CA Ashish Gupta

With the introduction of Negative List Approach under Service Tax Regime, the significance of categorization of taxable services was done away and all the services were grouped under two heads i.e. Taxable & Non-Taxable. Consequently, the payment of service tax was to be made under the Head – All Taxable Services. However, CBEC issued a Circular 165/16/2012 dated 20-11-2012 stating that henceforth all payments of service tax, interest & penalty shall be made under old Accounting Heads of taxable services for analytical purposes. Further, all new service tax registrations shall be made under respective services.

With the introduction of Negative List Approach under Service Tax Regime, the significance of categorization of taxable services was done away and all the services were grouped under two heads i.e. Taxable & Non-Taxable. Consequently, the payment of service tax was to be made under the Head – All Taxable Services. However, CBEC issued a Circular 165/16/2012 dated 20-11-2012 stating that henceforth all payments of service tax, interest & penalty shall be made under old Accounting Heads of taxable services for analytical purposes. Further, all new service tax registrations shall be made under respective services.

Earlier, the services rendered in relation to construction activities were classified under following service categories:

• Construction of Complex Service (CCS)

• Commercial of Industrial Construction Service (CICS)

• Works Contract Service (WCS)

From July, 2012 onwards the services in relation to construction activities were clubbed under one category i.e. Works Construct Service. It was deemed that all such service providers shall now be treated as Works Contractor and all the provisions shall equally apply to them. There was no contrary view in this regard, thus, the service providers were eligible to apply new valuation rules for valuation of construction services. Initially service tax was to be paid under the head All Taxable Services, therefore, it was not necessary to change the category from CICS / CCS to WCS. But when the aforesaid Circular was affected, the old accounting codes were restored and in such case CICS/CCS providers should have amended their registration by changing their service category to WCS. Although the circular does not effect the legal position on taxability of construction services but it brings certain procedural changes which needs to be observed by such service providers.

Subsequently, the service providers might be under the impression that their classification of service shall remain same and have continued to deposit service tax under respective accounting heads i.e. CICS or CCS. But the valuation options available under N. No. 24/2012 are only applicable on services executed under a works contract. Although the works contract includes the services of CICS or CCS but practically the category is different. Therefore, the service providers are required to amend their service tax registration by replacing CICS / CCS with WCS.

Now, the service tax return utility for the period Jul-Sep, 2012 released by CBEC has incorporated the effect of all new notifications with respect to Abatements, Exemptions & Reverse Charge as applicable for respective taxable service which is required to be submitted by 15th April, 2012. Although the classification of services has no significance now, but in service tax return assessee is required to furnish service-wise details as per the old taxable categories.

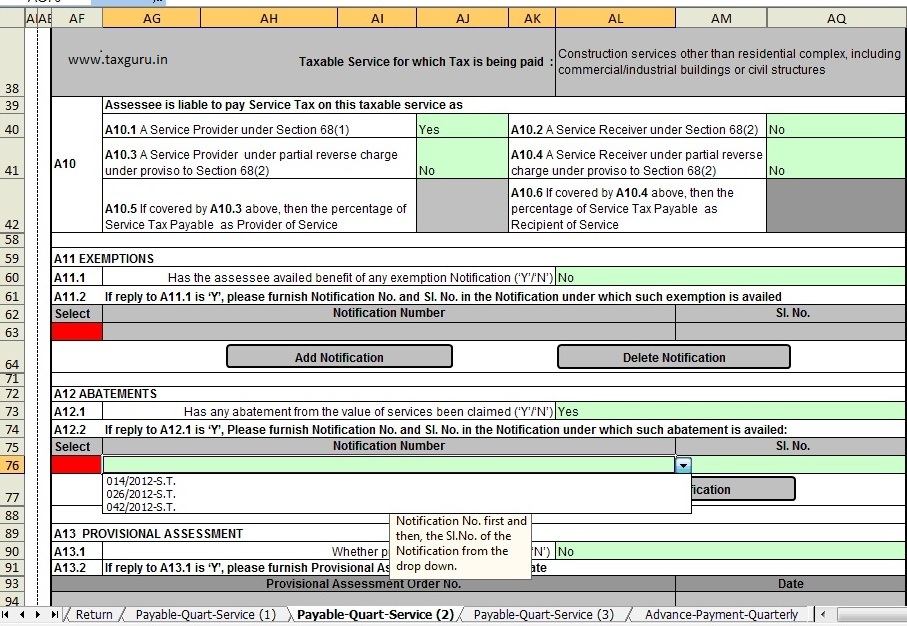

Case of a CICS provider:

Suppose a CICS provider, from July, 2012 has started charging service tax in accordance with the new valuation rules as provided in N. No. 24/2012 by availing percentage based valuation of its services. Thus, for every original construction he shall pay service tax on 40% of the total value charged for such services. But the payment of tax was made under CICS category as the aforesaid Circular restore the old accounting heads.

