E- Commerce (electronic commerce or EC) is an online interface business model linking the buyer and seller of goods and services, or the transmitting of funds or data, over an electronic network, internet or online social networks. Before we discuss about the impact of GST on E-Commerce, let’s see a basic E– Commerce Models and understand how they function and transact.

E-Commerce is also a distribution model of supply chain to receive orders and distribute the products or services to the customers that is the order from the customer and the order completion (fulfillment) through the online platform. E- Commerce is a structure that includes not only those transactions that center on buying -selling goods and services, providing customer service, sales support but also those transactions that support data and information, communication support between organizations and other business related transactions for revenue generation. These activities include generating demand for goods and services, offering sales support and customer service, or facilitating communications between business partners etc. Some of the examples are booking travel tickets or hotel accommodation; buying online books, cloths, TV, mobiles, electronic hardware/ software; getting or sharing information and diverse other online business transactions and customer services etc.

E-Commerce Business Models:

Electronic Commerce (E-Com) is a platform in which buying and selling of goods is done online and for this internet is needed. Based on the nature of Buyer and Seller and type of business, there could be four models of E-Commerce: These business transactions occur either as Consumer-to-Consumer (C2C), Business-to-Business (B2B), Business-to-Consumer (B2C), or Consumer-to-Business (C2B).

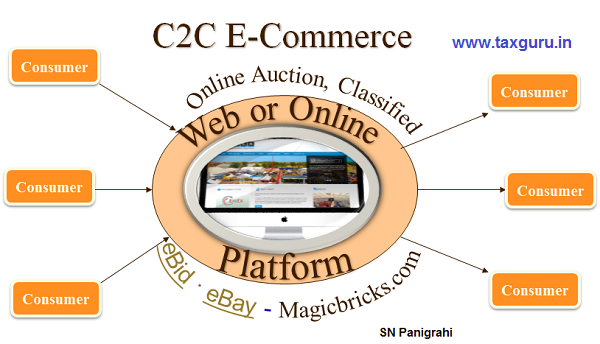

C2C (Consumer to Consumer) E-Commerce Model

C2C transactions happen between customers. Individual consumers may sell a wide variety of services/ products on the Web or through auction sites to other consumers. The E-Commerce players provide the platform and the processes, through which the transaction takes place. A commission on the transaction value will be the gain for the E-Commerce player. Example of C2C businesses are – Online auction (eBid · eBay · Bonanza · OnlineAuction.com), Online Classifieds, Online Real estate /. Rent (Commonfloor.com, Magicbricks.com, and 99acres.com) etc.

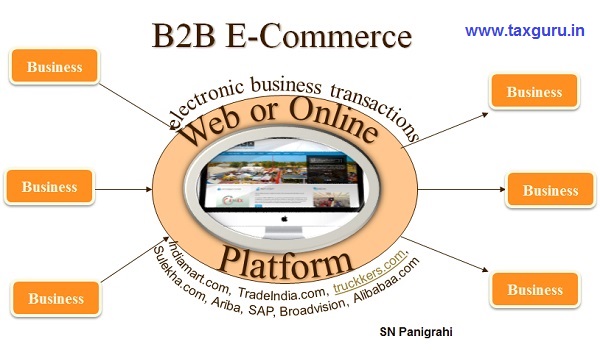

B2B (Business to Business) E-Commerce Model

B2B are the electronic business transactions among and between businesses. The Internet and reliance of all businesses upon other companies for supplies, utilities, and services has enhanced the popularity of B2B e-commerce and made B2B the fastest growing segment within the e- commerce environment. Examples of this model: Indiamart.com, TradeIndia.com, truckkers.com, Sulekha.com, Oracle, PeopleSoft, SAP, Broadvision, Commerce One, Heatheon/Webmd, 12 Technologies, Inc., Ariba , Aspect Development, Baan, BEA Systems, Internet Capital Group, VerticalNet, Vignette are some of the major vendors of e-commerce and B2B solutions.

B2C (Business to Consumer) E-Commerce Model

B2C is the most common form of E-Commerce in which a variety of goods are available. In B2C e-commerce, businesses sell directly a diverse group of products and services to customers Few categories to name are Electronics, Apparels, White goods, Footwear, Stationery, and services like Online Travel Booking and Online Matrimonial websites. Few key players at different categories of B2C are Flip kart, Snap deal, Amazon, Clear trip, Expedia, Ibibo, IRCTC, Make My Trip, Yatra, Jabong, Myntra, Yepme, Zovi, Fab Furnish, Pepper Fry, Urban Ladder, Zansaar, Big Basket, EkStop, LocalBanya, truckkers.com, Wal-Mart Stores, the Gap and ZopNow.

