In India, the Companies Act grants companies the autonomy to determine compliance with Section 148 regarding Cost Audit and Records. However, oversight can lead to issues, including show cause notices from the MCA’s Cost Audit Branch.

Cost Audit and Cost Records applicability 2024-25

&

Non Compliance attracting Show Cause Notices

CMA Navneet Kumar Jain

The government of India has given many privileges to India and one of the privileges is to decide at their own about the applicability of various provisions in the Companies Act. The companies have a free hand to decide whether section 148 of the Companies have been complied with or not, the directors and financials auditors have been entrusted with the responsibilities of ensure that wherever applicable cost records have been made and maintained. But it has come to the notice that due to oversight or other reasons, the wrong declarations were given resulting into issue of notices by Cost Audit Branch of MCA.

One question always comes to the mind of the compliance officials of the organisations at the beginning of the year that whether they are required to appoint cost auditor or have to maintain cost records and in which form they have to maintain the cost records, if section 148 of the Companies Act is applicable.

Simple way of checking the applicability of Section 148 with regard to applicability of maintenance of Cost records or cost audit for 2024-25 is

1) to review the financials of 2023-24 & Check the Total turnover of the Company

2) Check the HSN code wise turnover of the company (Manufacturing Turnover only except in case of items mentioned in Srl No 33 of Table B below)

3) Find out the category of HSN codewise sales as per Table A or Table B (Please note that the HSN codes wise sales is for products category, for services one need to refer to the relevant notification-Link given in the article)

The concept of reporting with regard to the maintenance of cost records by directors and financial auditors separately was brought in specifically to ensure that there are no misreportings with regard to applicability. Recently many show cause notices were also issued to companies who had not prepared the cost records or had not filed the cost audit report though apparently as per the data gathered by MCA through various sources Cost Audit seemed to be applicable on those companies.

The companies especially which consider themselves to be out of the ambit of section 148 of the Companies Act 2013 must at the beginning of every year get the same clarified by any professional preferably practicing CMA. It will help them to report the same comfortably in the Director’s report and Auditor’s report may also refer to the clarification obtained from practicing cost accountant.

Extract of one Show Cause Notice is give below which makes it clear that MCA has information with it with regard to the applicability of section 148, so the companies must act on its own rather than waiting for regulators to come calling.

Sub.: Show-Cause Notice for Non-Compliance of provisions of Section- 148 of the Companies Act, 2013.

WHEREAS, it has been found from our records that the company falls under the ambit of Cost Audit for the financial year ending 31st March 2023 but has not filed the Cost Audit Report in prescribed Form to the Central Government within the statutory time limit prescribed by Section 148 (6) of the Act and Rule 6 of Companies (Cost Records and Audit) Rules, 2014 (Rules) read with Section 403 of the Act. Thus, sub-section (6) of Section 148 of the Act has been contravened.

2. AND WHEREAS, as per sub-section (8) of Section 148 of the Act, “If any default is made in complying with the provisions of this section, –

a. The company and every officer of the company who is in default shall be punishable in the manner as provided in sub-section (1) of section 147.

b. the cost auditor of the company who is in default shall be punishable in the manner as provided in sub-sections (2) to (4) of section 147.”

3. WHEREAS your attention is also drawn towards Section 441 of the Act under which the aforesaid contravention may be compounded.

4. Now, therefore the addressees (being the company/ its officers in default as the case may be is called upon to show cause within 30 days from the date of issue of the show cause notice, as to why no penal action as contemplated under Section 148 (8)(a) read with Section 147(1) of the Act be initiated for contravention of Section 148(6) of the Act read with Rule 6 of CCRA Rules, 2014 and Section 403 of the Act.

5. It may be noted that in case you failed to reply (along with supporting documents) within the period as stipulated above, it will be presumed that you have nothing to say in the matter and prosecution will be launched against the company and all its officers who are in default, without any further reference in the matter.

6. In terms of the provision of Section 20 of the Act, the notice is hereby being served to the company and officers of the company who are in default by electronic mode on the email id, as provided by the company on MCA Portal.

