Executive Summary: The New Income Tax Act, 2025 retains the core transfer pricing (TP) framework of the 1961 Act but reorganizes and refines it. Sections 161–173 of the new Act (Chapter X) correspond broadly to old Sections 92–92F and related provisions. \

Key changes include a single integrated definition of “associated enterprise” (Sec. 162), clearer “international transaction” definitions (Sec. 163), updated ALP/methodology rules (Sec. 165) and a revamped documentation regime (Secs. 171–172). Safe-harbour (Sec. 167) and APA (Sec. 168–169) provisions are also codified.

Practically, taxpayers must continue to maintain a contemporaneous TP study, file the accountant’s report (currently Form 3CEB) by the due date, and compute each cross-border (and large domestic) related-party transaction at arm’s length. Non-compliance carries heavy penalties (e.g. 2% of transaction value or 50% of tax under-reported. This report analyzes each aspect of TP under the new Act, citing exact text, explaining compliance implications, and illustrating with worked examples and charts.

Concept and Objective of Transfer Pricing

The new Act begins Chapter X by re-stating the arm’s‐length principle. Section 161(1) provides that “Any income arising from an international transaction or a specified domestic transaction shall be computed having regard to the arm’s length price.”.

In other words, related‐party transaction profits must be determined as if the parties were unrelated. The objective remains twofold:

(1) to prevent artificial profit shifting or base erosion via manipulated prices; and

(2) to align India’s TP rules with OECD/BEPS principles.

In practice, this means that if a cross-border intercompany price reduces an entity’s profit, the tax authorities will adjust it upward to the arm’s‐length price (ALP), ensuring the correct share of income is taxed here.

Importantly, Sec. 161(2) (not shown above) preserves the anti-avoidance punch of old Sec. 92(2): even if an ALP adjustment lowers taxable profit, it cannot be used to reduce tax (subject to specified thresholds). This secures tax revenue while compelling taxpayers to set or justify related-party prices.

Associated Enterprise (Sec. 162)

Section 162 consolidates the definition of “associated enterprise” into a single provision (combining old Secs. 92A and 92AD concepts). It covers various control/ownership relationships.

For example, Sec. 162(1)(a) states that an AE exists if “one enterprise holds…shares carrying not less than 26% of the voting power in the other enterprise” (previously old Sec. 92A(1)(i)).

Likewise, a loan from one enterprise constituting ≥51% of the other’s total assets makes them associated, as does a 10%+ guarantee of the other’s borrowings.

The Act further lists managerial control tests: for example, Sec. 162(1)(d)–(e) include cases where one enterprise appoints a majority of directors in the other, or the same person controls management of both entities. Other criteria (90% supply dependence, intra-group sales/pricing control, and personal relationships) are also spelled out.

In short, Sec. 162(1) covers shareholding, debt, guarantees, mutual control, and family ties. Sub-section (2) then extends AE coverage for specified domestic transactions (SDTs): e.g. other units or businesses of the assessee (Sec. 122 transactions) or persons under Sec. 140/144 of the Act.

Practical implication: Taxpayers must map all related parties under these tests. Any transaction with a person meeting these AE criteria falls under TP rules (either international or domestic), triggering documentation and ALP compliance.

International Transaction (Sec. 163)

Section 163 defines “international transaction” broadly as any cross-border transfer between associated enterprises. The definition (Sec. 163(1)) explicitly includes:

- Tangibles: sale, purchase, lease or use of goods, machinery, vehicles, etc. (163(1)(a)).

- Intangibles: transfer or use of patents, trademarks, know-how, technical contracts, brands, customer lists, data, etc. (163(1)(b)).

- Financing: loans, guarantees, purchase/sale of marketable securities, advances/receivables, etc. (163(1)(c)).

- Services: any professional, technical, marketing, or management services (163(1)(d))[14].

- Business reorganizations: any cross-border restructuring/reorganization (163(1)(e)).

- Cost-sharing: allocations of joint costs or contributions among AEs (163(1)(f)).

Sub-section (2) “deems” a third-party transaction to be an international transaction if a prior agreement exists between the foreign AE and that third party or if the terms are in substance driven by the AE (even if the counterparty is not an AE).

