlFs to adopt different mythology for different investors of the same fund, may result in disproportionate representation of investors in the voting process. Considering the investor consent has been mandated for key/material changes/aspects of AIF operations, it is essential to ensure fair representation of investors in the process of obtaining consent. Thus, AlFs may be allowed to adopt one of the aforesaid methodologies consistently at fund level.

3.16. An agenda in line with the discussion above, was placed for discussion before the Alternative Investment Policy Advisory Committee (‘AIPAC’). AIPAC recommended the agenda considering that it provides flexibility to funds to opt for different methodologies, subject to explicit disclosure and procedures prescribed under laid down policy. Considering the intent to provide ease of compliance and monitoring for AlFs and other stakeholders, the Committee also recommended the proposal to bring consistency in percentage threshold for investor consent by prescribing 75% investor consent (by value), wherever applicable.

Proposals for sideration.

| Proposal | Details |

| Proposal 1.

|

Flexibility in manner of seeking investor consent –AIFs may be given an option to choose one of the following methodologies for obtaining and calculating investor consent for requirements mandated under AIF Regulations and/or in fund documents –

(a) Deemed consent – Votes in favour and lack of response within the specified voting timeline, shall be considered as approval for calculating consent (by value) as against the total value of the fund/scheme of AIF. (b) Present and voting – Votes in favour shall be considered for approval for calculating consent (by value) as against the total number of investors (by value) who participated in the voting process. (c) Express voting for approval – Votes in favour shall be considered for approval for calculating consent (by value) as against the total value of the fund/scheme of AIF. |

| Proposal 2. | Modalities for adopting a methodology for seeking investor consent – |

| 2a. | AIFs shall disclose the chosen methodology with the related policy/procedures for obtaining investor consent, along with the associated risks, in their PPMs. |

| 2b. | This shall include details regarding manner of communication for reaching out to investors, manner of conducting meetings/seeking votes, notice period/voting timeline, reminders for seeking response, etc. |

| 2c. | AIFs shall follow the chosen methodology consistently at the scheme/fund level, i.e., the methodology for obtaining consent shall not differ between investors of the same scheme. |

| Proposal 3. | Modalities for seeking investor consent for a proposal – |

| 3a. | Regardless of the chosen methodology as discussed above, all investors of the fund shall be provided an opportunity to vote on all proposals requiring investor consent. The following shall be disclosed to the investors while seeking their consent: (i) the proposal with rationale; (ii) the relevant regulatory provision/provision in fund documents which triggered the investor consent requirement; (iii) the required approval threshold; and, (iv) the manner of treating non-response/non-participation of an investor, as per the chosen methodology. |

| 3b. | For obtaining investor consent through deemed consent, communication sent to investors shall also disclose the timeline for providing response. The said timeline shall be uniform for all investors. |

| 3c. | For obtaining investor consent through present and voting, the manager of the AIF shall (i) hold meetings (physical/virtual/hybrid) of investors for obtaining their consent; or (ii) inform the proposal through agreed modes of communication and seek votes through physical/digital mode with disclosed voting timeline. In case of option (ii), only those investors who provide any response to the proposal within the voting timeline shall be considered to have participated in the voting process. |

| Proposal 4. | Responsibility of manager – |

| 4a. | The manager of the AIF shall be responsible for ensuring transparency, adherence to the laid down policy and fair access to all investors with respect to the process of seeking investor consent. |

| 4b. | The manager shall respond to investor queries regarding a specific proposal or the process/methodology for investor consent, within a reasonable timeframe. |

| 4c. | The records of all communications for notice, subsequent reminders, meetings and votes shall be maintained by the AIF/manager. |

| Proposal 5. | Applicability for existing funds –The extant methodologies adopted by existing schemes of AIFs shall be grandfathered. The proposed policy shall take effect from a prospective date. |

| Proposal 6. | Streamlining approval thresholds –The applicable provisions under AIF Regulations and circulars issued thereunder may be suitably amended to bring consistency in percentage threshold for unitholder consent – whereby approval of 75% of unitholder (by value) may be prescribed, wherever applicable. |

4. Rationalizing the ambit of conflicted transactions requiring investor consent under AIF Regulations

Existing regulatory framework for undertaking conflicted transactions –

4.1. The term ‘associate’ has been defined in AIF Regulations as a company or a limited liability partnership or a body corporate in which a director or trustee or partner or Sponsor or Manager of the AIF or a director or partner of the Manager or Sponsor holds, either individually or collectively, more than 15% of its paid-up equity share capital or partnership interest, as the case may be.

4.2. Various provisions of AIF Regulations make a reference to the term “associate”, which have been enumerated in the table at Annexure B. The term has been mainly used to prescribe safeguards in context of activities/transactions that have inherent conflict of interest issues. Some of the key provisions in this context are as under —

(a) Regulation 15 (1) (e) & (ea) of AIF Regulations – AlFs have been allowed to invest in associates and buy or sell investments from/to associates, only with the prior approval of 75% of investors by value of their investment in the AIF/scheme.

(b) Regulation 19F(4) & 19M of AIF Regulations – Special Situation Funds (SSFs) and Angel Funds have been entirely prohibited from investing in associates, to minimize connected party/round tripping concerns in the absence of diversification limits.

(c) Regulation 22(b) of AIF Regulations – Any fees charged to the AIF or any investee company by an associate of the Manager or Sponsor shall be disclosed periodically to the investors.

