Alternative Investment Funds (AIF) refers to a fund created or incorporated in India by pooling of funds from various investors whether Indian or foreigner by way of private placement for investment in a portfolio of securities in accordance with the defined investment policy for the benefit of its investors. AIF as the name suggests is an alternative mode of investment vis-à-vis the conventional modes like equity, bond etc. and are governed by SEBI (“Board”) vide the Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012.

In the recent years, this sector has attracted more number of investors pursuant to various factors like diversification, higher returns etc. in comparison to the traditional investment modes and as a result more number of AIFs are being registered. Through this article we have tried to answer some frequently asked questions relating to the eligibility and process for registration and compliances of AIF in India.

Q 1. What shall be the Structure of the AIF?

The AIFs can be registered in either of the following form:

a. Company

b. LLP

c. Trust

d. Body corporate set up under the laws of the Central or State Legislature

Q 2. What is the eligibility criteria to register the AIF?

For the purpose of the grant of certificate to an applicant, the Board considers the following conditions for eligibility, namely-

a. Authorisation – There has to be an authorisation in memorandum of association in case of Company, trust deed in case of trust and limited liability partnership deed in case of limited liability partnership to carry on the activities of AIF.

b. Registered deed – The trust or LLP applying for registration shall have its trust deed and LLP deed registered respectively and in case of Body corporate, it should have been set up or established under the laws of the Central or State Legislature and is permitted to carry on the activities of the AIF;

c. Qualification – At least one key personnel in the investment team of the manager of AIF shall have at least five years’ experience in advising or managing pools of capital or in fund or asset or wealth or portfolio management or in the business of buying, selling and dealing of securities or other financial assets and has relevant professional qualification;

d. Fit and proper person – The applicant, sponsor and manager must be fit and proper persons based on the criteria specified in Schedule II of the Securities and Exchange Board of India (Intermediaries) Regulations, 2008. The Board takes into account any consideration as it deems fit, including but not limited to the following criteria:

i. integrity, reputation and character;

ii. absence of convictions and restraint orders;

iii. competence including financial solvency and net worth.

e. Infrastructure – The manager or sponsor shall have the necessary infrastructure and manpower to effectively discharge its activities;

f. Investment Objectives and other details – The applicant shall clearly describe at the time of registration the objective of its investment, the targeted investors, proposed corpus, investment style or strategy and proposed tenure of the fund or scheme;

g. Disclosure for previous refusal – The applicant or any entity established by the sponsor or manager shall disclose whether the applicant or entity has earlier been refused registration by the Board;

h. In principal approval – In cases where the trust deed or LLP agreement are not registered, then the Board may grant an in principal approval if the applicant complies with the registration within six months. The AIF having in principal approval can accept commitments from investors but cannot accept the money till the registration is granted;

If the Board is not satisfied about granting certificate of registration, it may reject the application and inform the same to applicant within thirty days.

Q 3. What is the process of registration of the AIF?

The following shall be the process of registration of AIF:

a. Application – An application for registration shall be made in Form A, along with non-refundable application money of one lakh rupees, by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by a bank draft in favour of “The Securities and Exchange Board of India” at Mumbai.

b. Personal Appearance – Once the Board receives the application, the same will be examined and the Board may ask for any such information from sponsor or manager or in relation to the activities of the applicant and may also call the sponsor or manager for personal appearance.

c. Registration Fees – If the Board is satisfied with the application, it shall notify the applicant stating that the application was successful. The applicant shall then proceed for payment of registration fee of five lakh rupees, by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by bank draft in favour of “The Securities and Exchange Board of India” at Mumbai.

d. Certificate of Registration – The Board when satisfied about the fulfilment of the requirements of the regulations may grant certificate for registration in Form B. The Board can also lay certain conditions on grant of the certificate of registration which shall be valid till the AIF is wound up.

Q 4. What are the categories under which the registration can be granted?

The registration can be applied for under any of the three below mentioned categories:

Category I AIF

|

Category II AIF

|

Category III AIF

|

Further, the AIF which has been granted registration under a particular category cannot change its category subsequent to registration, except with the approval of the Board.