Implication: Any cross-border related-party dealings in goods, intangibles, services, financing, or reorgs fall under TP. Companies must analyze even indirect schemes (e.g. conduit arrangements) to identify if Sec. 163’s catch-all (including “any other transaction having a bearing on profits” at 163(1)(g)) applies.

Specified Domestic Transactions (Sec. 164)

Section 164 mirrors the old Sec. 92BA definition of SDTs. An SDT means any domestic transaction listed in Sec. 164 if total value in a year exceeds ₹20 crore.

These include: transactions referred to in Sec. 122 , transfers under Sec. 140(9) (assets/business transfers), business with persons under Sec. 140(13), transactions under certain other provisions of Chapter VIII or Sec. 144 with the arm’s-length clauses (140(9)/(13)/80-IA clauses), transactions under Sec. 205(4) (shareholders in demerged companies), and any prescribed transaction.

In short, large-value domestic related-party deals (e.g. between a parent and subsidiary) are brought into TP ambit via Sec. 164. Practically, an Indian taxpayer must check if any such SDT exceeds ₹20 Cr; if yes, the ALP rules apply just as for international cases.

Arm’s-Length Principle & Computation (Secs. 161, 165)

Sec. 161(1) restates that income from an international/SDT must be computed at ALP. Sec. 165 then prescribes how to compute ALP. Section 165(1) lists the six acceptable methods (the “traditional five” plus any “other method”):

- Comparable Uncontrolled Price (CUP)method (165(1)(a)),

- Resale Price method (165(1)(b)),

- Cost Plus method (165(1)(c)),

- Profit Split method (165(1)(d)),

- Transactional Net Margin (TNMM)method (165(1)(e)),

- Other prescribed method(165(1)(f)).

The taxpayer must select the Most Appropriate Method (MAM) for each transaction, per Sec. 165(2): “The most appropriate method… shall be selected having regard to the nature of the transaction… or the functions performed by such associated enterprises.”.

In practice, this means conducting a detailed FAR (Function-Asset-Risk) analysis: examining what each AE does, what assets/intangibles they use, and what risks they bear. The FAR outcome guides the choice of method. For example, manufacturing entities often use CUP or resale methods, whereas service providers often use TNMM.

Once the MAM is chosen, comparable transactions (or companies) are identified to benchmark pricing. The ALP is then the price (or profit margin) derived from these comparables.

Section 165(3) states that “any of the methods referred to in sub-section (1) may be adopted” to compute arm’s length price. If the Assessing Officer believes the declared ALP is incorrect, Sec. 165(4)–(6) empower unilateral re-determination (similar to old Sec. 92C(3)–(4)), subject to prescribed safeguards.

Practical Implications: Taxpayers must perform and document the MAM analysis. The ALP outcome must be the benchmark value (e.g. median of comparable margins). Any deviation may trigger adjustment by the Tax Officer (with penalties if misreporting).

The choice and application of methods should follow OECD Guidelines and judicial precedents. For instance, Courts have emphasized that comparables must be functionally and economically similar (see CIT v. Mahindra & Mahindra for automotive bench‐marking, CIT v. LG Electronics for intangible transfers, etc.).

Functional Analysis and Comparables Selection

(While not in the Act, a FAR analysis and comparables search are essential steps.) A practical step-by-step approach is:

1. Identify the transaction(s) and select the tested party (often the one with less complex functions/risks or for whom data is reliable).

2. Perform FAR analysis: Document exactly what functions each party performs (manufacturing, marketing, R&D, financing, etc.), what assets/intangibles they employ (factory, brands, patents), and what risks they bear (market risk, credit risk, operational risk). This analysis is often tabulated and is the foundation for method choice.

3. Determine MAM: Based on FAR and the OECD/Rule 10D comparability factors, pick the method that most reliably measures ALP (e.g. CUP if identical product sold at uncontrolled price exists, or TNMM if only profits available). Cite Sec. 165(2) which directs method selection by transaction nature.

4. Search for comparables: Use external databases to find independent companies or transactions. Apply filters for industry (NIC codes), geographic market, company size, credit rating, accounting period, etc., to ensure they are comparable (as per Rule 10D guidelines, e.g. CIT v. Veer Gems & Jewellers, 343 ITR 28 (SC) on broad comparability factors).