4.3. The intent of these provisions is to ensure that transactions involving heightened conflict potential are undertaken with appropriate transparency and investor awareness, without unduly constraining legitimate commercial activity.

Supervisory observations and need for rationalization –

4.4. Based on experience from supervision of AlFs, it is observed that the current definition of ‘associate’ is narrow, thus limiting the ambit of conflicted transactions that would require investor consent to be obtained. For instance, consider the following transactions which would not require investor consent as per extant framework —

a. Investment by AIF in an investee company whose director is a director of the AIF’s manager/sponsor;

b. Investment by AIF in an investee company where the controlling stake is held by the immediate relatives of director/partner of the AIF’s manager/sponsor, though the director alone holds less than 15% stake in the investee company;

c. Investment by an AIF in an investee company whose major shareholder also owns majority stake in the manager/sponsor of the AIF; and,

d. AIF buying or selling its investments from a person who is a relative of the manager/sponsor or their directors/partners.

4.5. It may be seen that the aforesaid transactions are inherently conflicted transactions. However, due to the narrow definition of ‘associates’, these transactions do not trigger investor consent requirement under the extant framework. These examples are intended to demonstrate the need for a principle aligned and outcome oriented regulatory framework with focus on materiality of the conflict involved and addressing gaps.

Comparative study and proposed approach –

4.6. In the context of the said matter, similar provisions pertaining to conflicted transactions in other regulatory frameworks were studied, as given at Annexu C. Based on the comparative study, it is seen that the term ‘related party’ has been referred under various SEBI regulations, for prescribing norms pertaining to conflicted/connected transactions. While many of these regulations consistently adopt the definition of ‘related party’ as given under Companies Act, 2013, certain changes have been carried out or additional entities have also been included to the ‘related party’ definition under these respective regulations, depending on the type of intermediary being regulated.

4.7. It is pertinent to note that AIF Regulations rely largely on adequate disclosures to investors and policy laid down by the Al F/manager for dealing with/managing conflict of interest issues which may arise over the course of business of the AIF. AIF Regulations mandate investor consent only for those transactions involving material conflict of interest, recognizing the sophisticated nature of AIF investors and the need for operational flexibility. Therefore, it is critical to prevent entities from exploiting the narrow regulatory definitions to evade mandatory investor approval for conflicted transactions.

4.8. The definition of ‘related party’ as given in Companies Act, 2013, is comprehensive in comparison to the definition of ‘associate’ given in AIF Regulations, as it covers aspects of control and relatives of key persons of the entity under consideration. Considering the same and that the same definition has been adopted under various SEBI Regulations, it is viewed that ‘related party’ as defined under Companies Act, 2013, provides a more suitable reference point for identifying material conflicted transactions that warrant investor consideration under the AIF framework.

4.9. Thus, the investor consent requirement may be made applicable to transactions with related parties of manager/sponsor of the AIF. Further, recognizing the limited role of trustee/Board of directors/designated partners of the AIF in managing the investments and day-to-day operations of the fund, it is proposed to exclude transactions with related parties of trustees/AIF (its Board of directors/designated partners) from the ambit of conflicted transactions which would require investor consent.

4.10. At the same time, it is also felt that the same definition of ‘related party’ may not be applied consistently across all the provisions of AIF Regulations where ‘associate’ is used, since the broad scope of ‘related party’ may not be required in contexts other than conflicted transactions. Thus, recognizing the need for operational flexibility, it is proposed to retain the reference to the word ‘associate’ in provisions not related to conflicted transactions.

4.11. Taken together with the proposals 1— 6 in the consultation paper on the manner of obtaining investor consent, the aforesaid proposals are intended to strengthen the transparency and conflict management provisions in the interest of the investors, without being onerous/disruptive in day-to-day operations of the AlFs.

4.12. An agenda in this regard was placed for discussion before AIPAC. AIPAC recommended the above proposals, noting that they seek to provide clearer definitions and a more structured framework for identification and approval of conflicted transactions.

| Proposals for consideration: | |

| Proposal 7. | Definition of ‘related party’ under AIF Regulations – AIF Regulations may be suitably amended to include the definition of ‘related party’ under AIF Regulations, borrowing from the definition as given under Section 2(76) of the Companies Act, 2013, while suitably modifying it to suit the AIF regulatory framework. The draft amendment proposed for the ‘related party’ definition under AIF Regulations is given at para 3 of Annexure D. |

| Proposals for consideration: | |

| Proposal 8. | For provisions in respect of conflict of interest or conflicted transactions, the term ‘associate’ may be replaced with the term ‘related party’, while retaining the existing reference to ‘associate’ in other provisions where broader coverage is not warranted. The draft changes proposed in the AIF Regulation/circular, in line with this proposal, are also given in the table at Annexure B. |

5. Public comments

5.1. Considering the implications of the aforementioned matters on the market participants, public comments are invited on the proposals 01 to 08 given above. The comments / suggestions should be submitted latest by July 21, 2026, only via online web-based form through the following link:

https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPublicComments=ves

5.2. In case of any technical issue in submitting your comment through web based public comments form, you may highlight the issues(s) to afdconsultation@sebi.gov.in, with a copy to padmab@sebi.gov.in, with the subject of the email as, “Rationalizing investor consent and conflicted transactions for AlFs”.

Issued on: June 30, 2026