7. The company is requested to bring the notice to the knowledge of all the officers who are in default, immediately upon its receipt.

The reason for getting the clarification at the beginning of the year is that the company has to file the form CRA-2 for appointment of cost auditor within 180 days of the beginning of the year The new financial year has begun and all accounting and secretarial professionals are busy in finalization of accounts and other documents for the year 2023-24 on the one hand and on the other hand there are many documents which are required to be filed with Ministry of Corporate Affairs for the year 2024-25 like CRA-2 for appointment of cost auditors.

One can view the updated notification on Companies Cost Audit and Report Rules 2014 at https://icmai.in/upload/pd/Companies_CRAR_2019.pdf

All of us have started experiencing the heat towards the compliance mechanisms being put up by the statutory/regulatory authorities. As the Cost Records and GST records both use the HSN codes for reporting purposes, leniency in the maintenance of cost records or missing out on getting the cost audit conducted can cost a lot hardships to the organisations in case of detection.

The cost audit applicability especially for companies (not under cost audit earlier) is based on the turnover of the previous year. So to check the applicability of cost records maintenance of cost audit one needs to review the HSN codewise turnover primarily. Please review the HSN code figures as have been submitted to GST authorities and reconciled with financials The detailed parameters are given below.

Through this article, we have tried to answer most of queries which a company can have with regard to cost records applicability or cost audit.

The government of India has mandated the maintenance of Cost Records and Cost Audits under section 148 of the Companies Act 2013. The relevant Acts/Rules/provisions with regard to cost records maintenance or cost audit or production of these documents before statutory authorities are given below

1) Companies Act 2013

2) Companies Cost Records and Audit Rules 2014 as amended till date

3) Companies (Audit and Auditors) Rules, 2014

4) Companies (Accounts) Rules, 2014

5) Director’s Responsibility Statement

6) CGST/SGST Acts

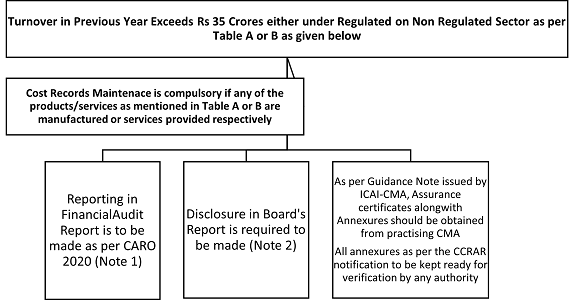

Summarised general steps to check the cost records maintenance or audit applicability. However, in case of inter unit transfers one needs to get the same checked thoroughly in line with various FAQs issued by Institute of Cost Accountants of India. One simple principle one should follow is to get the applicability checked in case turnover in above 35 crores and it is not a finance/banking/insurance/pure trading company (excepting dealing in implants etc.)

1) Compile the HSN codewise turnover of the company (Consolidation of all GSTINs segregated into Distinct person and outside sales) or activity wise turnover as per the activity mentioned in Table A or table B

2) Check for the HSN codes/activity in the Table A or table B of the notification issued by Ministry of Corporate Affairs.

3) Apply the rules for determination of applicability as per the table given below in 1) & 3) e turnover of 35 crores/50 crores/100 crores

Few queries which normally comes to the minds of the Directors/ CFOs/Compliance heads of organisations are given below with summarized replies

| 1) | Whether the company has been mandated under section 148 of the Companies Act 2013 to maintain cost records | Ist step is to check whether the company’s turnover is more than 35 Crores or not. If turnover exceeds Rs 35 Crores, then it needs to be checked whether any of the activities of the company are covered in any of the item under Table A or Table B of CCRAR 2014 (Refer Annexure 1). For this, firstly one needs to check the HSN code wise turnover of the company. This can be checked from the HSN codewise data which is being filed with the GST department through GSTR1. (to be consolidated on yearly basis for determination of overall turnover)

