#NAA

Log in to FollowEvery article filed under the “NAA” tag — analysis, news and updates.

454 articlesGoods and Services Tax

Goods and Services Tax

Profiteering cannot be alleged for project completed before 01.07.2017

Goods and Services Tax

Goods and Services Tax

Sri Laxmi Kala Mandir Guilty of not passing GST reduction benefit to Customers: NAA

Goods and Services Tax

Goods and Services Tax

NAA directs ‘Jay Ambe Developers’ to pass on ITC benefit to Homebuyers

Goods and Services Tax

Goods and Services Tax

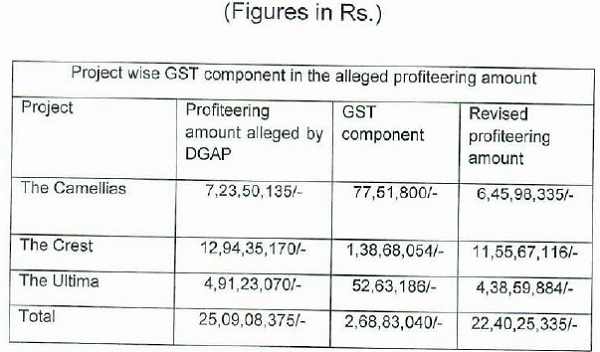

DLF guilty of profiteering in its Projects namely Camellia/Crest/Ultima: NAA

Goods and Services Tax

Goods and Services Tax

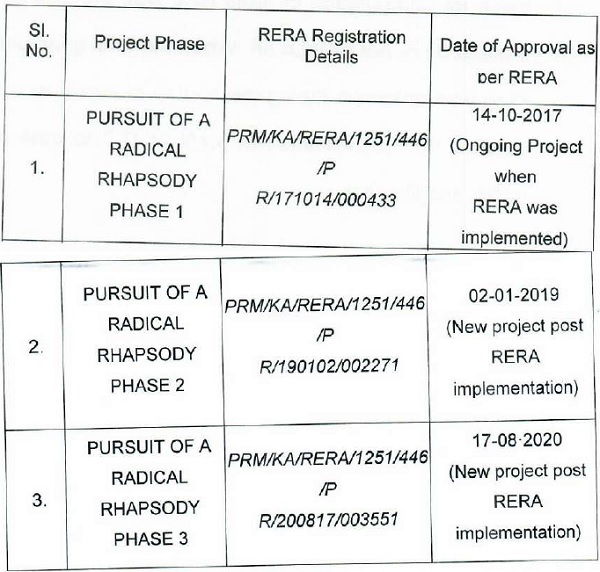

Anti-Profiteering provisions not applies to projects not in existence in GST period

Goods and Services Tax

Goods and Services Tax

JMD builder guilty of profiteering in its Project JMD Imperial Suits: NAA

Goods and Services Tax

Goods and Services Tax

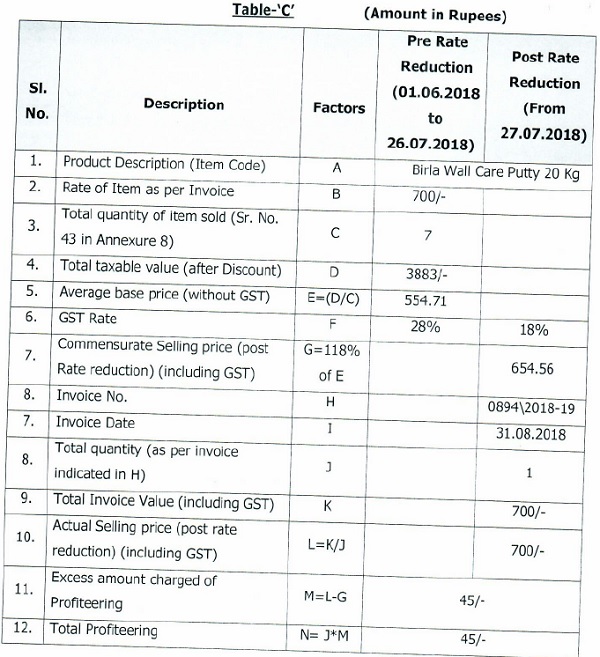

Prathima Multiplex guilty of not passing tax reduction benefit to Customers: NAA

Goods and Services Tax

Goods and Services Tax

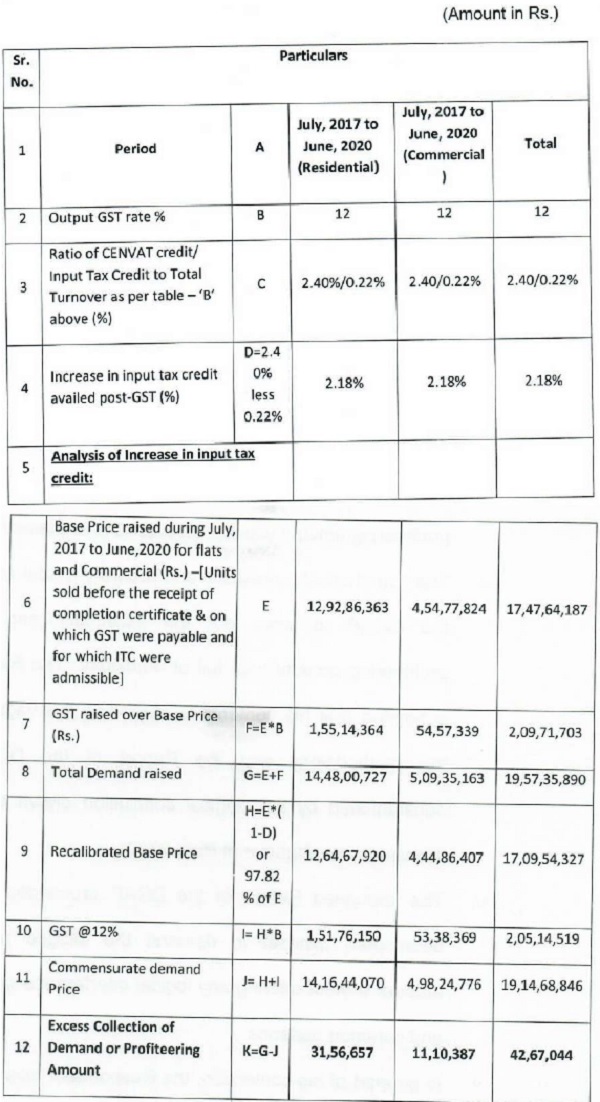

NAA directs ‘Total Environment Habitat’ to refund profiteered amount to Home buyers

Goods and Services Tax

Goods and Services Tax

NAA directs ‘Savaliya Procon’ to refund profiteered amount to home buyers with interest

Goods and Services Tax

Goods and Services Tax