5. Adjust and finalize comparables: Adjust for material differences (e.g. market conditions, warranty terms) if feasible. Compute the applicable measure (price, cost markup, gross profit margin, net margin, etc.) for each comparable.

6. Compute ALP range/median: From the comparables set, derive an ALP (e.g. median of the net margins). If the taxpayer’s actual price/margin lies within a reasonable range, no adjustment is needed; otherwise an adjustment is warranted.

Illustration: Example Transaction: An Indian manufacturing subsidiary sells 10,000 widgets to its foreign AE at ₹1,000/unit (₹10,000,000 total). Its cost of goods sold (COGS) is ₹800/unit (₹8,000,000), yielding profit ₹2,000,000.

Comparable independent distributors use a resale-price method: resale margin data show a 5% gross margin. The arm’s-length resale price would be ₹1,050 (since ₹1,000 × 1.05). Thus, ALP for 10,000 units = ₹10,500,000. The primary adjustment is ₹500,000. This is reflected in the books as:

- Original entry (no adjustment):

- Dr Debtors (AE) ₹10,000,000

- Cr Sales ₹10,000,000

- Dr COGS ₹8,000,000

- Cr Inventory ₹8,000,000

- Tax adjustment entry:

- Dr Debtors (AE) ₹500,000

- Cr “TP Adjustment” or Income ₹500,000

Result: Total Sales ₹10,500,000, COGS ₹8,000,000, Profit ₹2,500,000 (per ALP). Tax is then paid on ₹2.5 million instead of ₹2 million. If the ₹500,000 is not repatriated by year-end, a secondary adjustment applies (see below).

This example illustrates how FAR (functions: sales/distribution; assets: inventory; risk: resale market risk) leads to using the resale-price method, and how comparables determine ALP. A detailed TP study would document all these steps.

Safe Harbour (Sec. 167)

Section 167 introduces Safe Harbour rules: the CBDT can notify specific pricing guidelines that, if followed by eligible taxpayers, will be deemed arm’s-length.

It states: “The determination of income referred to in section 9(2) or the determination of arm’s length price in relation to an international transaction or specified domestic transaction shall be subject to such safe harbour rules as may be prescribed”.

In practice, taxpayers can opt for safe harbour (e.g. simple markup for low-value intra-group services or loans) to reduce dispute risk.

However, opting in does not waive compliance: even under safe harbour, documentation and form-filing are required, and any excess (if profit falls below the safe-harbour threshold) may be penalized per normal rules.

Advance Pricing Agreements (Sec. 168–169)

Sections 168–169 formalize India’s APA program. Sec. 168 authorizes the CBDT to enter into binding APAs (unilateral, bilateral or multilateral) on the ALP of specified international transactions. It notes that APAs can cover ALP under Sec 165 or computing income under Sec 9(2).

Once an APA is valid, the taxpayer enjoys certainty: for instance, Sec. 166(2) explicitly prohibits a TPO reference if a valid APA has been declared for that year. After an APA is entered, Sec. 169 requires the assessee to compute income as per the APA for covered years – even allowing them to amend a return or revisit previous assessments to give effect to the APA terms.

Practical note: Taxpayers with complex cross-border transactions should consider the APA route for certainty, but must still file complete documentation and “map” APA transactions (e.g. see proposed Form 48).

Documentation (Sec. 171) and Accountant’s Report (Sec. 172)

Section 171 imposes record-keeping requirements (akin to old Sec. 92D). Every taxpayer entering into international or specified domestic transactions must maintain detailed information and documents in the prescribed form and manner (functional analysis, comparability data, contracts, pricing, financials, etc.).

The Assessing Officer may require the TP study, agreements or data during assessment. Section 172 mandates the filing of an accountant’s report (old Form 3CEB).

It states: “Every person who has entered into an international transaction or specified domestic transaction during a tax year shall obtain a report from an accountant and furnish such report on or before the specified date in the prescribed form…”.

The “specified date” means the due date of the income-tax return (e.g. 30 September for companies, or as extended).

The Report (Form 3CEB) must be digitally signed by a Chartered Accountant and include prescribed details (transaction values, ALP adopted, etc.). Failure to maintain TP documents (Sec. 171) or to furnish the Report (Sec. 172) triggers penalties, as discussed below.