The companies engaged in the production of the goods or providing services, specified in the Tables below as per annexure 1, having an overall turnover from all its products and services of rupees thirty five crore or more during the immediately preceding financial year, shall include cost records for such products or services in their books of accounts |

| 2) | What are cost records | Primarily, Cost Records are records (accounting and statistical) relating to the utilization of various resources for manufacture of goods or provision of services by the organisations. |

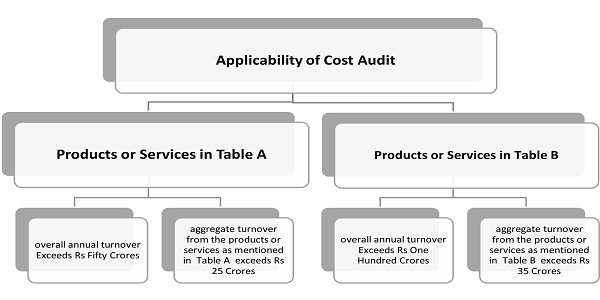

| 3) | whether the cost audit is applicable or not | a) Every company specified in Table (A) of Annexure 1 shall get its cost records audited in accordance with CCRAR 2014 rules if the overall annual turnover of the company from all its products and services during the immediately preceding financial year is rupees fifty crore or more and the aggregate turnover of the individual product or products or service or services for which cost records are required to be maintained is rupees twenty five crore or more

b) Every company specified in table (B) of Annexure 1 shall get its cost records audited in accordance with these rules if the overall annual turnover of the company from all its products and services during the immediately preceding financial year is rupees one hundred crore or more and the aggregate turnover of the individual product or products or service or services for which cost records are required to be maintained under CCRAR 2014 is rupees thirty five crore or more. |

| 4) | What to do if only maintenance of Cost Records is required | The financial auditor and directors are required to report about the applicability of section 148 and maintenance of cost records in the statutory documents viz Financial Audit Report and Director’s Responsibility Statement. |

| 5) | What to do if Cost Audit is also applicable | Appoint Cost Auditor immediately and file CRA-2 with MCA |

| 6) | When a company is required to appoint a Cost Auditor for statutory compliance under section 148 | Please refer to the explanations below |

| 7) | Within how many days the Cost Auditor should be appointed | The category of companies which are manufacturing goods or providing services falling under Table A or Table B and the thresholds limits laid down in rule 4,shall within one hundred and eighty days of the commencement of every financial year, appoint a cost auditor |

| 8) | How the appointment has to be reported to MCA and by what time | Every company on which cost audit is applicable shall inform the cost auditor concerned of his or its appointment as such and file a notice of such appointment with the Central Government within a period of thirty days of the Board meeting in which such appointment is made or within a period of one hundred and eighty days of the commencement of the financial year, whichever is earlier, through electronic mode, in form CRA-2 |

| 9) | Whether product level/ SKU wise/Itemwise data is required to be filed with MCA in case of multi product company | No, the data at eight digit HSN code is required to be filed with MCA in case of products and in case of services as per the relevant statutory requirement to the extent possible |

| 10) | Whether service providers are also covered under cost audit | Yes, only some services are covered, which have been mentioned in Table A or Table B |

| 11) | What type of data is required to be filed with MCA as part of Cost Audit | The data pertaining to costing, HSN codewise profitability, GST reconciliations, Related party Transactions, ratios, value addition etc. are required to be reported |

| 12) | Whether Cost Audit Annexures and Cost audit Report is required to be approved by Board of Directors | The Cost Audit annexures are required to be approved by the board of directors before these are given to Cost Auditor for conducting cost audit.

The Cost Auditor is required to submit Cost Audit Report in CRA-3 form which is required to be considered and examined by Board |

| 13) | How to file the Cost Audit/data or report with MCA | The Cost Audit Report is required to be filed in XBRL format through CRA-4 |

| 14) | What are the due dates for issuing of Cost Audit Report & filing of cost audit annexures and cost audit report in CRA-4 with MCA | The cost audit report should be issued within 180 days of the close of the financials year to which the report relates.