Q 5. What are the conditions and restrictions on Investments?

All AIF shall state investment strategy, investment purpose and its investment methodology in its placement memorandum to the investors. In order to invest in the AIF registered under any of the three categories, the investment shall be subject to the conditions below:

a. Investors – The AIF may raise funds from any investor whether Indian, foreign or non-resident Indians by way of issue of units.

b. Minimum Corpus – Each scheme of the AIF shall have corpus of at least twenty crore rupees.

c. Minimum investment value – The AIF shall not accept from an investor, an investment of value less than one crore rupees; provided that in case of investors who are employees or directors of the AIF or employees or directors of the Manager, the minimum value of investment shall be twenty-five lakh rupees.

d. Continuing interest – The Manager or Sponsor shall have a continuing interest in the AIF of not at least 2.5% of the corpus or Rs. 5 crores, whichever is lower, in the form of investment in the AIF and such interest shall not be through the waiver of management fees; provided that for Category III AIF, the continuing interest shall be not less than 5% of the corpus or Rs. 10 crores, whichever is lower.

e. Disclosure of investment – The Manager or Sponsor shall disclose their investment in the AIF to the investors of the AIF.

f. Limit on maximum investors – No scheme of the AIF shall have more than 1,000 investors; provided that the provisions of the Companies Act, 2013 shall apply to the AIF, if it is formed as a company.

g. Private placement – The AIF shall collect investment only by way of private placement.

h. Material alteration – Any material alteration to the fund strategy shall be made with the consent of at least two-thirds of unit holders by value of their investment in the AIF.

i. Limits of investment – Category I and II AIF shall invest not more than 25% of the investable funds in one Investee Company. Category III AIF shall invest not more than 10% of the investable funds in one Investee Company.

Q 6. How do the AIF raise investments?

a. The AIF may launch schemes subject to filing of placement memorandum with the Board in order to raise the investments.

b. Such placement memorandum shall be filed with the Board at least thirty days prior to launch of scheme along with the fees of one lakh rupees by way of direct credit in the bank account through NEFT/RTGS/IMPS or any other mode allowed by RBI or by bank draft in favour of “The Securities and Exchange Board of India” at Mumbai. Provided that payment of scheme fees shall not apply in case of launch of first scheme by the AIF.

c. The Board may communicate its comments, if any, to the applicant prior to launch of the scheme and the applicant shall incorporate the comments in the placement memorandum prior to launch of scheme.

Q 7. What is the tenure of the AIF?

Category I and II AIF or schemes launched by such funds shall have a minimum tenure of three years.

Q 8. Can the tenure of the AIF be extended?

a. The extension of the close ended AIF may be permitted up to two years subject to approval of two-thirds of the unit holders by value of their investment in the AIF.

b. The AIF shall fully liquidate within one year following expiration of the fund tenure or extended tenure in case where consent for extension is not granted.

Q 9. How can the AIF be liquidated?

In the absence of consent of its unit holders, the AIF shall fully liquidate within one year following expiration of the fund tenure or extended tenure.

Q 10. Can the units of AIF be listed?

a. The units of close ended AIF may be listed on stock exchange subject to a minimum tradable lot of one crore rupees.

b. Listing of AIF units shall be permitted only after final close of the fund or scheme.

Q 11. What are the compliances to be made by the AIF?

a. Review of policies – All AIFs are required to review that their policies and procedures are being implemented on a regular basis.

b. Custodian – AIF is required to mandatorily appoint a custodian registered with Board for safekeeping of securities if the corpus of the AIF exceeds five hundred crore rupees. Category III AIF is required to appoint such custodian irrespective of the size of corpus of the AIF.

c. Change in management – In case of any change in sponsor, manager or designated partners or any other material change from the information provided by the AIF at the time of application for registration, the same is required to be informed to the Board.

d. Change in control – In case of any change in control of the AIF, sponsor or manager, prior approval from the Board is required by the AIF.