Penalties and Adjustments

The new Act significantly beefs up penalties:

- Under-reporting Penalty: If an income from a related-party transaction is adjusted upward (under-reported), Sec. 174(9) imposes penalty of 50% of the tax payable on the under-reported amount. For willful misreporting (fraud, omission, etc.), Sec. 174(10) doubles this to 200%.

- Documentation Penalty: Section 457 penalizes failures under Sec. 171.

It provides: “If any person who has entered into an international transaction or specified domestic transaction fails to furnish any such information or document as required under section 171(2), a penalty equal to 2% of the value of such transaction may be imposed for each such failure”.

This effectively replaces the old Sec. 271BA penalty. For example, failing to prepare/produce the TP study, or submit the accountant’s report on time, attracts a 2% penalty on each transaction value.

- Secondary Adjustment: Section 170 addresses secondary adjustments. If a primary ALP adjustment results in excess profits “deemed distributed” as a loan between AEs, then Sec. 170(1) requires the assessee to increase its books accordingly (driving capital or inter-company loan accounts).

If the “loan” is not repatriated within the prescribed period, Sec. 170(2) further mandates an additional tax (33.99% plus interest) on that amount (though no penalty applies under Sec. 170(5) if repatriated eventually). This ensures the excess profit is not tax-deferrable indefinitely.

- Other Penalties: Incorrect TP disclosures (e.g. claiming non-arm’s-length prices knowingly) can also lead to penalties under Secs. 270A/271 etc., as before.

Implications for Compliance and Audit: CAs and companies must be diligent. Maintaining contemporaneous TP documentation, conducting a proper FAR and economic analysis, and filing accurate TP reports are mandatory.

During an assessment, the AO/TPO will scrutinize the TP report; any omission or inconsistency can trigger the above penalties.

Similarly, opting into safe harbour or APA programmes still requires full compliance with TP formalities.

Practical CA insight: always insist on detailed comparability checks and back up each adjustment with robust analysis to withstand TPO scrutiny (per CIT v. LG Electronics India and CIT v. Maruti Suzuki principles).

Sample Transfer Pricing Study Report (Template)

A typical CA-prepared TP study contains the following sections:

1. Executive Summary: Overview of company, group structure, and key TP conclusions (e.g. “All transactions have been benchmarked; the ALP margins lie within the prescribed ranges.”).

2. Company and Industry Profile: Description of the taxpayer’s business, industry conditions, financial performance, and intangibles (e.g. brand strength, market share).

3. Transaction Details: Description of related-party transaction(s) (nature, terms, pricing, year-end balances).

4. FAR Analysis: Detailed table of Functions, Assets, and Risks for each entity in the transaction (e.g. “Indian Co.: manufactures widgets, owns plant and inventory, bears market risk; Foreign AE: provides brand and marketing, collects payment.”).

5. Method Selection: Justification of the chosen method (e.g. “TNMM selected as most reliable method given sales function and lack of exact public comparable prices”, citing Sec. 165(2).

6. Comparables Search: Explanation of search filters (industry codes, geographic market, time period, size) and adjustments made.

7. Benchmark Analysis: Data of comparables (book values, net margins, etc.), and calculation of ALP (e.g. median margin or range).

8. Results: Comparison of actual outcome with ALP (showing that transfer price or margin is at/above ALP, or if not, quantifying the adjustment). Include any primary adjustment journal entries and resulting tax.

9. Conclusion: Affirmation that ALP has been met or, if adjustments were made, that they are correctly accounted for.

10. Appendices: Copies of intercompany agreements, financial statements, calculation details, and relevant correspondence (e.g. APA papers).

(This is a notional template. CA’s actual report should be customized to the case.)