Main features of this model is availability of virtual store or electronic catalog, product suggestion, account status, payment process, help disc, customer reviews etc.

C2B (Consumer-to-Business) E-Commerce Model

This business model is a complete reversal of the traditional business model in which companies offer goods and services to consumers (business-to-consumer= B2C). C2B is a kind of economic relationship that is qualified as an inverted business type. Consumer-to-business (C2B) e-commerce that involves individuals selling to businesses may include a service/ product that a consumer is willing to sell. Individuals offer certain prices for specific products/services. We can see the C2B model at work in blogs or internet forums in which the author offers a link back to an online business thereby facilitating the purchase of a product (like a book on Amazon.com), for which the author might receive affiliate revenues from a successful sale. Elance was the first C2B model e-commerce site. Companies such as pazaryerim.com and mobshop.com are examples of C2B.

Various business models as discussed above like C2C, B2B, B2C and C2B can be construed to fit into any of the operating models below.

E-Commerce Operating Models

Depending on the mode of operations, there are Three types of E-Com models :

(1) Marketplace model &

(2) Inventory Model (Buy and Sell Model)

(3) Service Aggregators

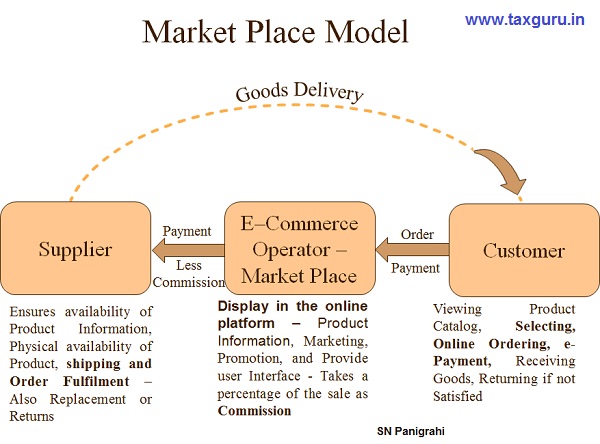

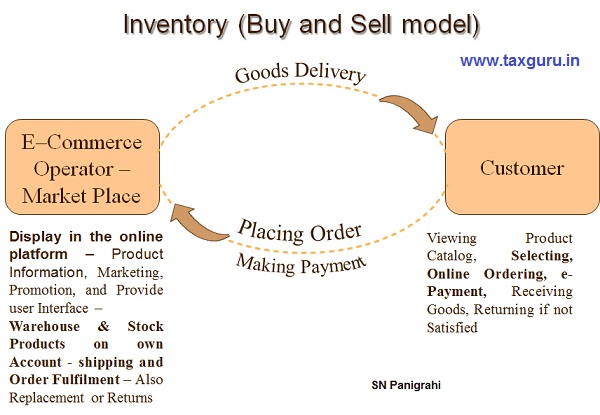

In the first model, products are displayed in the portal and once the order is received the products are picked and delivered to the customer. In the second E- Commerce model, products are procured, stored and delivered by the operator on his own after the order is received. Both the models are shown in the below schematic diagrams.

1. Market Place Model

In Marketplace model, products from multiple vendors are displayed in the online platform (Website) and the products could be from Brand, Shops or even Individual person. The marketplace provider takes care of the marketing and attracting customers, ensuring track of transactions and the user interface, whereas the vendor who is displaying his product will take care of availability of product and shipping. Marketplaces do offer shipment, delivery and payment help to merchants by tying up with some selected logistics companies and financial institutions. Marketplace provider takes a percentage of the sale as his revenue from the vendor. Marketplace doesn’t hold any physical inventory and thereby avoiding holding costs. Hence, Marketplace can offer a wide variety of products but the major concern for this model is the real time data and information flow between vendor and market place systems and product quality.

2. Inventory Model (Buy & Sell)

Shopping websites where online buyers choose from among products owned by the online shopping company or shopping website take care of the whole process end-to-end, starting with product purchase, warehousing and ending with product dispatch. A few examples of such are Jabong, Yepme and LatestOne.com.

In Inventory (Buy and Sell model), the products are purchased by the E-Commerce organization and stocked at their warehouses. Those procured products are displayed on the website and once the customer purchases the product, the product is delivered to the customer at his/her doorstep. In this model, huge inventory holding cost is a major setback but the benefit is the product can be delivered quickly to the customer and also highest level of customer experience can be provided since the E-Commerce provider manages and accountable for the delivery and quality of the product.