Now, the service tax return for the 2nd Qtr has to be filled in new return utility according to the amended provisions. The new return utility does not allow a CICS provider to mention the aforesaid notification number under the column of “Has any abatement from the value of service been claimed”. The drop down options only provides the abatement notification number and not the notification of valuation rules as presented below:

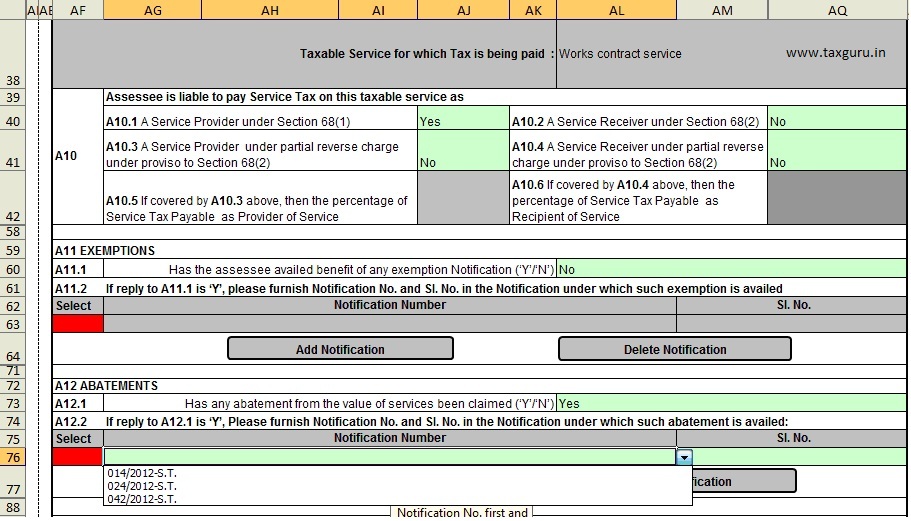

Since the N. No. 24/2012 offers valuation of services provided under the execution of a works contract, the benefit of such notification is only available to the WCS provider as it is cleared in the return utility:

It is clear from above that the provisions of N. No. 24/2012 are not applicable on the taxable service category of CICS or CCS. Technically the services rendered under CICS/CCS are now termed as WCS but until the service category is changed in the registration, a service provider may procedurally be not allowed to avail the benefit of such notification. Since the new return utility restricts the benefit of such notification to works contractors only, CICS provider has to amend their service tax registration so as to provide correct information in returns.

Case of a CCS provider:

Similarly it happens with CCS provider where the service provider has chooses to pay tax on the value of service determined on the basis of options given in N. No. 24/2012. In the return utility the option to avail the benefit of such notification is also not available to CCS provider, thus, they also have to amend their registration so as to remove such irregularity.

Conclusion:

The service providers engaged in providing CICS or CCS has following two options for filling return for 2nd Qtr:

1. File service tax return as WCS and get their registration amended by replacing CICS or CCS with WCS; or

2. File service tax return with out mentioning the abatement Notification No. but in such case amount of abatement claimed can not be provided in return.

It is suggested that the service providers should choose Option 1 as they have already paid service tax on the basis of the N. No. 24/2012.

Dear sir,

Is it that we have to select the notification and mention the amount of 60% in abatement?

Hi Deepak

Thats very true and I already mentioned that the service providers who claimed benefit under N.No. 24/2012 needs to change their category only and not others.

Thanks

Hi,

Thanks for sharing your views. But I feel that CICS / CCS service providers can opt 25% abatement scheme, if the land value is included, as per the Sl. No.12 of notification no. 26/2012, otherwise only need to opt for conversion to WCS..

Kindly correct me if I am wrong.