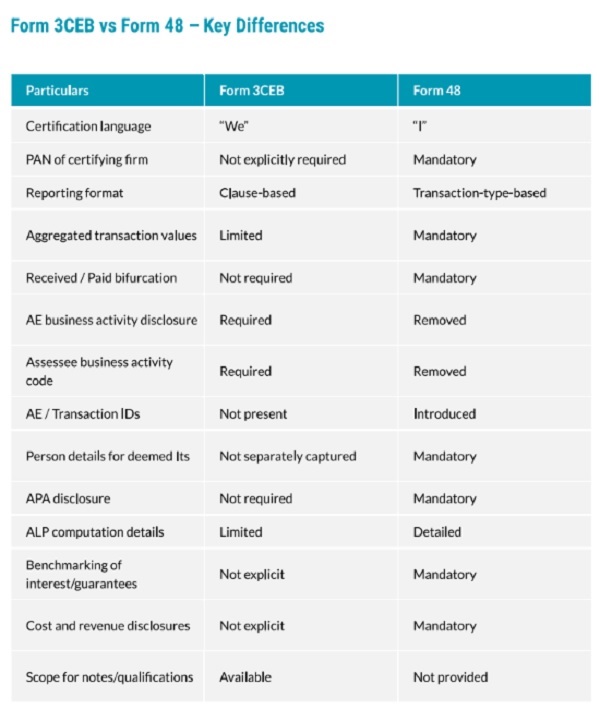

Example: Accountant’s Report (Form 3CEB( Now Form 48)) –

Note: Currently, the Income-tax Rules 1962 (as amended) still prescribe Form 3CEB( Now Form 48) for the accountant’s report. Draft rules 2026 propose a new “Form 48” for AY 2027-28 onwards, but until notified, Form 3CEB( Now Form 48) is used.

| Form No. 48 – Key Changes, Implications, and Areas Requiring Clarification [Click here] |

Below is a simplified illustration of relevant parts of Form 3CEB( Now Form 48) for an example transaction (the widget sale above):

| Clause | Details for AY 2026-27 (FY 2025-26) |

| (i) Name & address of assessee | ABC Widgets Pvt. Ltd., Mumbai (PAN, CIN) |

| (ii) Taxpayer status | Domestic company (resident) |

| (iii) Related foreign enterprises | XYZ Global Inc. (Shareholding 40%), Singapore |

| (iv) International Transactions | Sale of 10,000 widgets to XYZ Global Inc. @₹1,000 each (₹10,000,000) |

| (v) ALP Method adopted | Resale Price Method (determined arm’s length price ₹1,050/unit) |

| (vi) Price at ALP | ₹10,500,000 total |

| (vii) Primary adjustment | +₹500,000 (due to ALP > actual price) |

| (viii) SDT Transactions | None |

| (ix) Secondary adjustment | (If applicable) Tax computed on ₹500,000 if not repatriated (Interest charged at Sec. 234C rates) |

| (x) Accountant’s opinion | Confirms ALP adoption, and that TP documentation is maintained. |

| (Signature, CA stamp) | (Signed by CA) |

(This illustrative snippet shows how the accountant would disclose transaction details, ALP methodology, and adjustments. In practice, Form 3CEB( Now Form 48) is much longer.)

Forms, Due Dates, and CA Responsibilities

- Form 3CEB( Now Form 48) (Accountant’s Report):Due along with the income-tax return (generally 30 Sep for companies; 30 Nov for non-corp assessees). CAs must prepare and sign this form, verifying that all related-party transactions are reported, and disclose the ALP determination.

- TP Study: Not filed with the return but must be ready by March 31 following the year (or as prescribed). CAs should compile a detailed TP report/study, ensure it meets Rule 10D requirements, and retain it in case of inspection.

- Disclosure in Tax Audit (Form 3CD Clause 14AA):TP details (taxpayer’s “turnover” with AEs, ALP adopted, etc.) must be reported in the tax audit report (under Clause 14AA, formerly 44DA). This is typically part of the tax audit done by CAs under Sec. 44AB.

- Advance Pricing Agreement Application (Form 3CAA/3CCAA):If seeking an APA, apply in prescribed form, providing TP data for 3 years past and proposed 5 years future.

- Safe Harbour Compliance: If opting for safe harbour for e.g. intra-group services or loans, ensure all eligibility criteria are met each year (revenue thresholds, prescribed methodology). Option is declared in the return.

- Transfer Pricing Audit (Sec. 92CD):After assessments, if TP adjustments are made, the case may be assigned to a TP Officer for audit. CAs should prepare for such TP audit – having all justifications and doc in order.

In summary, CAs must advise clients to align TP practices with the new Act: review all related-party dealings under Sec. 162/163, choose and document ALP methods (Sec. 165), comply with documentation (Sec. 171–172), and note the shifted penalties (Secs. 457, 174). Early planning (FAR, comparables, APAs) and rigorous documentation are key to minimizing risk.