(6) Every company covered under cost audit shall, within a period of thirty days from the date of receipt of a copy of the cost audit report, furnish the Central Government with such report alongwith full information and explanation on every reservation or qualification contained therein, in Form CRA-4 in Extensible Business Reporting Language format. |

| 15) | How the cost data will be used by MCA | The cost audit data is used by different stake holders for policy decision making.

HSN codewise costing and profit abilities are available only in cost audit data on which GST rates are based. |

Primarily, turnover means gross turnover made by the company from the sale or supply of all products or services during the financial year. It includes any turnover from job work or loan license operations, any other operational income but exclude duties and taxes. Export benefit received should be treated as a part of sales

Simplified tables for the activities to be undertaken for compliance with section 148 of the Companies Act 2013 with regard to audit of Items of Cost in Respect of Certain Companies

Applicability of Cost Records Maintenance and reporting in various statutory documents

Note 1: whether maintenance of cost records has been specified by the Central Government under subsection (1) of section 148 of the Companies Act and whether such accounts and records have been so made and maintained; (Reference: Companies (Auditor’s Report) Order, 2020.

Note 2: a disclosure, as to whether maintenance of cost records as specified by the Central Government under sub-section (1) of section 148 of the Companies Act, 2013, is required by the Company and accordingly such accounts and records are made and maintained (Reference: The Companies (Accounts) Rules, 2014)

Applicability of Cost Audit

The companies on which cost records maintenance is applicable may have to undergo cost audit in case further condition of aggregate turnover and tablewise turnover is achieved

Summarised chart showing applicability of Cost audit is given below

Turnovers for the previous years are to be considered for the applicability of section 148 of the Companies Act 2013. Once the cost audit is applicable, it has to be continued even if turnover falls below the minimum criterion in any of the succeeding years.

Please refer to the FAQ as released by Institute of Cost Accountants of India with regard to maintenance of Cost Records as given below:

FAQ 14

Is maintenance of cost accounting records mandatory for a multi-product company where annual turnover from all the products & services is rupees thirty five crore or more during the immediately preceding financial year even if the turnover of the individual product/s that are covered under the Rules is less than rupees thirty five crores?

Reply:

The Rules provide threshold limits for the company as a whole. The Rules do not provide any minimum product specific threshold limits for maintenance of cost accounting records and consequently the company would be required to maintain cost accounting records for the products covered under Table-A or Table-B or both even if the turnover of such products is below rupees thirty five crores but its overall turnover is rupees thirty five crore or more during the immediately preceding financial year.

Micro enterprise or a small enterprise including as per the turnover criteria under sub-section (9) of section 7 of the Micro, Small and Medium Enterprises Development Act, 2006 (27 of 2006) will not be covered.

It is important to note that the cost statements, including other statements to be annexed to the cost audit report, shall be approved by the Board of Directors before they are signed on behalf of the Board by any of the director authorised by the Board, for submission to the cost auditor to report thereon

Through this article an attempt has been made to answer to many queries with regard to the applicability of cost records maintenance and cost audit under section 148 of the Companies Act 2013.

Annexure 1

Companies manufacturing products or providing services as have been mentioned in Table A (Regulated Sectors) or Table B Non Regulated sectors will be covered under Section 148 after fulfilling the turnover criterion

Table (A) Regulated Sectors

| Sl.no | Industry /Sector/ Product/Service | Customs Tariff Act

Heading (wherever applicable) 1. |

| 1. | Telecommunication services made available to users by means of any transmission or reception of signs, signals, writing, images and sounds or intelligence of any nature and regulated by the Telecom Regulatory Authority of India under the Telecom Regulatory Authority of India Act, 1997 (24 of 1997); including activities that requires authorisation or license issued by the Department of Telecommunications, Government of India under Indian Telegraph Act, 1885 (13 of 1885); | Not applicable |

| 2. | Generation, transmission, distribution and supply of electricity regulated by the relevant regulatory body or authority under the Electricity Act, 2003 (36 of 2003); | Generation – 2016;

