Pradhan Mantri MUDRA Yojana (PMMY): A Complete Guide to Shishu, Kishore, Tarun and Tarun Plus Loans

Introduction : Access to timely and affordable finance has always been one of the most critical challenges faced by micro and small entrepreneurs in India. A large segment of businesses—such as small traders, shopkeepers, artisans, service providers, and first-generation entrepreneurs—operate outside the formal corporate structure and often lack collateral or a documented credit history, making traditional bank financing difficult

Pradhan Mantri MUDRA Yojana (PMMY) is a scheme launched by the Hon’ble Prime Minister on April 8, 2015 for providing loans up to 20 lakh (for those entrepreneurs who have availed and successfully repaid previous loans under the ‘Tarun’ category) to the non-corporate, non-farm small/micro enterprises.

These loans are classified as MUDRA loans under PMMY. These loans are given by Commercial Banks, RRBs, Small Finance Banks, MFIs and NBFCs. The borrower can approach any of the lending institutions mentioned above or can apply online through this portal www.udyamimitra.in

Under the aegis of PMMY, MUDRA has created four products namely ‘Shishu’, ‘Kishore’, ‘Tarun’ and ‘Tarun Plus’ to signify the stage of growth / development and funding needs of the beneficiary micro unit / entrepreneur and also provide a reference point for the next phase of graduation / growth.

| MUDRA is a refinancing Institution. MUDRA does not lend directly to the micro entrepreneurs / individuals. Mudra loans under Pradhan Mantri Mudra Yojana (PMMY) can be availed of from nearby branch office of a bank, NBFC, MFIs etc. Borrowers can also now file online application for MUDRA loans on Udyamimitra portal (www.udyamimitra.in). |

Note: There are no agents or middleman engaged by MUDRA for availing of Mudra Loans. The borrowers are advised to keep away from persons posing as Agents/ facilitators of MUDRA/PMMY.”

Basic Question about this government loan :

1. The financial limit for these schemes are:-

- Shishu :covering loans upto 50,000/-

- Kishor : covering loans above 50,000/- and upto 5 lakh

- Tarun :covering loans above 5 lakh to 10 lakh

- Tarun Plus :covering loans above 10 lakh to 20 lakh (for those entrepreneurs who have availed and successfully repaid previous loans under the ‘Tarun’ category).

| MUDRA’s delivery channel is conceived to be through the route of refinance primarily to Banks/NBFCs/MFIs. At the same time, there is a need to develop and expand the delivery channel at the ground level.

In this context, there is already in existence, a large number of ‘Last Mile Financiers’ in the form of companies, trusts, societies, associations and other networks which are providing informal finance to small businesses. |

2. WHO ARE THE TARGET CLIENTS OF MUDRA/ WHAT KIND OF BORROWERS ARE ELIGIBLE FOR ASSISTANCE FROM MUDRA?

Non–Corporate Small Business Segment (NCSB) comprising of millions of proprietorship / partnership firms running as small manufacturing units, service sector units, shopkeepers, fruits / vegetable vendors, truck operators, food-service units, repair shops, machine operators, small industries, artisans, food processors and others, in rural and urban areas.

3. I HAVE DIPLOMA IN FOOD PROCESSING TECHNOLOGY. I WANT TO START MY OWN UNIT. PLEASE GUIDE ME.

Food Processing is an eligible activity for coverage under one of the MUDRA schemes. You can avail of assistance under MUDRA schemes for food processing from any financing banks/MFIs/NBFCs.

4. I HAVE GRADUATED RECENTLY. I WANT TO START MY OWN BUSINESS. CAN MUDRA HELP ME?

MUDRA loans are available in three categories. For small business, loans upto 50,000/- is available under the ‘Shishu’ category and beyond 50,000/- and upto `5 lakh under the ‘Kishor’ category.

It also offers loans beyond 5 lakh and upto 10 lakh under the Tarun category and beyond 10 lakh and upto `20 lakh under the Tarun Plus category (for those entrepreneurs who have availed and successfully repaid previous loans under the ‘Tarun’ category).

Depending on the nature of business and project requirement you can access finance from one of the intermediaries of MUDRA as per the norms.

5. I WANT TO EXPAND MY POTTERY BUSINESS BY ADDING MORE VARIETY AND DESIGNS. WHAT HELP CAN I GET FROM MUDRA?

You can avail assistance under the ‘Shishu’ category through any banks/NBFCs/ MFIs operating in your region for setting up your own enterprise.