Clause-by-Clause Comparison: Old vs New Act

| Old ITA 1961 | Subject | New ITA 2025 | Comments |

| Sec. 92(1)–(6) | ALP principle, no deduction if profit <90% of ALP | Sec. 161, 165 | Sec. 161(1) echoes 92(1) arm’s-length rule; 165 covers methods. |

| Sec. 92A | Associated enterprises (shareholding, management) | Sec. 162 | AE definition consolidated in Sec. 162 |

| Sec. 92B | International transaction definition | Sec. 163 | Rewritten, broader international transaction list |

| Sec. 92C | ALP methods (5 methods) | Sec. 165 | Preserves five methods and “other” (10AB); includes MAM rules. |

| Sec. 92D | Maintenance of information and documentation | Sec. 171 | Modernized record-keeping requirements (similar scope). |

| Sec. 92DA, 92DB | Safe harbours (int’l & loans) | Sec. 167 | Safe-harbour regime now in Sec. 167 (“subject to safe harbour rules”) |

| Sec. 92E | Accountant’s report (Form 3CEB( Now Form 48)) | Sec. 172 | Continues obligation to furnish CA’s report by due date |

| Sec. 92BA | Specified domestic transactions definition | Sec. 164 | SDT list retained with ₹20 Cr threshold |

| Sec. 92BB | “Other person” definitions (for Sec. 92BA cases) | — (Included in 163) | Many “other person” cases absorbed into broader Sec. 163 deeming rule. |

| Sec. 92F | Meaning of terms (“international transaction”, etc.) | Sec. 173 (definitions) | Definitions consolidated in Sec. 173 (ALP, enterprise, etc.). |

| Sec. 92CE | Secondary adjustment | Sec. 170 | Secondary adjustment and interest rules in Sec. 170 |

| Rule 10A–10E, 10AB | TP rules (methods, comparability, APAs, etc.) | To be updated* | These Income-tax Rules (1962) will apply till new rules; draft “TP Rules, 2026” incorporate many changes (e.g. Form 48). |

Note: The above mapping is indicative; taxpayers should refer to the text of each section/rule for exact details. Sec. 173* of the new Act contains definitions (ALP, enterprise, etc.), replacing old Sec. 92F (definitions).

Global Alignment

The new Act aligns India’s TP regime closely with OECD/BEPS standards. The integrated AE definition and broad int’l transaction concept mirror the OECD model.

Advance pricing agreements, safe harbours and specific anti-avoidance rules ensure India remains on par with global practice.

For example, Sec. 163’s inclusion of business restructurings (163(1)(e)) and cost contributions (163(1)(f)) reflects BEPS Action 8 guidance.

Taxpayers should also consider Transfer Pricing Guidelines (OECD, 2022) as a compliance benchmark, especially for functional analysis and comparability.

Sources: Primary source is the new Income-Tax Act, 2025 (e-Gazette). Authoritative commentary (CBDT notifications, OECD TP Guidelines) and case law (e.g. Veer Gems, Mahindra, LG Electronics) inform the practical insights above. All section citations use the new Act’s numbering for clarity.

| Form No. 48 – Frequently Asked Questions | [ Click here ] |

******

Disclaimer: This document has been prepared for educational and informational purposes only, with the objective of providing a comprehensive understanding of Transfer Pricing provisions under the Income-tax Act, 2025. While every effort has been made to ensure that the contents of this document are accurate, updated, and aligned with the statutory provisions, including relevant sections, rules, and practical interpretations, the same should not be construed as professional advice, legal opinion, or a substitute for consultation. The provisions of Transfer Pricing are highly interpretative and fact-specific, and their application may vary depending upon the nature of transactions, industry practices, judicial precedents, and regulatory developments. Readers are advised to refer to the original text of the Act, Rules, notifications, and circulars issued by the tax authorities, and to seek appropriate professional advice before acting on any matter discussed herein. The author does not accept any liability for any loss or damage arising directly or indirectly from reliance on the contents of this document. The examples used are purely illustrative in nature and are intended to facilitate conceptual clarity. Further, the law is subject to amendments, judicial interpretations, and administrative guidance, which may not have been fully captured at the time of preparation of this document.

Author Bio