Other Activity – Not Applicable |

| 3. | Petroleum products; including activities regulated by the Petroleum and Natural Gas Regulatory Board under the Petroleum and Natural Gas Regulatory Board Act, 2006 (19 of 2006); | 2709 to 2715;

Other Activity – Not Applicable |

| 4. | Drugs and pharmaceuticals; | 2901 to 2942; 3001 to

3006. |

| 5. | Fertilisers; | 3102 to 3105. |

| 6. | Sugar and industrial alcohol; | 1701; 1703; 2207. |

Table (B) Non-regulated Sectors

| SN | Industry/ Sector/ Product/ Service | Customs Tariff Act Heading

(wherever applicable) |

| 1. | Machinery and mechanical appliances used in defence, space and atomic energy sectors excluding and ancillary item or items;

Explanation – For the purposes of this sub- clause any company which is engaged in any item or items supplied exclusively for use under this clause, shall be deemed to be covered under these rules. |

8401; 8801 to 8805; 8901 to 8908 |

| 2. | Turbo jets and turbo propellers; | 8411 |

| 3. | Arms and ammunitions and Explosives; | 3601 to 3603; 9301 to 9306. |

| 4. | Propellant powders; prepared explosives (other than propellant powders); safety fuses; detonating fuses; percussion or detonating caps; igniters; electric detonators; | 3601 to 3603 |

| 5. | Radar apparatus, radio navigational aid apparatus and radio remote control apparatus; | 8526 |

| 6. | Tanks and other armoured fighting vehicles, motorized, whether or not fitted with weapons and parts of such vehicles, that are funded (investment made in the company) to the extent of ninety per cent, or more by the Government or Government agencies; | 8710 |

| 7. | Port services of stevedoring, pilotage, hauling, mooring, re-mooring, hooking, measuring, loading and unloading services rendered for 9 a Port in relation to a vessel or goods regulated by the Tariff Authority for Major Ports under the Major Ports Trusts Act, 1963 (38 of 1963) 10 ; | Not applicable. |

| 8. | Aeronautical services of air traffic management, aircraft operations, ground safety services, ground handling, cargo facilities and supplying fuel rendered at the 11 airports and regulated by the Airports Economic Regulatory Authority under the Airports Economic Regulatory Authority of India Act, 2008 (27 of 2008); | Not applicable. |

| 9. | Iron and Steel; | 7201 to 7229; 7301 to 7326 |

| 10. | Roads and other infrastructure projects corresponding to para No.(1) (a) as specified in Schedule VI of the Companies Act, 2013; | Not applicable. |

| 11. | Rubber and allied products being regulated by the

Rubber Board constituted under the Rubber Act, 1947 (XXIV of 1947) |

4001 to 4017 |

| 12. | Coffee and tea; | 0901 to 0902 |

| 13. | Railway or tramway locomotives, rolling stock, railway

or tramway fixtures and fittings, mechanical (including electro mechanical) traffic signaling equipment’s of all kind; |

8601 to 8608; 8609. |

| 14. | Cement; | 2523; 6811 to 6812 |

| 15. | Ores and Mineral Products; | 2502 to 2522; 2524 to

2526; 2528 to 2530; 2601 to 2617 |

| 16. | Mineral fuels (other than Petroleum), mineral oils etc.; | 2701 to 2708 |

| 17. | Base metals; | 7401 to 7403; 7405 to

7413; 7419; 7501 to 7508; 7601 to 7614; 7801 to 7802; 7804; 7806; 7901 to 7905; 7907; 8001; 8003; 8007; 8101 to 8113. |

| 18. | Inorganic chemicals, organic or inorganic compounds of precious metals, rare-earth metals of radioactive elements or isotopes, and Organic Chemicals; | 2801 to 2853; 2901 to 2942; 3801 to 3807; 3402 to 3403; 3809 to 3824. |