6. IS OBTENTION OF PAN CARD A MUST TO AVAIL PMMY LOANS?

PAN card is not compulsory to avail PMMY loans. However, the borrower may have to satisfy the KYC requirements of the financing institutions.

7. IS IT REQUIRED TO SUBMIT IT RETURNS FOR THE PRECEDING 2 YEARS FOR AVAILING LOAN OF `10 LAKH UNDER PMMY?

Generally, IT returns are not insisted for small value loans. However, the requirement of documents will be advised by the concerned lending institutions based on their internal guidelines and policies.

8. UNDER PMMY-SHISHU LOANS, WHAT IS THE TURN AROUND TIME FOR PROCESSING THE LOAN PROPOSAL?

For Shishu loans, normally the turn-around-time for processing the loan proposals on receipt of complete information is 7 to 10 days.

9. ARE MUDRA LOANS AVAILABLE FOR PURCHASE OF CNG TEMPO/TAXI?

MUDRA loans would be available for purchase of CNG Tempo/Taxi, in case the applicant intends to use the vehicle for commercial purposes.

10. IS KHADI ACTIVITY ELIGIBLE UNDER PMMY LOANS?

Yes. MUDRA loans are applicable for any activity which results in income generation. As Khadi is one of the eligible activities under Textile sector and in case MUDRA loans are taken for income generation, the same can be covered.