E – Commerce in India :

India’s e-commerce market is estimated to have crossed Rs. 211,005 crore in December 2016 as per the study conducted by Internet and Mobile Association of India. The report further claim that India is expected to generate $100 billion online retail revenue by the year 2020.

According to a ASSOCHAM-Forrester study, India’s E-commerce revenue is expected to jump from $26 billion in 2016 to $103 billion in 2020. While in terms of the base, India may be lower than China and other giants like Japan, the Indian rate of growth is way ahead of others. Against India’s annual growth rate of 51%, China’s E-commerce market is growing at 18%, Japan at 11% and South Korea at 10%, according to the joint study.

GST Provisions for E – Commerce :

The E-commerce industry in India is getting increasingly more competitive. Given the potential of the E-commerce industry in India, special provisions are made in the GST. Let us discuss in this paper, relevant provisions of GST which shall apply to E- Commerce Transactions.

What is E – Commerce & Who is E – Commerce Operator :

As per Sec 2(44) of CGST Act, “electronic commerce” means the supply of goods or services or both, including digital products over digital or electronic network;

Sec 2(45) of CGST defines “electronic commerce operator” as any person who owns, operates or manages digital or electronic facility or platform for electronic commerce;

Therefore as per the above definitions, in case Amazon and Flipkart like operators are facilitating actual suppliers to supply goods through their platform (Market place model or Fulfillment Model) to customers, they are called e-commerce Operators, where as if Amazon and Flipkart supplies which they supply on their own account by buying & stocking and then supplying to customers (inventory Model), then they will not be treated as e-commerce operators. Such supplies in the second case are treated as normal supply and all the provisions as applicable for normal cases shall apply. The only distinction between an aggregator and Market place e-commerce operators is that an aggregator provides underlying services under his brand.

GST Provisions for Market Place Model E – Commerce Operator:

Sec 52 of CGST Act, provides for collection of tax at source by an electronic commerce operator, at a notified rate where the consideration for supplies is to be collected by the operator. This clause elaborates on date of collection, date of payment of the amount to the credit of Government and filing of prescribed statements. Some of the key features are :

- Compulsory Registration :

Both the Supplier through the E – Commerce Operator and the E – Commerce Operator are compulsorily need to be Registered irrespective of value of their supply and threshold limit – Sec : 24 (ix) & (x) of CGST Act

- Registration in Every such State or Union territory in which They Operate :

Both the Supplier through the E – Commerce Operator and the E – Commerce Operator are liable to be registered in every such State or Union territory in which they operate – Sec 25. (1) of CGST Act

- Composition Scheme Suppliers Not Eligible :

Person opted for Composition Scheme is not eligible to supply of goods through an electronic commerce operator – Sec 10(2)(d) of CGST Act

- Collect TCS :

The E – Commerce operator is required to collect an amount at the rate not exceeding one per cent (be notified by the Government on the recommendations of the Council) of the net value of taxable supplies made through it by other suppliers – Sec 52. (1) of CGST Act

- Net Value of Taxable Supplies

The net value of taxable supplies mean the aggregate value of taxable supplies of goods or services or both, made during any month by all registered persons through the operator less the aggregate value of taxable supplies returned to the suppliers during the said month. For Example say Rs100 Lakhs of supplies are made by all the suppliers through the E Commerce Operator during a month, and say Rs 1 Lakh worth of goods are returned to the suppliers in the same month, then the net value of taxable supplies shall be Rs 9 Lakhs (Rs 10 – Rs 1) – Explanation to Sec 52. (1) of CGST Act

- TCS shall be paid to the Government :

TCS so collected shall be paid to the Government by the operator within ten days after the end of the month in which such collection is made, in such manner as may be prescribed – Sec 52. (3) of CGST Act

- Furnish Monthly Electronic Statement :

The E – Commerce operator shall furnish a statement, electronically, containing the details of outward supplies of goods or services or both effected through it, including the supplies of goods or services or both returned through it, and the amount collected under sub-section (1) during a month, in such form and manner as may be prescribed, within ten days after the end of such month – Sec 52. (4) of CGST Act

- Furnish Annual Electronic Statement

The E – Commerce operator shall furnish an annual statement, electronically, containing the details of outward supplies of goods or services or both effected through it, including the supplies of goods or services or both returned through it, and the amount collected under the said sub-section during the financial year, in such form and manner as may be prescribed, before the thirty first day of December following the end of such financial year – Sec 52. (5) of CGST Act

- Supplier Can Claim Credit:

The supplier who has supplied the goods or services or both through the operator shall claim credit, in his electronic cash ledger, of the amount collected and reflected in the statement of the operator furnished – Sec 52. (7) of CGST Act

- Matching of Details Furnished :