| 19. | Jute and Jute Products; | 5303, 5307 13 , 5310 |

| 20. | Edible Oil; | 1507 to 1518 |

| 21. | Construction Industry as per para No.(5) (a) as specified in Schedule VI of the Companies Act, 2013 (18 of 2013) | Not applicable. |

| 22. | Health services, namely functioning as or running hospitals, diagnostic centres, clinical centres or test laboratories; | Not applicable. |

| 23. | Education services, other than such similar services falling under philanthropy or as part of social spend which do not form part of any business. | Not applicable. |

| 24. | Milk powder; | 0402 |

| 25. | Insecticides; | 3808 |

| 26. | Plastics and Polymers; | 3901 to 3914; 3916 to 3921; 3925 |

| 27. | Tyres and Tubes; | 4011 to 4013 |

| 28. | Pulp and Paper; | 4701 to 4704; 4801 to 4802 |

| 29. | Textiles; | 5004 to 5007; 5106 to 5113; 5205 to 5212; 5303;

5307; 16 5310; 5401 to 5408; 5501 to 5516 |

| 30. | Glass; | 7003 to 7008; 7011; 7016 |

| 31. | Other machinery and Mechanical Appliances; | 8403 to 8487 |

| 32. | Electricals or electronic machinery; | 8501 to 8507; 8511 to 8512; 8514 to 8515; 8517; 8525 to 8536; 8538 to 8547. |

| 33. | Production, import and supply or trading of following medical devices, namely:-

(i) Cardiac stents; (ii) Drug eluting stents; (iii) Catheters; (iv) Intra ocular lenses;; (v) Bone cements; (vi) Heart valves; (vii) Orthopaedic implants (viii) Internal prosthetic replacements; (ix) Scalp vein set; (x) Deep brain stimulator (xi) Ventricular peripheral shud; (xii) Spinal implants; (xiii) Automatic impalpable cardiac defibrillators17; (xiv) Pacemaker (temporary and permanent); (xv) Patent ductus arteriosus, atrial septal defect and ventricular septal defect closure device; (xvi) Cardiac re-synchronize therapy; (xvii) Urethra spinicture devices (xviii) Sling male or female; (xix) Prostate occlusion device; and (xx) Urethral stents; |

9018 to 9022 |

Penal provisions for non-compliances:

If any default is made in complying with the provisions of section 148,—

(a) the company and every officer of the company who is in default shall be punishable in the manner as provided in sub-section (1) of section 147;

Section 147(1) states that for any contravention of the sections 139 to 146 (Both Inclusive)of Companies Act the company shall be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees and every officer of the company who is in default shall be punishable with fine which shall not be less than ten thousand rupees but which may extend to one lakh rupees.

(b) the cost auditor of the company who is in default shall be punishable in the manner as provided in sub-sections (2) to (4) of section 147.

Summarised provision: (If cost auditor of a company contravenes any of the provisions of section 148, the cost auditor shall be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees or four times the remuneration of the auditor, whichever is less. Provided that if an auditor has contravened such provisions knowingly or wilfully with the intention to deceive the company or its shareholders or creditors or tax authorities, he shall be punishable with imprisonment for a term which may extend to one year and with fine which shall not be less than fifty thousand rupees but which may extend to twenty-five lakh rupees or eight times the remuneration of the auditor, whichever is less)

An attempt has been made to explain the provisions in simplified manner. The readers are requested to go through the provisions in details from the gazette notifications. The author has explained the provisions as per his understanding, The readers may send mail for any enquiries/clarifications to navneetic@yahoo.com

CMA Navneet Kumar Jain | Jitender Navneet & Co | Cost Accountants | PCAOB Registered Public Accounting Firm | navneetic@yahoo.com

Author Bio

My client company, a yarn manufacturer, has discontinued cost audits from 2020-21. What are the available sources/options for filing the cost audit report?”

My client companies (three construction companies) have discontinued the cost audits from 2020-21 . What is to be done ? Can we report to somebody ? If so , to whom ?

Thank you so much for information.