e. Auditor – The books of accounts of the AIF are required to be audited annually by a qualified auditor.

f.Valuation –

i. AIF shall provide the description of its valuation procedure and methodology for valuing assets to its investors.

ii. An independent valuer shall undertake the valuation of investments of Category I and Category II AIF on half yearly basis. Such valuation can be made annual if approved by the investor having invested 75% in value in the AIF.

iii. Category III AIFs shall ensure that the calculation of the net asset value (“NAV”) and the fund management function of the AIF are independent.

iv. Such NAV shall be disclosed to the investors at intervals not longer than a quarter for close ended funds and at intervals not longer than a month for open ended funds.

g. Conflict of Interest – The sponsor and manager of the AIF shall act in a fiduciary capacity towards its investors and shall disclose to the investors, all conflicts of interests as and when they arise or seem likely to arise.

h. Disclosures to investors – AIF shall ensure transparency and disclose the following information periodically or on event basis to its investors:

Periodic Disclosure:

i. financial, risk management, operational, portfolio, and transactional information regarding fund investments;

ii. any fees ascribed to the manager or sponsor; and any fees charged to the AIF or any investee company by an associate of the manager or sponsor;

iii. annual report to its investors within one hundred and eighty days from the end of year stating the financial information of investee companies and the material risks and how they are managed.

Event Basis Disclosure:

i. any inquiries/ legal actions by legal or regulatory authorities in any jurisdiction;

ii. any material liability arising during the AIF’s tenure;

iii. any breach of a provision of the placement memorandum; or agreement made with the investor or any other fund documents, if any; and

iv. change in control of the Sponsor or Manager or Investee Company

i. Maintenance of Records – The Manager or Sponsor shall be required to maintain the records describing:

i. the assets under the scheme/fund;

ii. valuation policies and practices;

iii. investment strategies;

iv. particulars of investors and their contribution;

v. rationale for investments made.

The records shall be maintained for a period of five years after the winding up of the fund.

Submission of reports to the Board – The Board may at any time seek such information, reports, documents etc. from AIF as it may desire, with respect to the activities carried on by AIF.

k. Dispute resolution – AIF either by itself or by its manager or sponsor shall have a mechanism for dispute resolution and laid down procedure for resolution of disputes between the investors, AIF, Manager or Sponsor which may be mutually decided between the investors and the AIF.

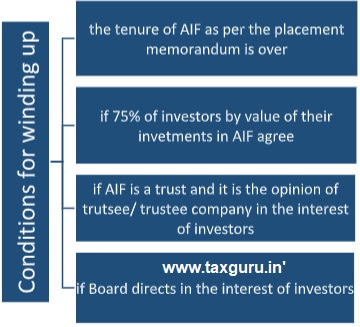

Q 12. What are the conditions and procedure for winding up of the AIF?

a. The process of winding up of the AIF registered either in the form trust, LLP, company or body corporate shall also be governed by their respective laws.

b. The AIF shall intimate the Board and investors of the situations and conditions leading to the winding up.

c. Post intimation to Board and investors, no further investments shall be made by the AIF.

d. The assets shall be liquidated, and the proceeds accruing to investors in the AIF shall be distributed after satisfying all liabilities within one year of the date of intimation to Board and investors.

e. If there is any condition in placement memorandum regarding the specific distribution, such condition must be approved, after obtaining consent of at least 75% of the investors by value of their investment in the AIF.

f. The registration certificate shall be surrendered to the Board upon winding up of the AIF.

AIF is relatively a new concept for Indian market and accordingly represents a very small share in the global market. The government is required to take certain initiatives like inculcating more compliance related disclosures leading to transparency and belief of investors in the funds, attracting the domestic investors so that dependency on foreign funds are reduced, relaxations in the minimum investment limit etc. to encourage investments in AIF. It can further be seen that the inclination of investors in this sector in line with their risk return perspective backed by the stringent regulations of government on non-compliances will definitely improve the current statistics of Indian AIF in the global market.

Author Bio