The details of supplies furnished by every operator under sub-section (4) shall be matched with the corresponding details of outward supplies furnished by the concerned supplier – Sec 52. (8) of CGST Act

- Communication of Mismatch :

Where the details of outward supplies furnished by the operator under sub-section (4) do not match with the corresponding details furnished by the supplier under section 37, the discrepancy shall be communicated to both persons – Sec 52. (9) of CGST Act

- Mismatch – Added to the Output Tax Liability

The amount in respect of which any discrepancy is communicated under sub-section (9) and which is not rectified by the supplier in his valid return or the operator in his statement for the month in which discrepancy is communicated, shall be added to the output tax liability of the said supplier, where the value of outward supplies furnished by the operator is more than the value of outward supplies furnished by the supplier, in his return for the month succeeding the month in which the discrepancy is communicated – Sec 52. (10) of CGST Act

- Pay Tax with Interest :

The concerned supplier, in whose output tax liability any amount has been added under sub-section (10), shall pay the tax payable in respect of such supply along with interest, at the rate specified under sub-section (1) of Section 50 (not exceeding 18%) on the amount so added from the date such tax was due till the date of its payment – Sec 52. (11) of CGST Act

- Offences & Penalties :

Provisions for serving notices, seeking information, penalties for fail to furnish the information are provided in Sec 52(12), (13) & (14) of CGST Act

The E– Commerce operator shall be liable to pay a penalty of ten thousand rupees or an amount equivalent to the tax evaded for offenses like tax not collected under section 52 or short collected or collected but not paid to the Government – Sec 122. (1) (vi) of CGST Act

- The Supplier making supplies to the customer shall be treated as normal supply and all the provisions as provided in the act shall be applicable.

GST Provisions for Inventory Model :

- Since this model is similar to any supplier and recipient of supplies, therefore shall be treated as normal supply and all the provisions as provided in the act shall be applicable.

GST Provisions for aggregator Model :

- The term ‘aggregator’ has been separately defined in the Model Law, to mean a person who owns and manages an electronic platform to enable a customer to connect with persons providing a service under the brand name of the aggregator. An aggregator (as defined) in the Model GST Law, has been subsumed in the definition of an e-commerce operator in the final act as it is redundant to define separately. So the word aggregator is dropped from the Act. The only distinction between an aggregator and other e-commerce operators is that an aggregator provides underlying services under his brand. Therefore all the provisions as discussed under Market Place shall apply in case of aggregator also.

Special Provisions :

The Central Government may notify categories of services, the tax on intra- State supplies of which shall be paid by the electronic commerce operator if such services are supplied through it, on the recommendations of the Council. Such provisions are made to ensure that the aggregators who operate from outside India do not escape tax. Provisions are also made that in case the electronic commerce operator does not have a physical presence in the taxable territory, any person representing such electronic commerce operator for any purpose in the taxable territory shall be liable to pay tax. Further also provided that where an electronic commerce operator does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

Conclusion :

Present laws of different kind and nature unable to properly recognize, assess and levy tax resulting in leakage of revenue. At the same time the E– Commerce operators were also feeling absence of proper provisions in the law leading to lot of confusion, litigation, and harassment and suffering costs of non-set off multiple taxes.

Recognizing the needs of modern day business operations and to remove confusions special provisions are made in the GST law. However, the operators are dissatisfied with some of the stringent provisions in the law and vehemently opposing Provisions of TCS which they feel blockage of huge funds, resulting in difficulties in working capital.

Author Bio

website like Just dial or Yellow pages can be termed as E Commerce operator ?

my client maintain website where he display advertisement of different suppliers and he get charge for this advertisement.

Actual sales and purchase take place outside the website. my Client does not relevant or control supply.

He does not collect payment on behalf of supplier even not connected in supply or receipt of goods or service.

website is just like a add agency or classified agency e.g. Yellow pages, Just-dial etc.

does he termed as E Commerce Operator ? what is GST registration requirement ?

LETS TAKE AN EXAMPLE

A PVT LTD COMPANY PURCHASES SOME FURNITURE ONLINE ON WHICH GST @5% APPLIES .

WHETHER THE COMPANY ELIGIBLE TO TAKE THE CREDIT OF SUCH INVOICE OR NOT.

IF YES HOW?

Hello sir,

I read your artical.. it is great..

Can you plz assist me in understanding below concern..

We are providing inter state matrimonial information services under our own name thru website where we provide profile details and contacts of one user to other matching user.

We

Would we be considered as e-commerce operator.

Should we take gst number.?

Thanks

AK

very good write -up on E-commerce …

So now the aggregator means nothing but E-commerce operator ,they will be treated as Market place and accordingly GST applicable .