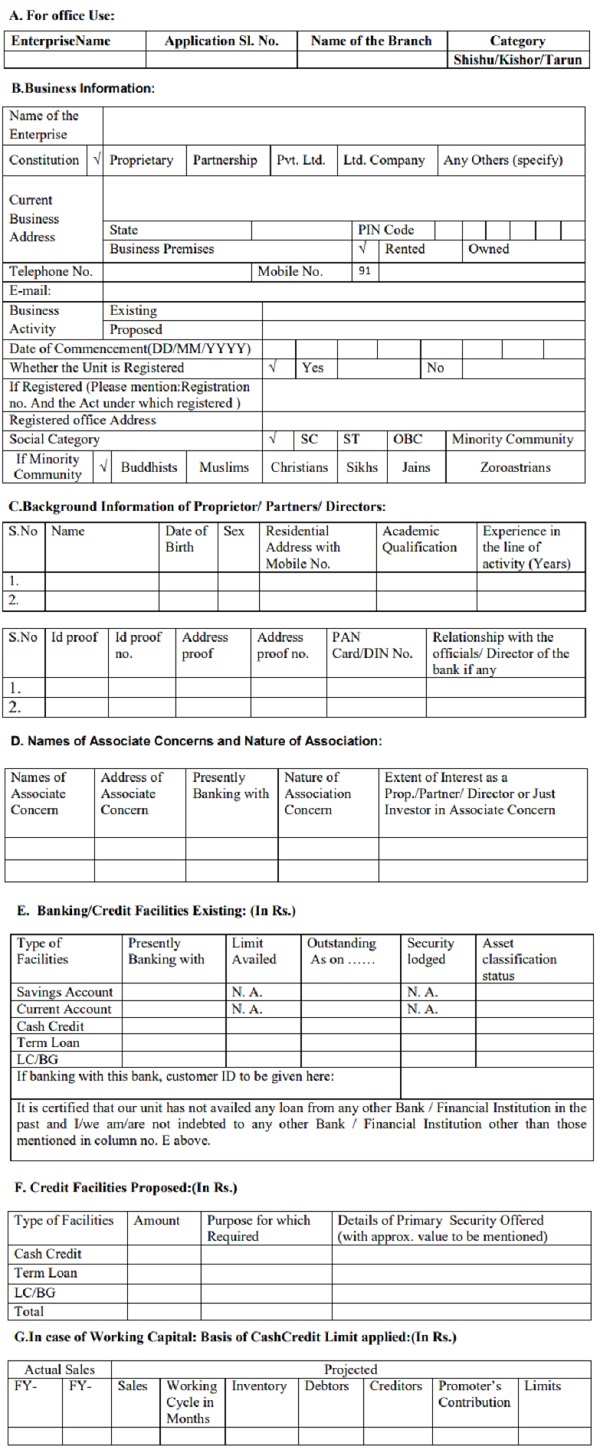

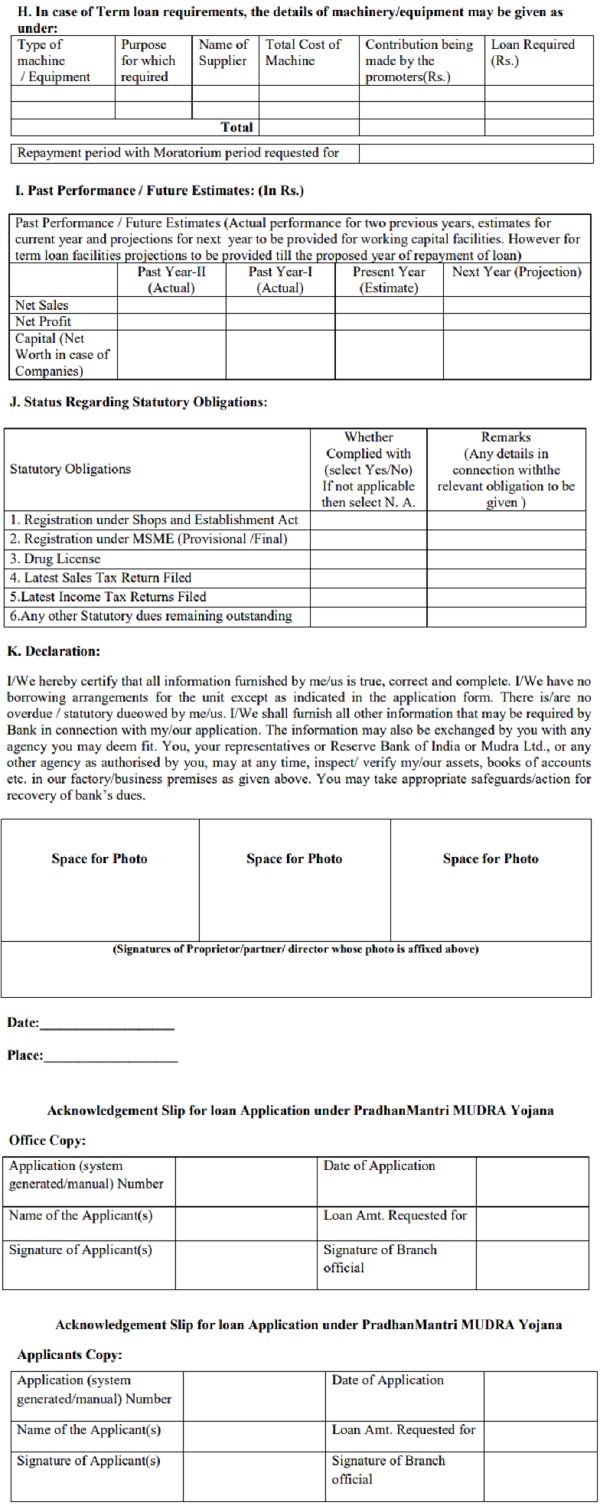

Common Loan Application form for Kishor, Tarun

LOAN APPLICATION FORM PRADHAN MANTRI MUDRA YOJANA

( To be submitted along with documents as per the check list )

Download loan application form – Click here

–

CHECK LIST FOR DOCUMENT REQUIRED FOR THESE LOANS :

(The check list is only indicative and not exhaustive and depending upon the local requirements at different places addition could be made as per necessity)

1) Proof of identity – Self certified copy of Voter’s ID card / Driving License / PAN Card / Aadhar Card/Passport.

2) Proof of Residence – Recent telephone bill, electricity bill, property tax receipt (not older than 2 months), Voter’s ID card, Aadhar Card & Passport of Proprietor/Partners/Directors.

3) Proof of SC/ST/OBC/Minority.

4) Proof of Identity/Address of the Business Enterprise – Copies of relevant licenses/registration certificates/other documents pertaining to the ownership, identity and address of business unit.

5) Applicant should not be defaulter in any Bank/Financial institution.

6) Statement of accounts (for the last six months), from the existing banker, if any.

7) Last two years balance sheets of the units along with income tax/sales tax return etc. (Applicable for all cases from Rs.2 Lacs and above).

8) Projected balance sheets for one year in case of working capital limits and for the period of the loan in case of term loan (Applicable for all cases from Rs.2 Lacs and above).

9) Sales achieved during the current financial year up to the date of submission of application.

10) Project report (for the proposed project) containing details of technical & economic viability.

11) Memorandum and articles of association of the company/Partnership Deed of Partners etc.

12) In absence of third party guarantee, Asset & Liability statement from the borrower including Directors& Partners may be sought to know the net-worth.

13) Photos (two copies) of Proprietor/ Partners/ Directors.

| Common Loan Application form for Kishor, Tarun | Download |

Author Bio